If you own a free standing home in Metford, NSW 2323, you're probably wondering whether what you're paying for home and contents insurance is reasonable — or whether you're leaving money on the table. This article breaks down a real insurance quote for a four-bedroom, two-bathroom brick veneer home in Metford, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question comes in at $2,463 per year (or $241 per month) for combined home and contents insurance, covering a building sum insured of $619,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Metford sits at $2,404 per year, meaning this quote is only about $59 above the local average — a difference of roughly 2.5%. It also falls comfortably within the suburb's interquartile range of $1,752 to $2,472, placing it squarely in the middle of the pack rather than at either extreme.

In short, this isn't a bargain, but it's not an overpriced outlier either. For a well-built 2004 home with solar panels, ducted climate control, and a 214 sqm floor plan, a premium in this range is broadly consistent with what Metford homeowners are paying.

---

How Metford Compares

To put this quote in proper context, it helps to zoom out and look at the bigger picture. Metford's suburb insurance data is based on 18 quotes, which gives us a reasonable local sample to work with.

| Benchmark | Premium |

|---|---|

| This Quote | $2,463/yr |

| Metford Suburb Average | $2,404/yr |

| Metford Suburb Median | $2,287/yr |

| NSW State Average | $9,528/yr |

| NSW State Median | $3,770/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

| Lake Macquarie LGA Average | $11,064/yr |

The numbers tell an interesting story. While this quote is close to the Metford suburb average, it sits well below the NSW state average of $9,528 and the national average of $5,347. It's worth noting, however, that state and national averages are heavily skewed upward by high-risk areas — particularly flood and cyclone-prone regions — so the median figures are often more meaningful for comparison.

Against the NSW median of $3,770 and the national median of $2,764, this quote looks even more competitive. Metford, situated in the Hunter Valley, doesn't carry the extreme weather risk premiums seen in parts of Queensland or northern NSW, which helps keep local insurance costs relatively contained.

The Lake Macquarie LGA average of $11,064 appears unusually high and is likely influenced by a mix of high-value properties and higher-risk postcodes within the broader LGA — another reason why suburb-level data is far more useful than LGA-wide figures when assessing your own premium.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the insurance premium:

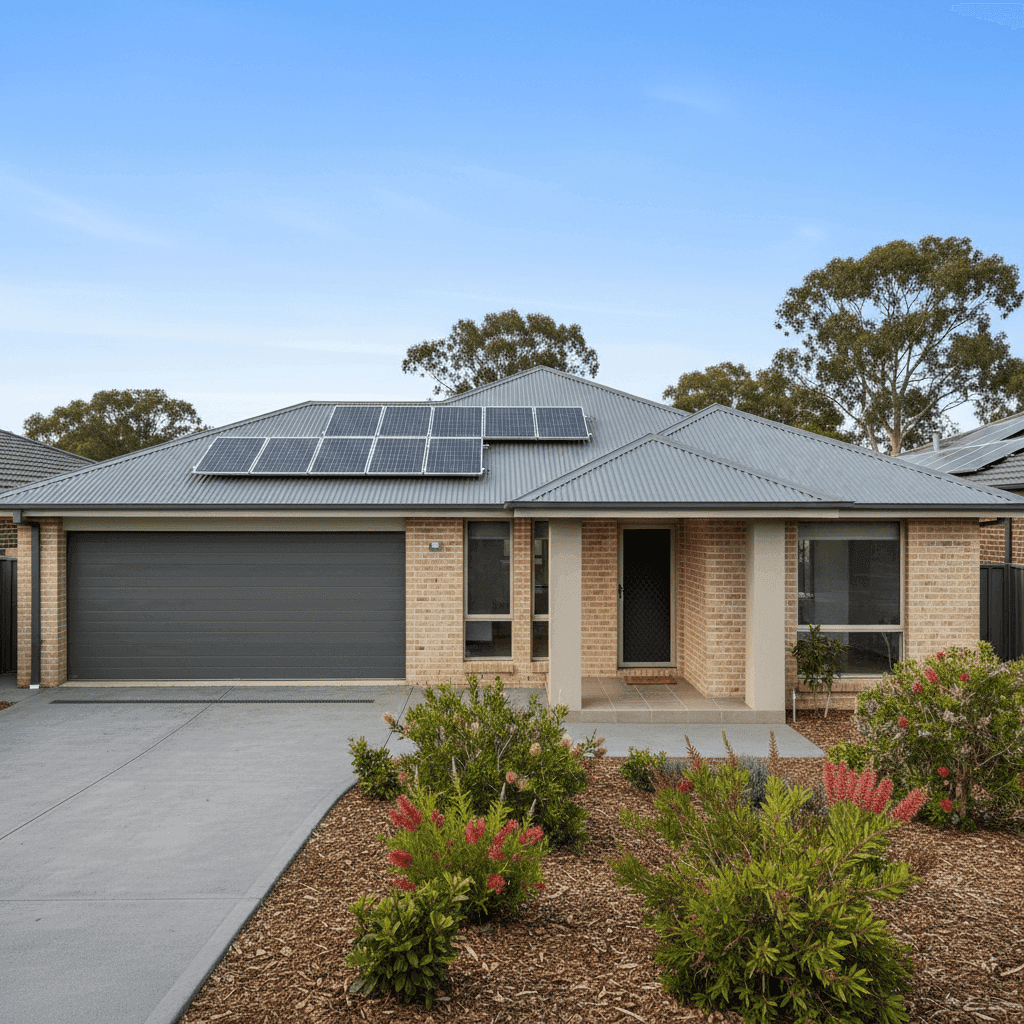

Brick Veneer Construction Brick veneer is one of the most common external wall types in Australian suburban homes and is generally viewed favourably by insurers. It offers solid fire resistance and durability, which can help moderate premiums compared to timber-framed or weatherboard homes.

Steel/Colorbond Roof Colorbond steel roofing is highly regarded in the insurance industry. It's lightweight, resistant to fire, and holds up well in storms — all factors that reduce claim risk. Homes with older tile roofs or fibrous cement sheeting often attract higher premiums, so this is a genuine advantage.

Slab Foundation A concrete slab foundation is considered low-risk from an insurance standpoint. There's no subfloor cavity to worry about, no elevated floor susceptible to storm surge or pest damage, and slab homes tend to be structurally straightforward to assess and repair.

Solar Panels This property has solar panels installed, which does add a small amount to the insured value and can influence premiums marginally. It's important to ensure your building sum insured accounts for the replacement cost of the solar system — many homeowners overlook this.

Ducted Climate Control Ducted air conditioning systems are a meaningful asset and contribute to the overall replacement cost of the home. Insurers factor in the cost of reinstating these systems when assessing building cover, so having an accurate sum insured is important.

No Pool, No Cyclone Risk The absence of a swimming pool removes a common source of liability and maintenance-related claims. And because Metford is not in a designated cyclone risk area, the premium doesn't carry the uplift that coastal Queensland or northern WA properties often face.

2004 Construction Homes built in 2004 benefit from construction standards that were already well-developed under the Building Code of Australia. This vintage is generally seen as lower risk than older homes built before modern standards, particularly around electrical systems and structural requirements.

---

Tips for Homeowners in Metford

1. Review Your Building Sum Insured Regularly At $619,000, the building sum insured needs to reflect the full cost of rebuilding — not the market value of the property. Construction costs have risen sharply in recent years across NSW, so it's worth reassessing your sum insured annually to avoid being underinsured. Don't forget to factor in your solar panels and ducted air conditioning.

2. Consider Raising Your Excess to Lower Your Premium Both the building and contents excess on this policy sit at $1,000. If you have a solid emergency fund and are unlikely to make small claims, increasing your excess to $1,500 or $2,000 could reduce your annual premium meaningfully. Just make sure the saving justifies the extra out-of-pocket cost if you do need to claim.

3. Bundle and Compare Home and contents insurance is already bundled here, which typically delivers better value than purchasing the two covers separately. That said, it's still worth comparing quotes from multiple insurers at renewal time. Loyalty doesn't always pay in insurance — switching providers or negotiating can sometimes yield significant savings.

4. Keep Your Home Well-Maintained Insurers look more favourably on well-maintained properties, and some may ask about the condition of your roof, gutters, and plumbing at the time of quoting. A Colorbond roof in good condition is an asset — keep gutters clear and address any wear promptly to avoid issues at claim time.

---

Compare Your Own Quote at CoverClub

Whether you're renewing soon or just curious about where you stand, it pays to compare. At CoverClub, you can enter your property details and see how your current premium stacks up against real quotes from across Australia. It takes minutes and could save you hundreds. Don't settle for "fair" when "great value" might be just a comparison away.