Monkland is a quiet residential suburb in Queensland's Gympie region, known for its relaxed lifestyle and mix of older character homes. If you own a free-standing home here — particularly one of the weatherboard classics built in the mid-twentieth century — understanding what you should be paying for home and contents insurance is genuinely useful. This article breaks down a real quote for a 3-bedroom, 2-bathroom property in Monkland (postcode 4570) and puts it in context against suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,373 per year (or roughly $323 per month) for combined home and contents cover, with a building sum insured of $650,000 and contents valued at $50,000. The building excess sits at $1,000 and the contents excess at $500.

Our price rating for this quote is FAIR — Around Average, which is a reasonable outcome for a property of this age and construction type in regional Queensland.

To put that in perspective: the suburb median for Monkland is $3,270 per year, meaning this quote sits just slightly above the midpoint of what others in the area are paying. It's comfortably below the suburb average of $3,938 and well within the interquartile range of $2,865 to $5,076. In other words, this isn't a bargain, but it's not an outlier either — it's a solid, market-rate premium.

---

How Monkland Compares

One of the most striking things about this quote is how it stacks up against broader benchmarks. Queensland is one of Australia's most expensive states for home insurance, largely driven by extreme weather risks in northern and coastal areas. The Queensland state average premium is a hefty $9,129 per year, though the state median of $3,903 is far more representative of what most Queenslanders actually pay — the average is pulled up sharply by high-risk postcodes in cyclone-prone regions.

At $3,373, this Monkland quote sits below both the QLD state average and the state median, which is a positive sign. It also compares favourably to the national average of $5,347, though it's somewhat above the national median of $2,764.

Within the Fraser Coast LGA, the average premium is $4,810 per year — so this quote is notably cheaper than the broader local government area average, suggesting Monkland itself benefits from relatively lower risk pricing compared to some surrounding areas.

You can explore more detailed local data on the Monkland suburb stats page.

> Note: The suburb comparison is based on a sample of 10 quotes, so treat these figures as indicative rather than definitive. As more data is collected, the benchmarks will become increasingly reliable.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on the premium quoted.

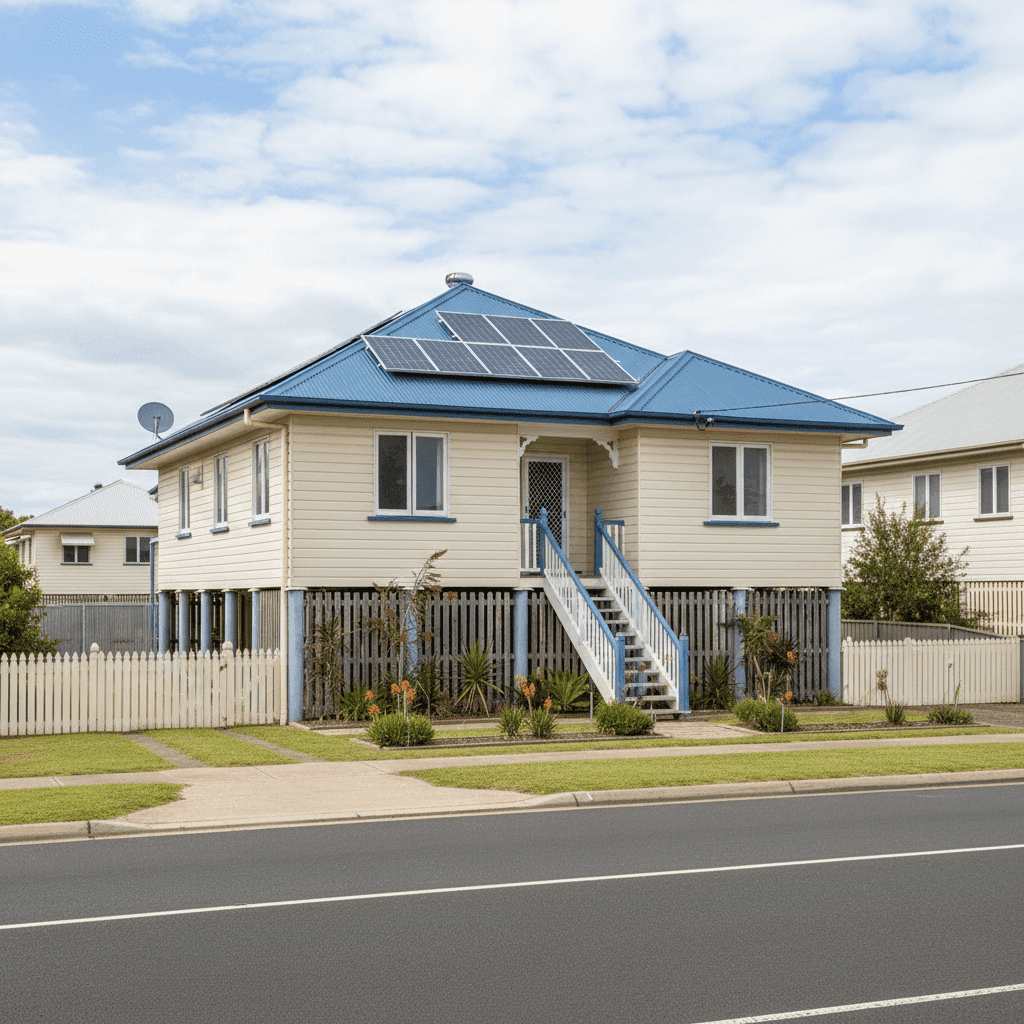

Age and Construction (1962, Weatherboard)

Built in 1962, this home is over 60 years old. Older properties typically attract higher premiums because ageing materials — particularly timber weatherboard walls — can be more susceptible to damage and more expensive to repair or replace to modern building standards. That said, weatherboard homes are common in Gympie and surrounds, so insurers operating in this market are well-acquainted with the risk profile.

Roof Type: Steel/Colorbond

A Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in storms compared to older roofing materials like terracotta tiles or corrugated iron. This is likely a positive factor in keeping the premium from being higher.

Stumps Foundation

Homes on stumps (also called timber or concrete stumps) are very common in Queensland's older housing stock. They offer good ventilation and can handle certain ground movement better than slab foundations, but they do introduce some risk around subfloor maintenance and potential pest damage. Insurers factor this in, particularly for homes of this vintage.

Solar Panels

This property has solar panels installed. While solar adds value and reduces energy costs, it also adds to the replacement cost of the building — which is reflected in the $650,000 sum insured. Make sure your policy explicitly covers solar panels as part of the building, and check whether the insurer covers damage to the panels themselves (e.g., from hail or storm).

Ducted Climate Control

Ducted air conditioning is a significant fixed asset and contributes to the overall building replacement value. It's worth confirming with your insurer that the ducted system is included under building cover rather than contents, as this can vary between policies.

No Pool, No Cyclone Risk

The absence of a swimming pool removes a common liability risk factor, and the property falling outside a designated cyclone risk zone is a meaningful premium advantage — particularly relevant given Queensland's reputation for tropical weather events further north.

---

Tips for Homeowners in Monkland

1. Review your sum insured regularly At $650,000, the building sum insured needs to genuinely reflect what it would cost to rebuild the home from scratch — including demolition, materials, labour, and professional fees. Construction costs have risen significantly in recent years, so a figure set a few years ago may no longer be adequate. Consider using a building cost calculator or speaking to a quantity surveyor.

2. Don't overlook the age of your home's wiring and plumbing A 1962 weatherboard home may have original or partially updated electrical wiring and plumbing. Some insurers ask about this directly, and undisclosed outdated systems can affect your ability to make a claim. It's worth having these inspected and updated where necessary — both for safety and insurability.

3. Protect your stumps Subfloor maintenance is easy to ignore but important in Queensland's humid climate. Timber stumps can be vulnerable to termites and rot. Regular pest inspections and ensuring good subfloor ventilation can prevent costly damage that may not always be covered under a standard home insurance policy.

4. Compare quotes at renewal time A "fair" rating means you're paying around the market rate — but that doesn't mean you can't do better. Insurance premiums can vary significantly between providers for the same property. Using a comparison tool at renewal is one of the simplest ways to ensure you're not paying more than you need to.

---

Ready to Compare?

Whether you're looking to benchmark your current policy or find a better deal, CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Get a quote today and see how your premium stacks up against your neighbours.