Moama is a popular riverside town on the New South Wales side of the Murray River, known for its relaxed lifestyle, proximity to Echuca, and a growing community of owner-occupiers and retirees. If you own a free standing home in this postcode, understanding what you should be paying for home and contents insurance — and whether your current policy stacks up — is well worth your time.

This article breaks down a real insurance quote for a three-bedroom, two-bathroom brick veneer home in Moama (NSW 2731), compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

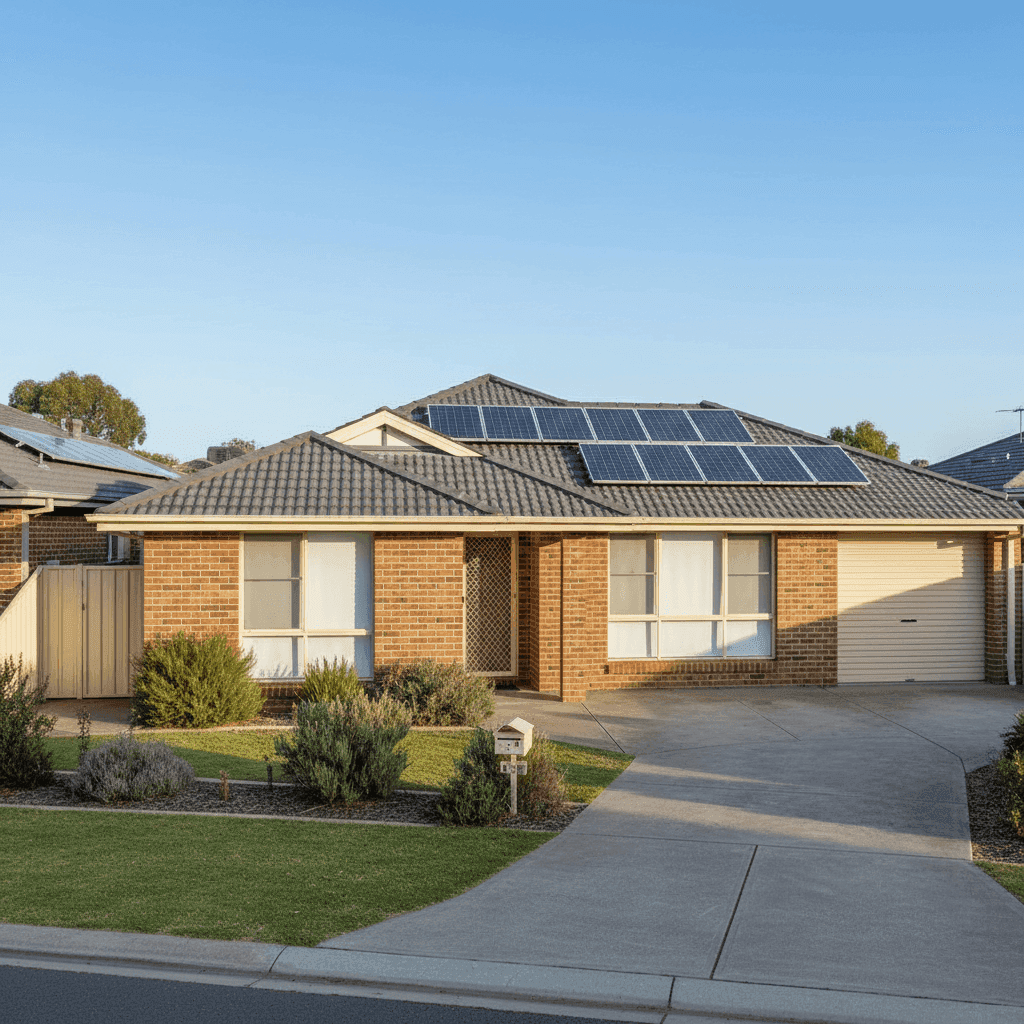

The annual premium for this property came in at $1,608 per year (or roughly $154 per month), covering both building ($542,000 sum insured) and contents ($65,000), each with a $1,000 excess.

Our pricing engine rates this quote as CHEAP — below average for the area. That's genuinely good news. Based on data from 58 quotes collected for Moama and the surrounding 2731 postcode, the suburb median sits at $3,530 per year — meaning this quote comes in at less than half the typical price paid by local homeowners. Even against the 25th percentile (the cheapest quarter of quotes), which sits at $2,376 per year, this premium still undercuts the market meaningfully.

For a property of this size and specification, a sub-$1,700 annual premium represents solid value — particularly when building cover alone is set at over half a million dollars.

---

How Moama Compares

Moama's insurance pricing landscape is worth understanding before you accept any quote at face value.

| Benchmark | Premium |

|---|---|

| This Quote | $1,608/yr |

| Moama (2731) Median | $3,530/yr |

| Moama (2731) Average | $40,221/yr |

| Moama 25th Percentile | $2,376/yr |

| Moama 75th Percentile | $4,564/yr |

| Murray River LGA Average | $24,396/yr |

| NSW State Median | $3,770/yr |

| NSW State Average | $9,528/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

A few things stand out here. The Moama suburb average of $40,221 per year is extraordinarily high — almost certainly skewed upward by a small number of very expensive quotes, possibly for properties with elevated flood risk near the Murray River. The median of $3,530 is a far more reliable indicator of what most homeowners in the area actually pay, and it's that figure you should be benchmarking against.

Compared to the NSW state median of $3,770 and the national median of $2,764, Moama sits in a broadly comparable range — though the elevated LGA average for Murray River ($24,396) signals that flood-exposed properties in the region can attract dramatically higher premiums.

This quote, at $1,608, sits well below every one of these benchmarks, which suggests the property's characteristics and insurer selection are working in the owner's favour.

---

Property Features That Affect Your Premium

Several features of this home likely contribute to its competitive premium:

Brick Veneer Walls Brick veneer is one of the more insurer-friendly external wall types in Australia. It offers solid fire resistance and durability, which typically translates to lower rebuild risk in the eyes of underwriters compared to timber or cladding-clad homes.

Tiled Roof A tiled roof is considered a low-risk roofing material — it performs well in hail and is less susceptible to fire spread than Colorbond or corrugated iron in some scenarios. Combined with brick veneer walls, this property presents a relatively conventional and well-regarded construction profile.

Concrete Slab Foundation Slab foundations are standard across much of regional NSW and are generally viewed favourably by insurers, particularly in areas without significant subsidence or reactive soil concerns.

Built in 2000 A home built around the turn of the millennium benefits from modern building codes without the age-related risks associated with older properties (such as outdated wiring or plumbing). It's a sweet spot for insurers — not too old, not a new build with unknown defects.

Solar Panels This property has solar panels installed, which can add modest complexity to a building claim (panels are generally covered under building insurance). However, they're increasingly common and most mainstream insurers factor them into standard building cover without significant premium loading.

Ducted Climate Control Ducted air conditioning systems are a notable inclusion in a building sum insured calculation. At $542,000, the building cover here should adequately account for this fixed asset, which is important — underinsurance is a real risk when high-value fixtures are overlooked.

No Pool The absence of a swimming pool removes a common source of liability and maintenance-related claims, which can contribute to a cleaner risk profile.

139 sqm Floor Area, Standard Fittings At 139 square metres with standard-grade fittings, this home sits in a manageable rebuild cost range. The $542,000 sum insured equates to roughly $3,900 per square metre — a reasonable figure for regional NSW when factoring in site costs, labour, and the full scope of a rebuild.

---

Tips for Homeowners in Moama

1. Check Your Flood Coverage Carefully Moama's proximity to the Murray River means flood is a genuine consideration for many properties in the area — even those that haven't flooded historically. When comparing policies, confirm whether flood cover is included as standard or available as an optional add-on, and check the insurer's flood mapping for your specific address. Not all "storm" cover includes riverine flooding.

2. Don't Confuse the Suburb Average with What You Should Pay As the data above shows, Moama's average premium is dramatically inflated by high-risk outlier properties. Don't assume you need to pay anywhere near $40,000 per year — most homeowners in the suburb pay closer to $3,500, and well-constructed homes with lower risk profiles can do significantly better.

3. Review Your Sum Insured Annually Construction costs in regional NSW have risen considerably in recent years. If your building sum insured hasn't been reviewed since you took out the policy, there's a real chance you're underinsured. Use a building cost calculator or speak with a quantity surveyor to sense-check your coverage amount — particularly if you've made improvements or added fixtures like solar panels or ducted systems.

4. Compare Before You Renew Insurers rarely reward loyalty with their best pricing. When your renewal notice arrives, take 10 minutes to run a fresh quote at CoverClub and see how your current premium compares. The market moves, and so do the best deals.

---

Find Your Best Rate with CoverClub

Whether you're a first-time buyer in Moama or a long-term homeowner wondering if you're paying too much, CoverClub makes it easy to see where your premium sits against the market. Compare home and contents insurance quotes today and find out if you're getting the value you deserve. You can also explore detailed pricing data for Moama and the 2731 postcode or browse NSW-wide insurance trends to get a fuller picture.