Nestled in the Dandenong Ranges east of Melbourne, Monbulk is a leafy semi-rural suburb known for its large blocks, established gardens, and a strong sense of community. It's also the kind of location where home insurance deserves careful attention — and for good reason. This article breaks down a real home and contents insurance quote for a six-bedroom free standing home in Monbulk (VIC 3793), compares it against local, state, and national benchmarks, and offers practical guidance for homeowners in the area.

---

Is This Quote Fair?

The quote in question comes in at $3,083 per year (or $295/month) for combined home and contents cover, with a building sum insured of $795,000 and contents valued at $120,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, which is an accurate reflection when you look at the numbers in context. The quote sits just 4.3% below the suburb average of $3,221/year for Monbulk, and it's modestly above the suburb median of $2,718/year. That gap between average and median tells an important story: a handful of higher-priced quotes are pulling the average up, meaning many Monbulk homeowners are paying closer to $2,718 — but a significant portion are also paying well above $3,000.

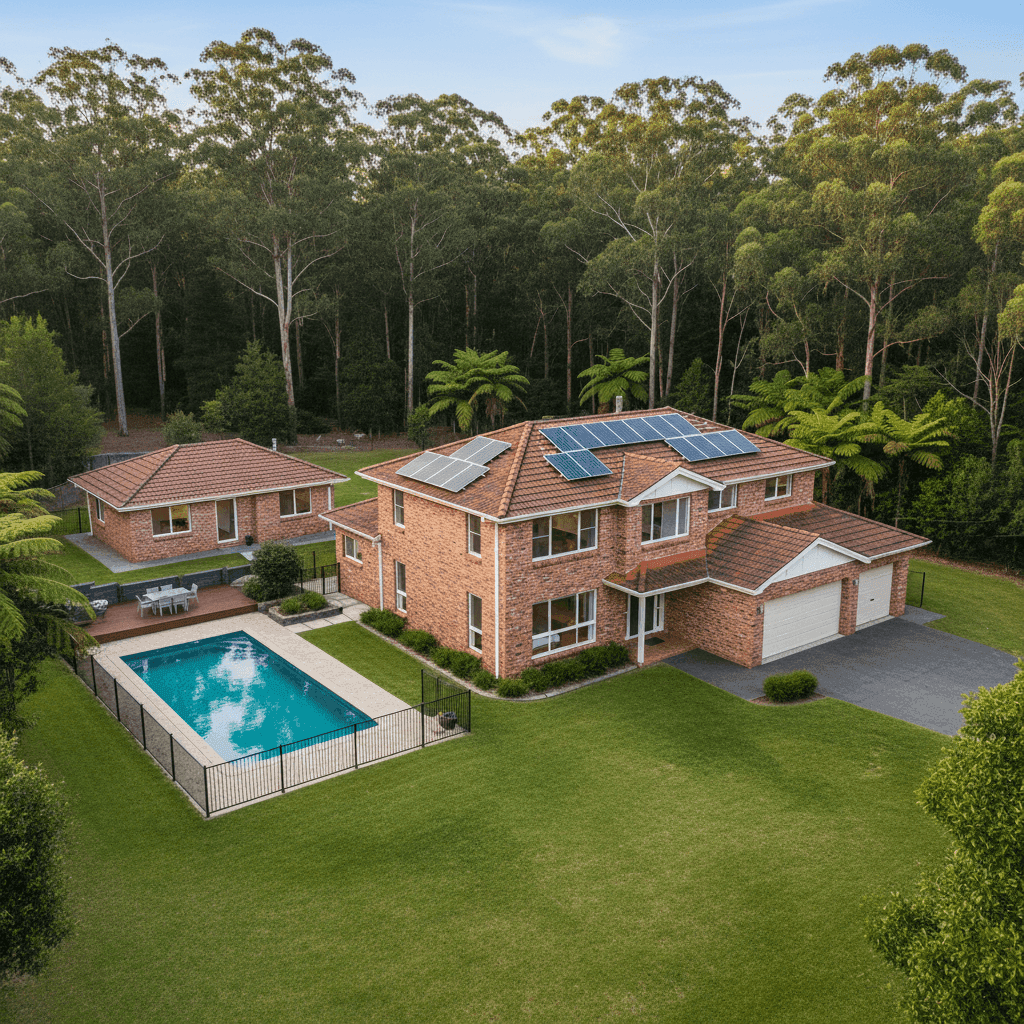

At $3,083, this quote is comfortably within what you'd expect for a property of this size and complexity. It's not a bargain, but it's not overpriced either — and for a 286 sqm home on stumps with a pool, solar panels, granny flat, and ducted climate control, there are legitimate reasons the premium sits where it does.

---

How Monbulk Compares

Understanding where your premium sits relative to broader benchmarks helps put the "fair" rating into sharper focus. Here's how Monbulk stacks up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,083 |

| Monbulk Suburb Average | $3,221 |

| Monbulk Suburb Median | $2,718 |

| Monbulk 25th Percentile | $2,070 |

| Monbulk 75th Percentile | $4,024 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

| Yarra Ranges LGA Average | $5,600 |

(Based on [35 quotes collected for Monbulk](https://coverclub.com.au/stats/VIC/3793/monbulk). View [VIC state stats](https://coverclub.com.au/stats/VIC) or [national stats](https://coverclub.com.au/stats/national).)

A few things stand out here. First, this quote is almost exactly in line with the VIC state average of $3,000/year — suggesting the insurer is pricing this property similarly to a typical Victorian home, despite Monbulk's elevated bushfire risk profile. Second, the quote is dramatically below the national average of $5,347/year, which is heavily influenced by high-risk regions in Queensland, WA, and Northern Australia where cyclone and flood premiums push costs skyward.

Perhaps most striking is the comparison to the Yarra Ranges LGA average of $5,600/year. This quote comes in at nearly half that figure — a meaningful difference that likely reflects the specific insurer's risk appetite, the property's brick veneer construction (which performs better in bushfire scenarios than timber), and the tiled roof. Homeowners in the broader LGA should be aware that premiums can vary enormously depending on exact location and property characteristics.

---

Property Features That Affect Your Premium

Several aspects of this property have a direct bearing on the insurance cost — both upward and downward.

Building age and construction (1968, Brick Veneer, Tiles): A home built in 1968 is over 55 years old, which can raise concerns for insurers around ageing plumbing, wiring, and structural integrity. However, brick veneer walls and a tiled roof are generally viewed favourably — they offer solid fire resistance and durability compared to weatherboard or Colorbond alternatives.

Stumped foundation: Homes on stumps are common in the Dandenong Ranges and can be more vulnerable to movement and moisture-related damage over time. Some insurers apply a loading for this foundation type, particularly with older homes where original timber stumps may not have been replaced.

Pool and granny flat: Both add to the insured value and the insurer's liability exposure. A pool introduces risk of injury and water damage, while a granny flat effectively increases the dwelling footprint and replacement cost — both factors that justify a higher premium.

Solar panels: Rooftop solar adds replacement value to the building sum insured and can also introduce risks around electrical faults or storm damage. Most insurers include solar panels under building cover, but it's worth confirming this explicitly in your policy documents.

Ducted climate control: Large-scale HVAC systems are expensive to repair or replace, and their inclusion in the building sum insured of $795,000 is appropriate for a 286 sqm home of this specification.

Bushfire proximity: Monbulk is situated within a Bushfire Management Overlay area. While this property is not in a cyclone risk zone, the surrounding vegetation and terrain mean bushfire risk is a genuine consideration — and one that insurers price carefully in this region.

---

Tips for Homeowners in Monbulk

1. Review your building sum insured annually. Construction costs have risen sharply in recent years. A 286 sqm home with standard fittings, a pool, and a granny flat could cost significantly more than $795,000 to rebuild today — especially in a regional area where trades and materials carry a premium. Use a building cost calculator or speak with a local builder to sense-check your sum insured each year.

2. Confirm your granny flat and solar panels are explicitly covered. Not all policies automatically extend full cover to secondary dwellings or rooftop solar. Read the Product Disclosure Statement (PDS) carefully, and ask your insurer directly whether the granny flat is included under the building definition and whether solar panels are covered for accidental damage and storm events.

3. Take bushfire preparedness seriously — it can affect your cover. Some insurers in high-risk bushfire areas require homeowners to maintain defensible space around the property. Keeping gutters clear, maintaining ember guards, and following local CFA guidelines not only reduces your risk but may also support your claim if the worst happens.

4. Shop around at renewal time. This quote is rated fair, but the 25th percentile for Monbulk is $2,070/year — meaning roughly a quarter of comparable quotes come in below that figure. If your renewal notice arrives and the premium has crept up, it's worth getting at least two or three competing quotes before accepting it.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new purchase, CoverClub makes it easy to see how your quote stacks up. Get a home insurance quote today and compare it against real data from your suburb, your state, and across Australia — so you can make a confident, informed decision.