Nestled in the lush hinterland of the Sunshine Coast, Montville is one of Queensland's most picturesque villages — known for its cool-climate charm, tree-lined streets, and heritage cottages. But owning a home here comes with its own set of insurance considerations. This article breaks down a real home and contents insurance quote for a four-bedroom free standing home in Montville QLD 4560, helping you understand whether the premium is competitive and what factors are driving the cost.

---

Is This Quote Fair?

The annual premium for this property comes in at $4,166 per year (or $392/month), covering a building sum insured of $691,000 and contents valued at $222,000, each with a $1,000 excess.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average for Montville sits at $4,255 per year, meaning this quote comes in just $89 below the local average — a modest but welcome saving. It also falls comfortably within the interquartile range for the suburb (between the 25th percentile of $3,101/yr and the 75th percentile of $4,665/yr), which tells us this is a mainstream, reasonable price rather than an outlier in either direction.

That said, "fair" doesn't necessarily mean "the best available." There's a meaningful gap between this quote and the suburb's 25th percentile — homeowners who shop around actively can potentially find cover closer to $3,100/yr for a comparable property. It's worth remembering that insurers price risk differently, and a few extra minutes comparing quotes can translate into hundreds of dollars in annual savings.

---

How Montville Compares

Understanding where Montville sits in the broader insurance landscape is useful context when evaluating any quote. Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Montville (4560) | $4,255/yr | $3,850/yr |

| Sunshine Coast LGA | $7,249/yr | — |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, Montville's average premium is dramatically lower than the Queensland state average of $9,129/yr. This is largely because QLD's state average is heavily skewed by high-risk coastal and cyclone-prone areas — think Far North Queensland and parts of the Gulf. The median tells a more balanced story: Queensland's median of $3,903/yr is actually quite close to Montville's median of $3,850/yr, suggesting the suburb sits roughly in the middle of the pack for the state when extreme outliers are removed.

Compared to the national average of $5,347/yr, this quote looks even more reasonable. However, the national median of $2,764/yr is a reminder that homeowners in lower-risk states (particularly Victoria and South Australia) often pay significantly less.

For a deeper dive into local pricing trends, visit the Montville suburb insurance stats page, or explore broader Queensland home insurance data and national benchmarks.

---

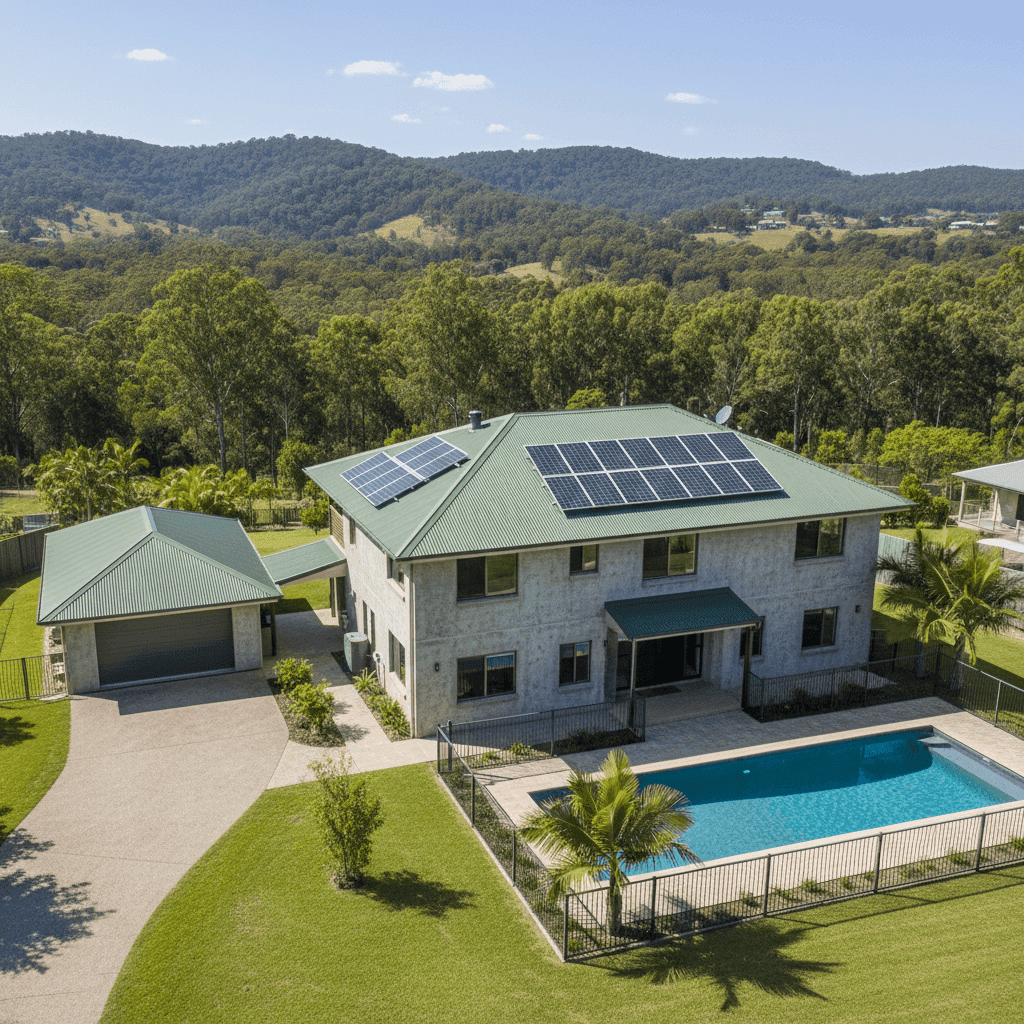

Property Features That Affect Your Premium

This particular property has a number of characteristics that insurers weigh carefully when calculating risk. Here's how each feature is likely influencing the premium:

Concrete External Walls Concrete construction is generally viewed favourably by insurers. It's more resistant to fire, rot, and storm damage than timber weatherboard, which can help moderate the premium compared to less durable wall materials.

Steel/Colorbond Roof A Colorbond steel roof is one of the better roof types from an insurance perspective. It's durable, resistant to cracking and leaking, and performs well in high-wind events. This is a positive factor for pricing.

Stump Foundation The home sits on stumps, which is common for older Queensland properties built in the pre-1980s era. While stumps can introduce some risk around structural movement and pest damage (particularly in hinterland environments with moisture), they also elevate the home above ground — providing some protection from localised flooding.

Construction Year: 1975 At roughly 50 years old, this home is considered an older property. Insurers factor in the age of a dwelling when assessing the likelihood of claims related to ageing plumbing, electrical systems, and structural wear. Older homes can attract slightly higher premiums, though quality construction and maintenance can offset this.

Timber/Laminate Flooring Timber floors are a valued feature but can be more susceptible to water damage than tiles. This may contribute modestly to the contents and building premium.

Swimming Pool Pools add to the replacement cost of the property and can introduce liability considerations, both of which are reflected in the sum insured and premium.

Solar Panels Solar panels are typically covered under building insurance, but they add to the replacement value of the home. At 214 sqm, this is a mid-to-large sized dwelling, and with solar included in the building sum insured of $691,000, the coverage appears appropriately sized.

Granny Flat The presence of a granny flat on the property is a significant factor. Additional dwellings increase the total insurable value and can introduce questions around occupancy, liability, and contents coverage. It's important to confirm with your insurer that the granny flat is explicitly covered under your policy.

---

Tips for Homeowners in Montville

1. Review your granny flat coverage carefully Not all standard home insurance policies automatically cover a secondary dwelling. Check your Product Disclosure Statement (PDS) to confirm whether the granny flat is included — and if not, ask about adding it as an endorsement or taking out a separate policy.

2. Get your building sum insured right At $691,000 for a 214 sqm home with a pool and granny flat, the sum insured looks reasonable — but it's worth using a building replacement cost calculator periodically, especially given rising construction costs in regional Queensland. Being underinsured can leave you significantly out of pocket after a major claim.

3. Shop the market at renewal time With a suburb 25th percentile of $3,101/yr, there's clearly a range of pricing available in Montville. Loyalty doesn't always pay — insurers often reserve their best rates for new customers. Comparing quotes annually is one of the simplest ways to keep your premium in check.

4. Ask about discounts for security and maintenance Some insurers offer discounts for properties with monitored alarm systems, deadbolts, or smoke detectors. Given the age of this home, ensuring electrical and plumbing systems are up to date may also reduce the risk of claim-related disputes.

---

Ready to Compare?

Whether you're a long-time Montville local or new to the area, it pays to know what the market looks like before you renew. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can see exactly where your premium sits relative to your neighbours.

Get a quote today at CoverClub and find out if you're paying the right price for your piece of the hinterland.