If you own a free standing home in Miepoll, VIC 3666, you're likely no stranger to the rolling rural landscape of the Murrindindi local government area. It's a quiet, semi-rural pocket of Victoria — and like many properties in regional Victoria, the cost of insuring your home can vary considerably depending on your property's features, age, and the level of cover you choose.

This article breaks down a real home and contents insurance quote for a three-bedroom, two-bathroom free standing home in Miepoll, comparing it against local, state, and national benchmarks to help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

The annual premium for this property comes in at $2,280 per year (or $223/month), covering both building (sum insured: $507,000) and contents ($80,000). Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner.

To put that in context: the Victorian state average for home insurance sits at $3,000 per year, with a median of $2,718. This quote comes in roughly $438 below the state median and $720 below the state average — a meaningful saving on an annual basis.

At the national level, the picture is even more striking. The national average premium is $5,347/yr, with a national median of $2,764. This quote sits well below both figures, suggesting the property and its location present a relatively low risk profile to insurers.

The building excess is set at $2,000 and the contents excess at $1,000 — both fairly standard for Australian home insurance policies. Higher excesses are one way to keep premiums down, so it's worth checking whether these levels suit your financial situation.

---

How Miepoll Compares

One of the more telling data points here is the Murrindindi LGA average premium of $4,184 per year — significantly higher than what this particular quote is offering. That's a gap of nearly $1,900 annually, which suggests this homeowner is well-positioned relative to many of their neighbours in the broader LGA.

For suburb-level statistics on Miepoll, granular data is limited given the area's small population, but the LGA and state comparisons paint a useful picture. Regional and semi-rural Victoria can attract higher premiums due to factors like bushfire exposure, limited emergency services access, and the higher cost of rebuilding in areas with less local trade infrastructure. The fact that this quote beats both the state and LGA averages is a positive indicator.

Here's a quick summary of where this quote sits:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,280 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| Murrindindi LGA Average | $4,184 |

| National Average | $5,347 |

| National Median | $2,764 |

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium — some favourably, others less so.

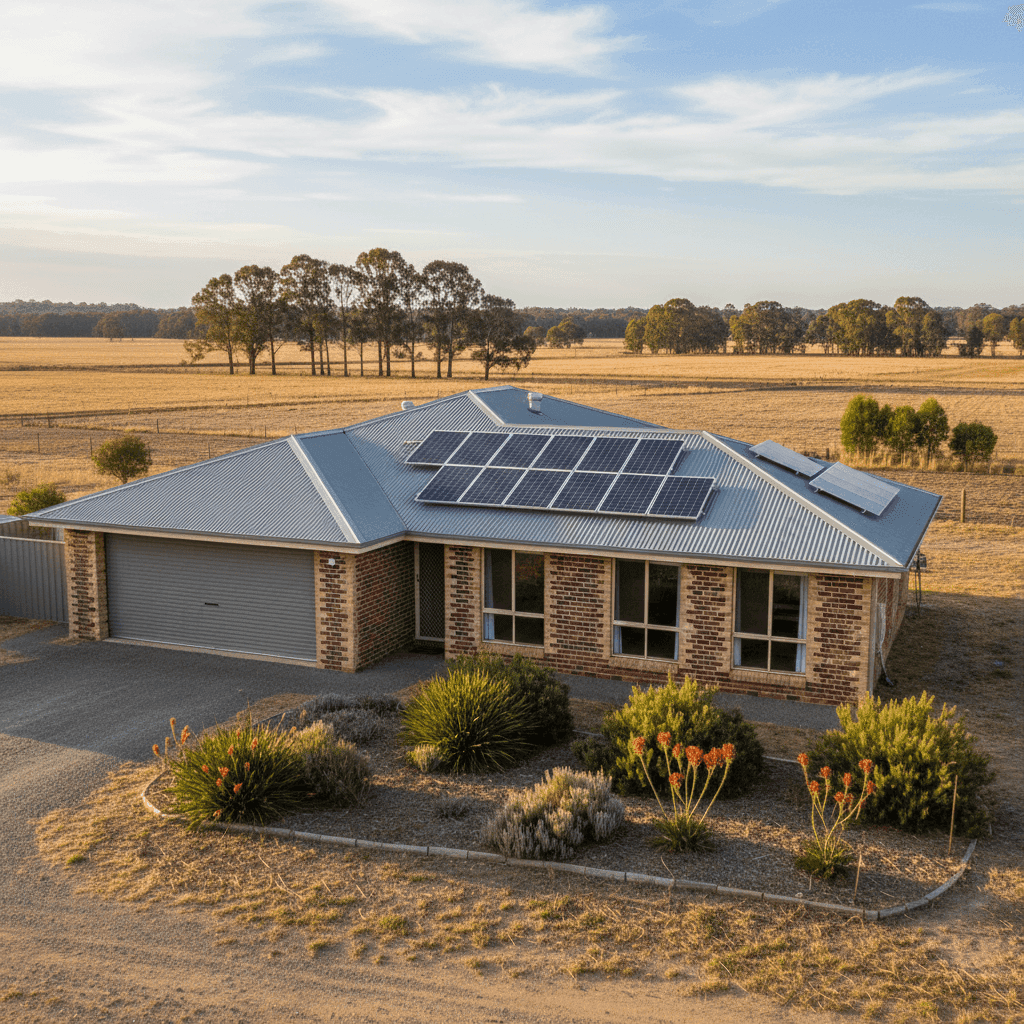

Brick veneer construction is generally viewed positively by insurers. It offers solid fire resistance and structural durability compared to weatherboard or timber-clad homes, which can be more vulnerable in bushfire-prone areas. Combined with a steel/Colorbond roof, which is durable and low-maintenance, the construction profile of this home is relatively insurer-friendly.

The stump foundation is worth noting. Homes on stumps (as opposed to concrete slabs) can be more susceptible to movement, pest damage, and moisture-related issues over time — particularly in older properties. This home was built in 1980, which means it's over 40 years old. Older homes can attract slightly higher premiums due to the increased likelihood of wear and the cost of sourcing period-appropriate materials for repairs.

Timber and laminate flooring is a common feature in homes of this era and generally doesn't significantly impact premiums, though it's a consideration for contents cover when assessing replacement costs.

On the plus side, solar panels are installed on this property. While solar panels add some replacement cost to a building sum insured, many insurers now factor them in as a standard feature. The ducted climate control system is another fixed asset that contributes to the building's insured value — and at $507,000, the sum insured appears to reflect these inclusions appropriately.

There is no pool on the property, which removes a common source of liability and maintenance risk that can nudge premiums upward.

---

Tips for Homeowners in Miepoll

1. Review your sum insured regularly Building costs in regional Victoria have risen significantly in recent years. Make sure your $507,000 sum insured reflects current rebuild costs — not just the market value of the land. Underinsurance is one of the most common and costly mistakes Australian homeowners make.

2. Consider your bushfire preparedness The Murrindindi region has experienced significant bushfire events historically. Even if your specific property isn't classified as a high-risk zone, maintaining a defensible space around your home, clearing gutters, and using ember-resistant materials can all reduce your risk — and may be recognised by some insurers.

3. Check what's included for solar panels and ducted systems Not all policies automatically cover solar panel systems or ducted air conditioning under building cover. Confirm with your insurer that these fixed assets are explicitly included in your policy wording, and that the sum insured accounts for their replacement value.

4. Compare before you renew Even if this quote is below average today, premiums can shift significantly at renewal. Insurers regularly adjust their pricing based on claims data, reinsurance costs, and local risk assessments. Using a comparison tool like CoverClub at renewal time ensures you're not quietly paying more than you need to.

---

Get a Quote for Your Miepoll Home

Whether you're a first-time buyer or a long-time Miepoll resident reviewing your existing cover, it pays to compare. CoverClub makes it easy to see how your current premium stacks up — and whether there's a better deal waiting for you. Enter your address at CoverClub to get started and see real quotes tailored to your property.