Mooroobool is a well-established residential suburb in Cairns, Far North Queensland — and like much of the region, it comes with its own unique set of insurance considerations. This analysis looks at a building-only insurance quote for a large, modern free standing home in the area, breaking down whether the premium is competitive and what factors are likely driving the cost.

---

Is This Quote Fair?

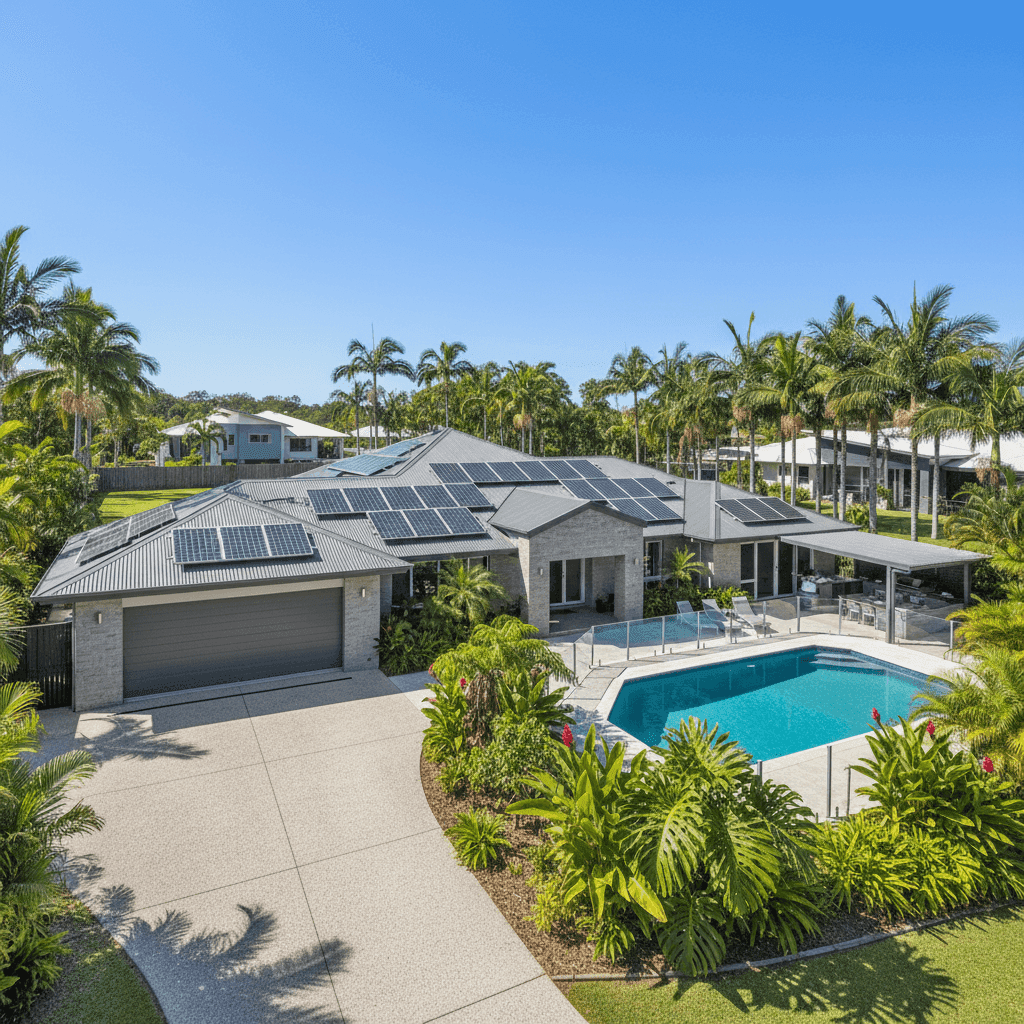

The quote in question sits at $7,714 per year (or $739/month) for building-only cover on a 6-bedroom, 3-bathroom free standing home, with a building sum insured of $2,501,000 and a standard $1,000 excess.

Based on CoverClub's pricing data, this quote is rated Expensive — Above Average for the Mooroobool area. The suburb's average annual premium sits at $4,972, and the median is $4,637, meaning this quote is running approximately 55% above the suburb average and 66% above the suburb median. It also falls well above the 75th percentile for the area ($5,573), placing it among the priciest quotes in the local sample.

That said, context matters enormously here. This is a large, high-value property — 389 sqm of living space with a sum insured of $2.5 million is significantly above what most homes in the suburb would be insured for. The premium reflects not just the location risk, but also the sheer scale and replacement value of the dwelling. It's also worth noting that the Cairns LGA average premium is a striking $12,404 per year, which puts this quote in a more favourable light when viewed through a regional lens.

---

How Mooroobool Compares

To properly contextualise this quote, it helps to look at the broader pricing landscape:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $7,714 |

| Mooroobool Suburb Average | $4,972 |

| Mooroobool Suburb Median | $4,637 |

| Mooroobool 75th Percentile | $5,573 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

| Cairns LGA Average | $12,404 |

(Based on a sample of 40 quotes in the Mooroobool area. [View full suburb stats](https://coverclub.com.au/stats/QLD/4870/mooroobool).)

A few things stand out from this comparison. First, Queensland's state average ($9,129) is considerably higher than the national average ($5,347) — a reflection of the elevated natural hazard risk across much of the state, particularly in cyclone-prone regions like Cairns. In fact, the gap between QLD's average and the national average is nearly $3,800 per year, underscoring just how much geography influences what Queenslanders pay for home insurance.

Second, the Cairns LGA average of $12,404 is remarkably high — nearly 2.5 times the national average. This quote, while above the suburb median, is actually well below the broader LGA average, which suggests the property's construction quality and age may be helping to keep costs in check relative to older or more vulnerable homes in the region.

You can explore more QLD home insurance data here.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted:

Cyclone Risk Zone Mooroobool falls within a designated cyclone risk area — this is arguably the single biggest driver of elevated premiums in the Cairns region. Insurers price cyclone exposure heavily, and it affects virtually every policy written in Far North Queensland.

Large Home with High Sum Insured At 389 sqm and a sum insured of $2,501,000, this is a substantial property. Rebuilding costs scale with size and quality, and above-average fittings mean the per-square-metre replacement cost is higher than a standard build. The sum insured directly influences the base premium calculation.

Concrete Walls and Colorbond Roof Concrete external walls are generally viewed favourably by insurers — they offer excellent resistance to wind, fire, and impact damage. Combined with a steel/Colorbond roof (which performs well in high-wind events), this construction profile can help moderate the premium compared to timber-framed or older homes.

Slab Foundation and Tile Flooring A concrete slab foundation is a low-risk construction type for insurers — there's no subfloor space to flood or decay. Tile flooring is similarly durable and resistant to water damage, which is a positive in a high-humidity, high-rainfall climate like Cairns.

Pool, Solar Panels, and Ducted Climate Control These features add to the overall replacement value of the property and are typically factored into the sum insured. Solar panels in particular can be costly to replace and may carry specific coverage considerations depending on the policy. Ducted climate control systems are also expensive to reinstate after storm or water damage.

Modern Construction (Built 2015) A 2015 build means the property was constructed to relatively recent building codes, which in Queensland include strict cyclone-resilience standards. Newer homes generally attract lower premiums than older stock in cyclone-prone areas.

---

Tips for Homeowners in Mooroobool

1. Review your sum insured regularly With construction costs rising across Australia, the gap between what your policy covers and what it would actually cost to rebuild can grow quickly. For a home of this size and quality, it's worth getting a professional building valuation every few years to ensure your sum insured remains accurate — over-insuring adds unnecessary cost, while under-insuring can leave you exposed.

2. Shop around — especially in a high-risk zone Insurers price cyclone risk very differently. The spread of premiums in Mooroobool (from $3,466 at the 25th percentile to $5,573 at the 75th) shows there's meaningful variation in the market. Comparing quotes through CoverClub is one of the easiest ways to see what different insurers are offering for your specific property.

3. Check what's included for storm and cyclone damage Not all policies treat cyclone damage the same way. Some include a separate cyclone excess, while others may have exclusions or sub-limits for certain types of wind or water ingress. Read the Product Disclosure Statement (PDS) carefully and ask your insurer directly if you're unsure.

4. Consider the value of your solar and pool assets Make sure your policy explicitly covers your solar panel system and pool infrastructure. Some standard building policies include these automatically, while others treat them as optional extras or exclude certain components. Given the replacement cost of a full solar system and pool equipment, it's worth confirming the details before you need to make a claim.

---

Ready to Compare?

Whether you're looking to benchmark your current policy or find a better deal, CoverClub makes it easy to compare home insurance quotes tailored to your property. With real pricing data from across Mooroobool and the broader Cairns region, you can see exactly where your quote sits in the market — and whether there's room to save.