If you own a free standing home in Moore Park Beach, QLD 4670, you've probably wondered whether your home insurance premium is reasonable — or whether you're paying more than you should be. This article breaks down a real home and contents insurance quote for a four-bedroom property in the suburb, comparing it against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,165 per year (or $296 per month) for a combined home and contents policy, covering a building sum insured of $649,000 and contents valued at $50,000. Both the building and contents excesses are set at $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Moore Park Beach sits at $3,141 per year, meaning this quote is only $24 above what most comparable properties in the area are paying. That's a negligible difference — less than 1% above the local average.

It's worth noting the distinction between the average and the median, though. The suburb median premium is $2,785 per year, which is noticeably lower than this quote. The median is often a better indicator of what a "typical" homeowner pays, as it's less influenced by outliers at the high end. That said, this quote still falls comfortably within the middle of the market — the 25th percentile sits at $2,150/yr and the 75th percentile at $3,564/yr — meaning this premium lands solidly in the second half of the range without pushing into expensive territory.

In short: you're not getting a bargain, but you're not being overcharged either. There's room to potentially do better, but this quote is a defensible price for the property and cover level.

---

How Moore Park Beach Compares

To put this quote in broader context, it helps to look at how Moore Park Beach premiums stack up against the rest of Queensland and the country.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Moore Park Beach (suburb) | $3,141/yr | $2,785/yr |

| Queensland (state) | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

The contrast with Queensland's state-wide figures is striking. The QLD average premium of $9,129 per year is nearly three times the suburb average — a reflection of the enormous variability in insurance costs across the state. Queensland is home to some of Australia's most exposed coastal and cyclone-prone regions, which push the state average dramatically upward. Moore Park Beach, by comparison, is not classified as a cyclone risk area, which helps keep premiums far more manageable.

Compared to national figures, the picture is similarly favourable. The national average of $5,347/yr is well above what Moore Park Beach homeowners are typically paying, though the national median of $2,764/yr is actually slightly below the suburb median — suggesting that while many Australians pay less, Moore Park Beach is broadly in line with the middle of the national market.

The takeaway: Moore Park Beach is a relatively affordable suburb to insure compared to much of Queensland, and this quote reflects that positioning accurately.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence its insurance cost, both positively and negatively.

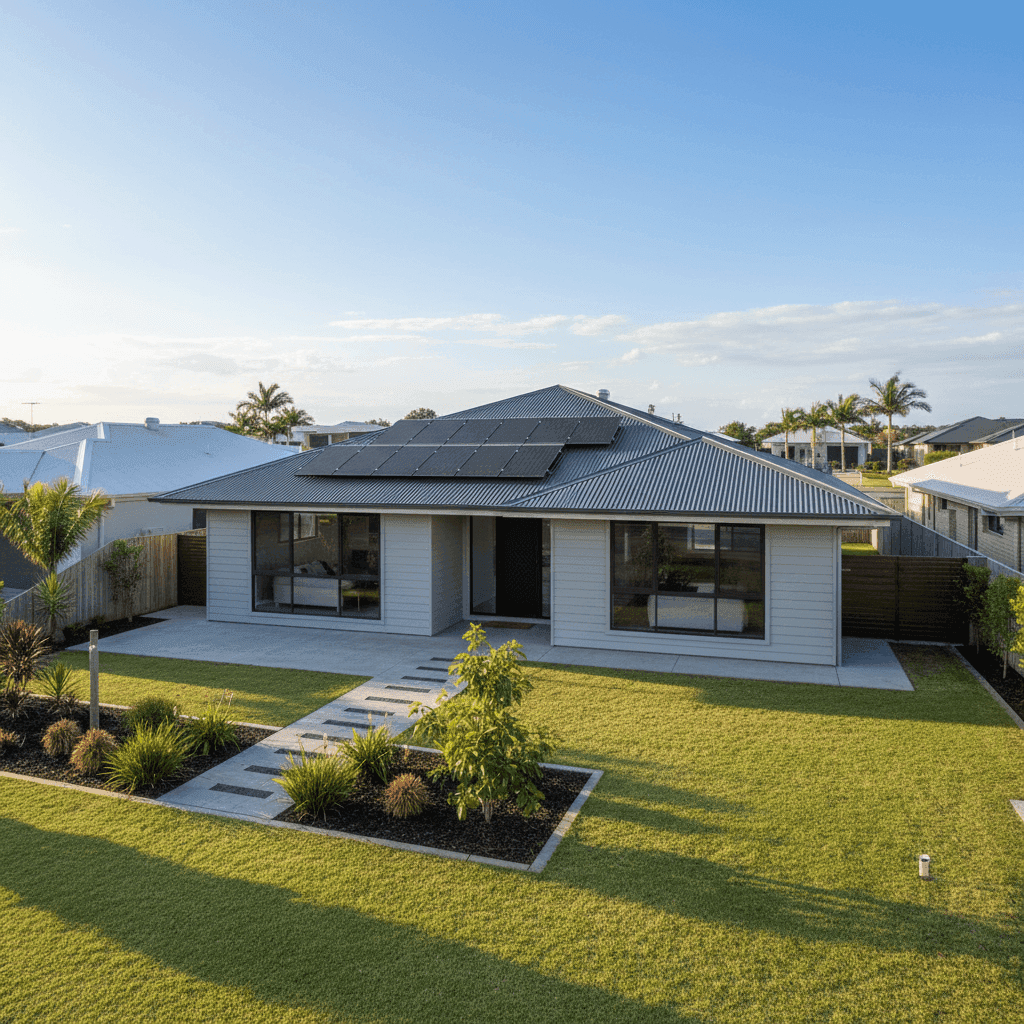

Construction quality and materials play a significant role. The home features Hardiplank/Hardiflex external walls and a steel/Colorbond roof — both considered durable, low-maintenance materials that insurers generally view favourably. Colorbond roofing in particular is resistant to fire, corrosion, and high winds, which can help moderate premiums compared to older or less resilient materials.

The slab foundation is another positive factor. Slab-on-ground construction is common in Queensland and is generally well-regarded by insurers for its stability and resistance to underfloor moisture issues.

Timber and laminate flooring is worth flagging as a consideration. These materials can be more susceptible to water damage than tiles, which may factor into how an insurer prices contents and internal damage cover.

The home's above-average fittings quality — think quality kitchen appliances, premium fixtures, and better-than-standard finishes — increases the cost to rebuild or repair, which is reflected in the $649,000 building sum insured. Underinsuring a home with high-quality fittings is a common and costly mistake, so it's good to see an appropriate sum insured here.

Solar panels add value to the property but also represent an additional asset that needs to be covered. Many policies include solar panels as part of the building cover, but it's always worth confirming this with your insurer explicitly.

Finally, the ducted climate control system is another fixed installation that contributes to the replacement cost of the home. Like solar panels, this is typically covered under building insurance, but verifying the specifics of your policy is always wise.

---

Tips for Homeowners in Moore Park Beach

1. Review your sum insured annually Building costs have risen significantly in recent years due to labour shortages and material price increases. A sum insured that was accurate two years ago may no longer reflect what it would actually cost to rebuild your home today. Use a building cost estimator or speak with a quantity surveyor to make sure you're not underinsured.

2. Confirm solar panel and ducted system coverage As mentioned above, solar panels and ducted air conditioning are significant assets. Check your policy documents to confirm these are explicitly covered — including for accidental damage and storm events — and that the covered value is sufficient.

3. Shop around at renewal time Even if your current quote is rated as fair, the insurance market changes constantly. Premiums can shift significantly between insurers for the same property. Use a comparison tool like CoverClub to benchmark your renewal quote before accepting it automatically.

4. Consider your excess carefully This policy carries a $1,000 excess on both building and contents. Opting for a higher excess can reduce your annual premium — but make sure you'd genuinely be comfortable covering that amount out of pocket in the event of a claim. For most homeowners, $1,000 is manageable, but it's a personal decision worth thinking through.

---

Compare Your Quote with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, it pays to have the right data on your side. CoverClub aggregates real premium data from across Australia so you can see exactly where your quote sits in the market — not just whether it sounds reasonable, but whether it actually is.

Get a home insurance quote today and see how your premium compares to your neighbours in Moore Park Beach and beyond.