If you own a free standing home in Merriwagga, NSW 2652, you might be wondering whether you're paying a fair price for home and contents insurance — or leaving money on the table. This article breaks down a real insurance quote for a three-bedroom weatherboard home in Merriwagga, benchmarks it against local, state, and national data, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The annual premium for this quote comes in at $1,611 per year (or $156 per month), covering a building sum insured of $459,000 and $50,000 in contents. Both the building and contents excess are set at $2,000.

Based on our pricing data, this quote is rated CHEAP — below average for the area. That's genuinely good news for the homeowner. At the 25th percentile for Merriwagga, the suburb benchmark sits at $1,692 per year, meaning this quote actually undercuts even the cheapest quarter of local premiums. Compared to the suburb average of $2,140 and the median of $1,975, this policyholder is saving anywhere from $364 to $529 per year simply by securing a competitive quote.

It's worth noting that a higher excess ($2,000 for both building and contents) does contribute to a lower premium. Choosing a higher excess means you agree to cover more out-of-pocket in the event of a claim, which insurers reward with reduced upfront costs. If cash flow is a concern, it's worth modelling what a lower excess would cost — but for homeowners with solid savings, this is a smart trade-off.

---

How Merriwagga Compares

To put this quote in full context, here's how Merriwagga stacks up against broader benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $1,611 |

| Merriwagga Suburb Average | $2,140 |

| Merriwagga Suburb Median | $1,975 |

| LGA (Griffith) Average | $2,279 |

| NSW State Average | $3,801 |

| NSW State Median | $3,410 |

| National Average | $2,965 |

| National Median | $2,716 |

The contrast with NSW state figures is particularly striking. The NSW state average premium of $3,801 is more than double this quote — a reflection of how dramatically premiums can vary across the state. Coastal and flood-prone regions of NSW tend to push state averages up considerably, which makes inland rural areas like Merriwagga comparatively affordable to insure.

Even against the national average of $2,965, this quote sits well below the midpoint. Homeowners in Merriwagga are in a relatively low-risk environment compared to many parts of Australia, and that's reflected in the pricing. You can explore the full Merriwagga suburb insurance stats to see how the local market is trending over time.

Note: Merriwagga suburb data is based on a sample of 14 quotes, so averages should be treated as indicative rather than definitive.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers price the risk. Understanding these factors can help you anticipate how your own home might be assessed.

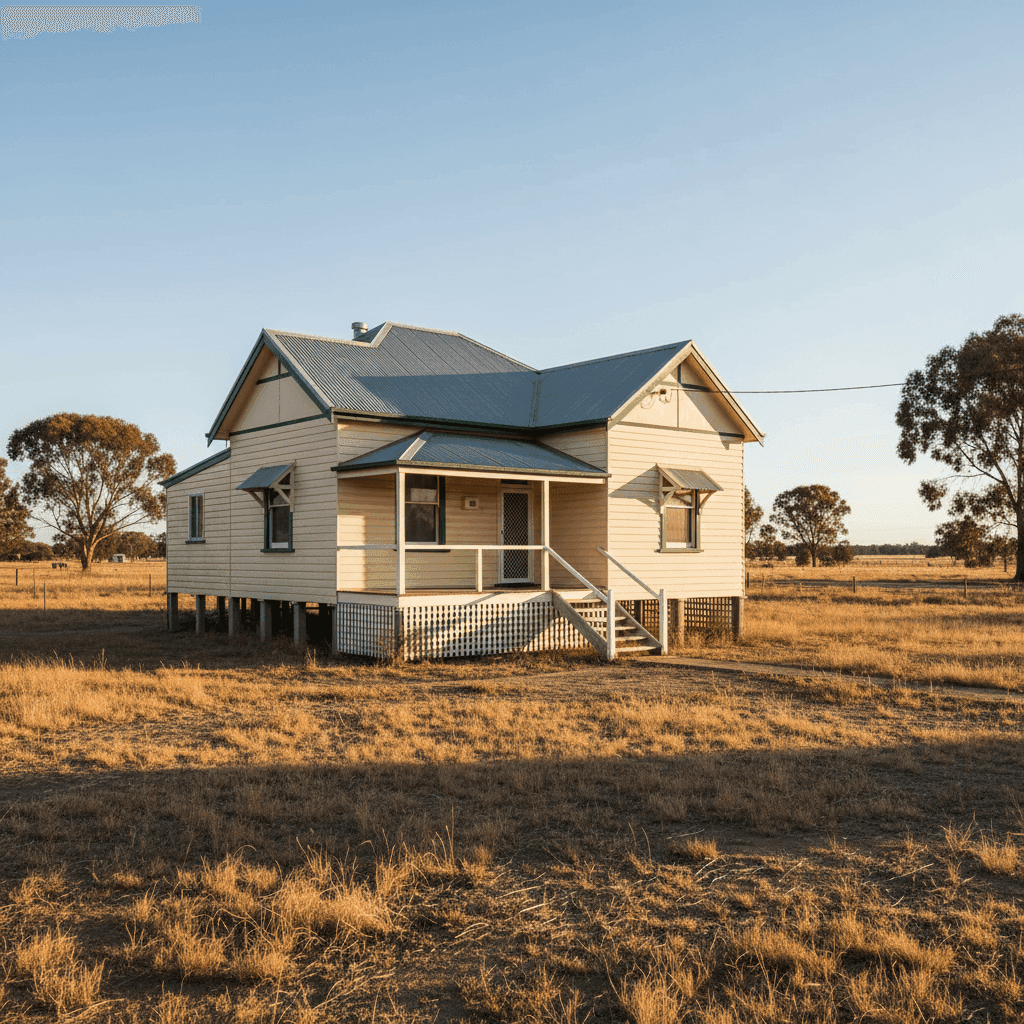

Weatherboard timber walls are one of the most significant rating factors here. Timber-framed and clad homes are generally considered higher risk than brick veneer or double brick constructions, primarily due to fire susceptibility. Insurers typically apply a loading to weatherboard homes, which can push premiums higher — making the competitive price achieved here even more impressive.

Steel/Colorbond roofing is viewed favourably by most insurers. It's durable, resistant to hail damage, and performs well in high-wind conditions. Compared to older tile or corrugated iron roofs, Colorbond is generally associated with lower claims frequency, which can help moderate your premium.

Stumped foundations — where the home is elevated on timber or concrete stumps — add a layer of complexity to the risk assessment. On the positive side, elevation can reduce exposure to ground-level flooding and moisture ingress. However, stumped homes may be considered more vulnerable to certain structural risks, and the elevated floor space can be a factor in building replacement cost estimates.

Construction year (1964) means this is a home with over 60 years of history. Older homes can attract higher premiums due to the likelihood of ageing plumbing, wiring, and structural components. Replacement costs for period-style construction can also be higher than modern builds, as sourcing matching materials and skilled tradespeople adds to the cost of reinstatement.

Timber and laminate flooring is relatively straightforward from an insurance perspective, though it's worth ensuring your contents sum insured accounts for the cost of floor coverings if they're not included in your building policy.

The property is not in a cyclone risk zone, has no pool, no solar panels, and no ducted climate control — all of which keep the risk profile clean and the premium manageable.

---

Tips for Homeowners in Merriwagga

1. Review your building sum insured regularly A $459,000 building sum insured for a 130 sqm home built in 1964 may be appropriate now, but construction costs have risen sharply in recent years. Use a building replacement cost calculator annually to ensure you're not underinsured — particularly important for older weatherboard homes where like-for-like replacement can be expensive.

2. Maintain your weatherboard cladding Timber exteriors require ongoing maintenance to remain insurable at competitive rates. Peeling paint, rotting boards, or untreated timber can signal deferred maintenance to insurers and may affect your ability to claim. A well-maintained home is also less likely to suffer weather-related damage in the first place.

3. Consider the excess trade-off carefully This policy carries a $2,000 excess on both building and contents — a meaningful out-of-pocket cost if something goes wrong. If you'd prefer a lower excess, compare quotes at CoverClub to see what different excess levels mean for your annual premium. The right balance depends on your personal financial buffer.

4. Don't set and forget your contents sum insured $50,000 in contents cover is a common starting point, but it's easy to underestimate how much your belongings are actually worth. Walk through each room and tally up furniture, appliances, clothing, and valuables. Many Australians are underinsured on contents without realising it — and in a claim scenario, that gap can be costly.

---

Compare Quotes and Save

Whether you're renewing your existing policy or shopping for the first time, it pays to compare. The data shows that premiums in Merriwagga can vary significantly — from under $1,700 to over $2,500 per year for similar properties. Getting multiple quotes is the simplest way to make sure you're on the right side of that range.

Get a home insurance quote at CoverClub and see how your property stacks up in seconds. With suburb-level benchmarking and side-by-side comparisons, CoverClub makes it easy to find cover that fits your home — and your budget.