Moonee Ponds is one of Melbourne's most sought-after inner-north suburbs — a leafy, character-rich area known for its period homes, vibrant shopping strips, and strong community feel. But owning a classic free standing home here comes with its own set of insurance considerations, particularly when the property has heritage construction features that can significantly influence what you pay. This article breaks down a real home and contents insurance quote for a 4-bedroom, 2-bathroom free standing home in Moonee Ponds (VIC 3039), and helps you understand whether the price stacks up.

---

Is This Quote Fair?

The annual premium for this property came in at $3,903 per year (or $349/month), covering both building and contents. Our price rating for this quote is Expensive — Above Average.

To put that in context: the suburb average for Moonee Ponds sits at $2,434/year, with a median of just $1,869/year. This quote lands well above both of those benchmarks, and even sits above the suburb's 75th percentile of $3,499/year — meaning it's pricier than at least three-quarters of comparable quotes in the area.

That said, "expensive" doesn't necessarily mean "wrong." The sum insured on the building is $2,371,000, which is substantial and reflects the true rebuild cost of a larger, older home with premium construction materials. The contents are insured for $338,000, which is also on the higher side. These figures directly drive the premium — and if they're accurate, they may well justify the price. The key question is always whether the coverage is right-sized for the property.

Both the building and contents excess are set at $5,000, which is relatively high. Choosing a higher excess is a common way to reduce your annual premium, but it also means a larger out-of-pocket cost if you need to make a claim. It's worth weighing whether that trade-off suits your financial situation.

---

How Moonee Ponds Compares

Understanding where this quote sits relative to broader benchmarks gives a clearer picture of value.

| Benchmark | Premium |

|---|---|

| This Quote | $3,903/yr |

| Moonee Ponds Suburb Average | $2,434/yr |

| Moonee Ponds Suburb Median | $1,869/yr |

| Moonee Valley LGA Average | $1,817/yr |

| VIC State Average | $3,000/yr |

| VIC State Median | $2,718/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

Compared to the Victorian state average of $3,000/year, this quote is about 30% higher. However, when stacked against the national average of $5,347/year, it's actually well below — a reminder that home insurance costs vary enormously depending on location, risk profile, and the specific insurer.

The Moonee Valley LGA average of $1,817/year is notably lower than the suburb average, which suggests that properties within Moonee Ponds itself may carry slightly higher risk characteristics or higher insured values than surrounding areas in the council zone.

With only 31 quotes in the suburb sample, it's also worth noting that local data has some natural variability — a wider range of property types and insured values can skew averages in either direction.

---

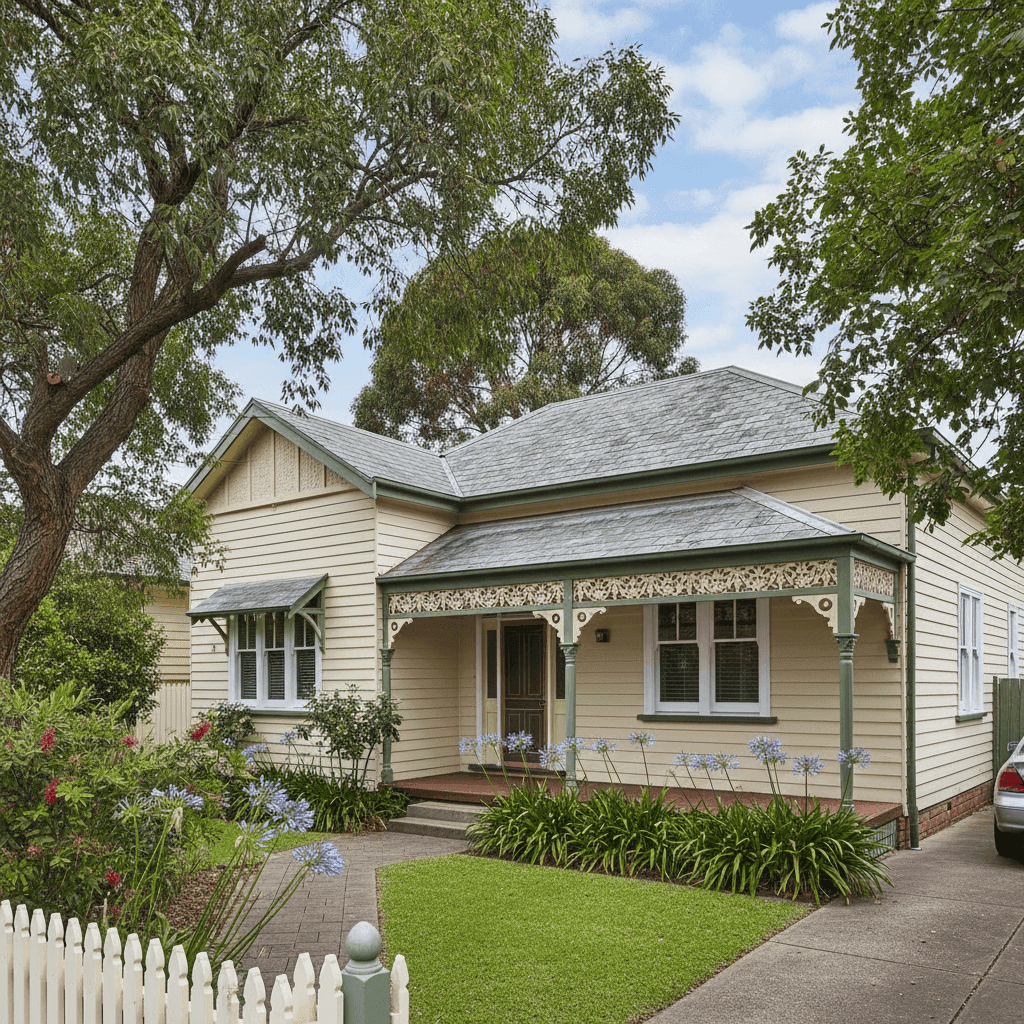

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to the above-average premium:

Weatherboard timber construction is one of the most significant factors. Older weatherboard homes are considered higher risk by insurers due to their susceptibility to fire and the higher cost of like-for-like repairs. Sourcing matching timber weatherboards for a 1937-era home can be expensive, and tradespeople with the skills to work on heritage properties often charge a premium.

Slate roof is another cost driver. Slate is a beautiful, durable material — but it's also one of the most expensive roofing materials to repair or replace. Insurers factor in the full cost of reinstatement, and a slate roof on a home of this size adds meaningfully to the rebuild estimate.

Construction year (1937) matters too. Pre-war homes often have older electrical wiring, plumbing, and structural elements that may not meet current building codes. In the event of a major claim, bringing the property up to modern standards can significantly increase rebuild costs — and responsible insurers price for this.

Slab foundation with timber/laminate flooring is a fairly standard combination, but timber flooring in older homes can be prone to moisture-related issues, particularly if the slab has any drainage concerns.

Ducted climate control adds to the contents and building value — these systems are expensive to install and replace, and their inclusion in the insured value is appropriate.

Building size of 214 sqm is above average for an inner-Melbourne home, and combined with the high-quality period construction, contributes to the elevated sum insured of $2,371,000.

---

Tips for Homeowners in Moonee Ponds

1. Get your sum insured independently verified. With a building sum insured of $2,371,000, it's worth having a qualified quantity surveyor or building estimator confirm that figure. Being over-insured costs you more in premiums; being under-insured can leave you seriously exposed after a major loss. Many insurers offer free online calculators, but a professional assessment is more reliable for heritage properties.

2. Review your excess level carefully. A $5,000 excess on both building and contents is quite high. If you haven't made a claim in years and have strong cash reserves, this might be a deliberate and sensible choice. But if you'd struggle to cover that cost unexpectedly, consider whether a lower excess — even if it increases the annual premium slightly — gives you better peace of mind.

3. Ask about heritage or period home specialists. Some insurers specialise in older or heritage properties and may offer more competitive pricing or better coverage terms for weatherboard and slate-roofed homes. Mainstream policies don't always account for the nuances of period construction, so it's worth exploring specialist options.

4. Compare quotes annually. Insurance markets shift, and loyalty doesn't always pay. Given this quote is above the suburb average, shopping around at renewal time — using a comparison service like CoverClub — could uncover meaningful savings without sacrificing coverage quality.

---

Ready to Compare Home Insurance in Moonee Ponds?

Whether you're renewing an existing policy or insuring a property for the first time, comparing quotes is the single most effective way to make sure you're getting fair value. CoverClub makes it easy to see how your premium stacks up against real data from your suburb, your state, and across Australia.

Get a home insurance quote today and find out if you could be paying less — without compromising on the cover your home deserves.