If you own a free standing home in Molesworth, TAS 7140, you're likely no stranger to the unique considerations that come with insuring a property in regional Tasmania. Between the cool climate, rural surroundings, and the sheer cost of rebuilding a sizeable home, getting the right home and contents insurance at a fair price matters more than most people realise.

This article breaks down a real insurance quote for a five-bedroom, two-bathroom free standing home in Molesworth — examining whether the premium is competitive, how it stacks up against local and national benchmarks, and what property features are likely driving the cost.

---

Is This Quote Fair?

The annual premium for this quote comes in at $2,940 per year (or $288 per month), covering both building and contents for a home insured at $842,000 for the building and $85,000 for contents.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a meaningful finding. With a building excess of $3,000 and a contents excess of $1,000, the insurer has structured this policy with higher out-of-pocket costs in the event of a claim, which is a common way to reduce the upfront premium. Homeowners should weigh that trade-off carefully — a lower annual premium can be excellent value if you rarely claim, but it's worth having a financial buffer to cover that excess if something does go wrong.

For a property of this size and value, a sub-$3,000 annual premium is genuinely competitive. The sum insured for the building alone is substantial at $842,000, reflecting the true cost of rebuilding a five-bedroom home in today's construction environment.

---

How Molesworth Compares

To put this quote in context, here's how the $2,940 premium sits against available benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $2,940/yr |

| Molesworth suburb average | $3,299/yr |

| Molesworth suburb median | $3,431/yr |

| Molesworth 25th percentile | $3,006/yr |

| Molesworth 75th percentile | $3,545/yr |

| TAS state average | $2,458/yr |

| TAS state median | $2,272/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| West Coast LGA average | $3,729/yr |

A few things stand out here. This quote sits below the suburb average by around $359 per year and is even cheaper than the suburb's 25th percentile of $3,006 — meaning it's among the most competitively priced quotes seen in this area. You can explore more local pricing data on the Molesworth suburb stats page.

Interestingly, this quote is slightly above the Tasmanian state average of $2,458, which reflects the fact that Molesworth sits within the West Coast LGA — one of Tasmania's more expensive areas to insure, with an LGA average of $3,729 per year. Remoteness, limited emergency services access, and longer rebuild times in regional areas all contribute to higher base premiums across this LGA, making this quote look even more favourable by comparison.

Against the national average of $2,965, this quote is essentially on par — a solid result for a large five-bedroom home with a high sum insured.

---

Property Features That Affect Your Premium

Several characteristics of this property influence what insurers charge. Here's a look at the key factors at play:

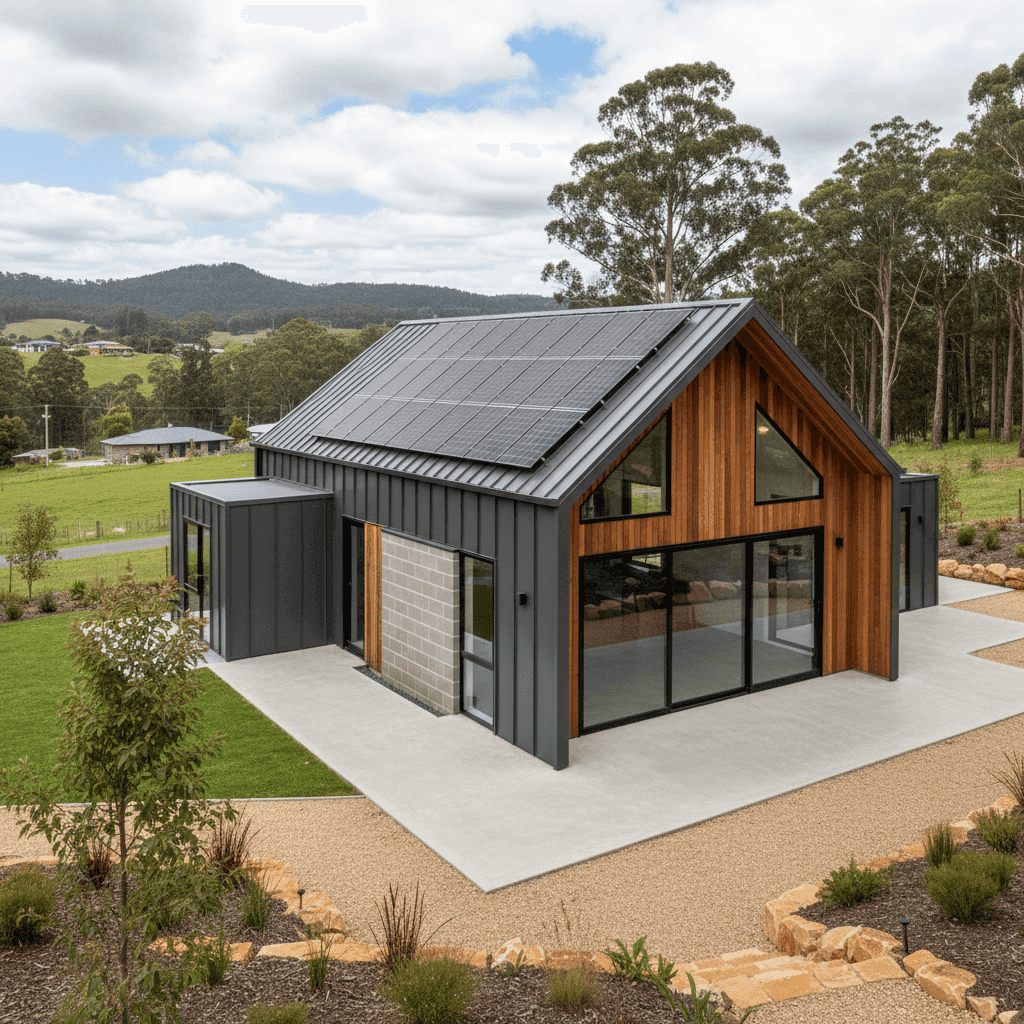

Steel/Colorbond Roof Colorbond roofing is generally viewed favourably by insurers. It's durable, fire-resistant, and performs well in harsh weather conditions — all of which reduce the likelihood of a claim. This is likely contributing positively to the premium outcome.

Slab Foundation A concrete slab foundation is considered one of the more stable and low-risk foundation types. Unlike older homes with timber stumps or suspended floors, slab homes are less susceptible to subsidence and pest-related structural damage, which insurers tend to reward with more competitive pricing.

Construction Year: 2010 A home built in 2010 is relatively modern and would have been constructed to contemporary building codes. Newer builds typically attract lower premiums than older homes, as they're less likely to have ageing electrical systems, plumbing issues, or structural deterioration.

Solar Panels The presence of solar panels adds some complexity to a home insurance policy. Panels represent an additional asset on the roof that needs to be covered — both for damage to the panels themselves and for any liability if they cause issues. It's worth confirming with your insurer exactly how solar panels are treated under your policy, as coverage can vary.

Building Size: 130 sqm At 130 square metres, this is a modestly sized footprint for a five-bedroom home, which may suggest an efficient or multi-storey layout. The sum insured of $842,000 accounts for full rebuild costs, which in Tasmania's regional areas can be significantly higher than metropolitan centres due to material and labour transport costs.

No Pool, No Ducted Climate Control The absence of a swimming pool removes a notable liability risk that often increases premiums. Similarly, no ducted climate control system means fewer complex mechanical components that could fail and cause water or fire damage.

Contents: $85,000 The contents cover of $85,000 is a reasonable figure for a five-bedroom home with standard fittings. It's worth doing a thorough home inventory periodically to ensure this figure remains accurate — underinsurance is one of the most common and costly mistakes homeowners make.

---

Tips for Homeowners in Molesworth

1. Review your sum insured regularly Construction costs in Tasmania have risen significantly in recent years. The $842,000 building sum insured should be reviewed annually to ensure it reflects current rebuild costs. Many insurers offer index-linked policies that adjust automatically, but it's still good practice to verify this with your provider.

2. Understand your excess structure This policy carries a $3,000 building excess and a $1,000 contents excess. Before renewing or switching policies, think about your claims history and risk tolerance. If you'd struggle to cover a $3,000 excess out of pocket, it may be worth comparing policies with a lower excess — even if the annual premium is slightly higher.

3. Confirm solar panel coverage With solar panels on the roof, ask your insurer specifically: Are the panels covered for accidental damage? What happens if a panel causes a fire or roof damage? Are they included in the building sum insured or listed as a separate item? Getting clear answers now avoids nasty surprises at claim time.

4. Compare quotes at least annually Insurance markets shift, and loyalty doesn't always pay. Given that this quote is already below the suburb average, it's a good benchmark to beat — but running a fresh comparison each year ensures you're not paying more than you need to. Even a $200–$300 saving per year adds up over time.

---

Ready to Compare Home Insurance in Molesworth?

Whether you're renewing your existing policy or shopping for the first time, comparing multiple quotes is the smartest way to make sure you're getting genuine value. At CoverClub, we make it easy to see how your premium stacks up and find competitive options tailored to your property. Get a home insurance quote today and see what's available for your Molesworth home.