If you own a free standing home in Morayfield, QLD 4506, you've probably noticed that home insurance premiums can vary enormously — even between neighbouring streets. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom brick veneer property in Morayfield, comparing it against suburb, state, and national benchmarks so you can make a truly informed decision.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,385 per year (or $233 per month), covering both building (sum insured: $674,000) and contents ($50,000), each with a $1,000 excess. Our independent price rating for this quote is FAIR — Around Average.

That rating holds up when you dig into the numbers. The suburb average for Morayfield sits at $2,390 per year, meaning this quote is almost exactly in line with what most comparable properties in the area are paying. It also sits comfortably above the 25th percentile ($1,495/yr) and well below the 75th percentile ($3,063/yr), placing it squarely in the middle of the market for this postcode.

In short: this isn't a bargain, but it's not an overpriced policy either. For a property of this size, age, and specification, paying close to the suburb average is a reasonable outcome — though there's always room to do better with a bit of comparison shopping.

---

How Morayfield Compares

To put this quote in proper context, it helps to zoom out and look at the broader picture. You can explore the full Morayfield suburb insurance stats, Queensland state-wide data, and national insurance benchmarks on CoverClub.

Here's how the numbers stack up:

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,385 |

| Morayfield suburb average | $2,390 |

| Morayfield suburb median | $2,231 |

| Moreton Bay LGA average | $3,435 |

| QLD state average | $9,129 |

| QLD state median | $3,903 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. First, Morayfield is a genuinely affordable suburb when it comes to home insurance — the local average of $2,390 is dramatically lower than the Queensland state average of $9,129. That gulf is largely explained by the state's exposure to extreme weather events, particularly cyclones and flooding in Far North Queensland, which push the state average sky-high. Morayfield, sitting in South East Queensland, benefits from a significantly lower natural hazard risk profile.

Compared to the national median of $2,764, this quote is actually slightly below par — another positive sign. The Moreton Bay LGA average of $3,435 is notably higher than the suburb figure, which suggests that some neighbouring areas within the same local government area carry higher risk ratings, making Morayfield a relatively cost-effective pocket of the region.

---

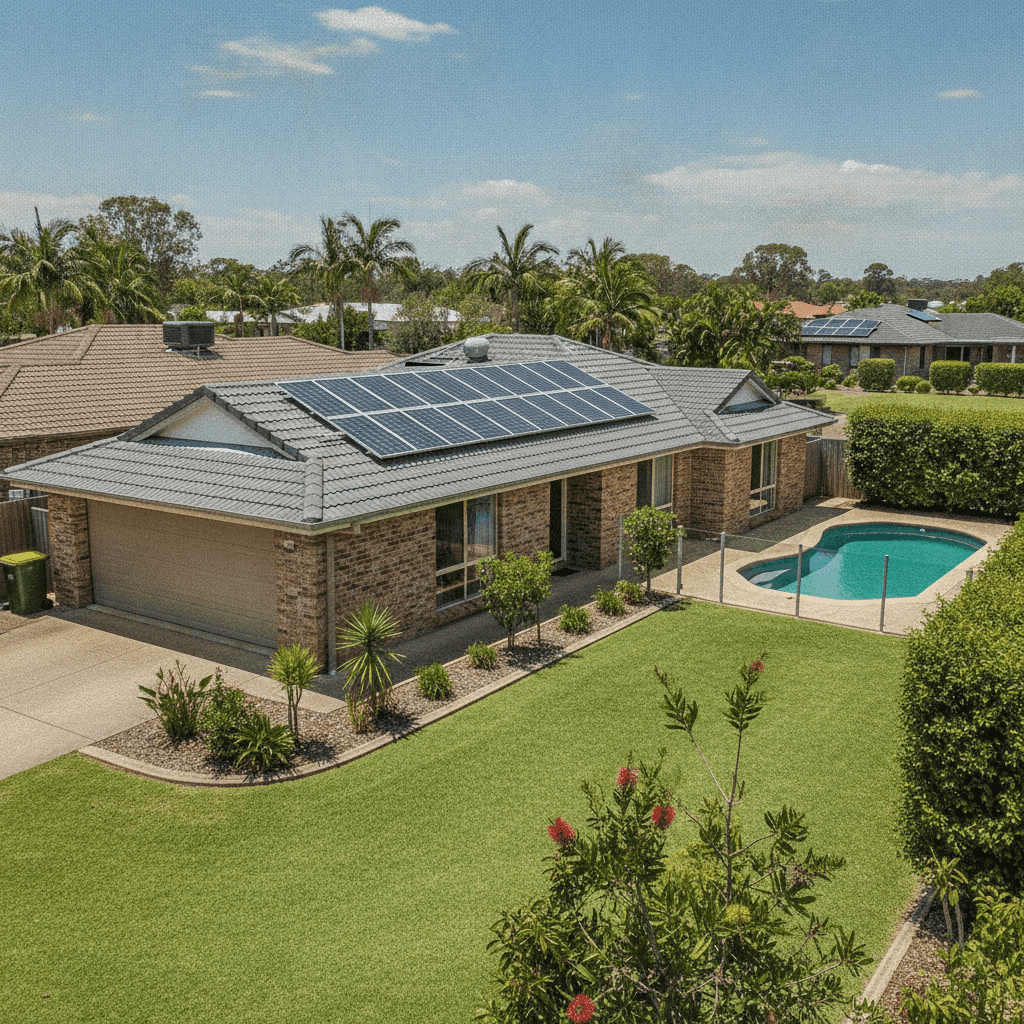

Property Features That Affect Your Premium

Every home is different, and insurers price policies based on a detailed assessment of the property's characteristics. Here's how the features of this particular home influence its premium:

Brick Veneer Walls & Tiled Roof Brick veneer construction is generally viewed favourably by insurers. It's durable, fire-resistant, and holds up well in storms — all factors that reduce the likelihood of a major claim. Similarly, a tiled roof is considered a solid, long-lasting material. Together, these construction materials typically attract more competitive premiums compared to, say, weatherboard or Colorbond alternatives.

Slab Foundation A concrete slab foundation is the standard for homes of this era and is generally considered low-risk from an insurance perspective. It offers good structural stability and is less susceptible to subsidence or pest damage than older pier-and-beam foundations.

Built in 1992 At over 30 years old, this home is entering the age range where some insurers begin to factor in the cost of updating older plumbing, electrical systems, or roofing. It's worth ensuring your sum insured ($674,000) accurately reflects current rebuild costs, including labour and materials inflation — something that has risen sharply in recent years across Queensland.

Pool, Solar Panels & Ducted Climate Control These three features add both value and complexity to a policy. A swimming pool increases liability exposure and adds to the overall replacement cost of the property. Solar panels — particularly a rooftop system — need to be explicitly covered for storm, hail, and fire damage. Ducted climate control systems are a significant fixed asset and can be expensive to repair or replace. All three features are good reasons to review your sum insured carefully and confirm they're included in your building cover.

Tile Flooring Tiled flooring throughout is a practical choice in Queensland's climate and is generally straightforward to insure. It's durable and less susceptible to water damage than carpet or timber, which can slightly reduce contents-related claims risk.

---

Tips for Homeowners in Morayfield

1. Review your sum insured annually With $674,000 in building cover, this policy is in a reasonable range for a 214 sqm brick veneer home — but construction costs in South East Queensland have risen significantly. Use a building cost calculator or speak with a quantity surveyor to make sure you're not underinsured, particularly given the pool, solar system, and ducted air conditioning.

2. Confirm your solar panels and pool are explicitly covered Not all standard home insurance policies automatically cover solar panel systems or swimming pool infrastructure as part of the building sum insured. Check your Product Disclosure Statement (PDS) carefully and ask your insurer to confirm these are included — and at what value.

3. Consider increasing your excess to reduce your premium Both the building and contents excess on this policy sit at $1,000. If you have a healthy emergency fund, opting for a higher excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. Just make sure the saving is worth the additional out-of-pocket cost if you do need to claim.

4. Compare quotes at renewal — every year Even though this quote is rated Fair, the insurance market shifts constantly. Insurers reprice their books regularly, and loyalty doesn't always pay. Running a fresh comparison at renewal time takes only a few minutes and could save you hundreds of dollars without changing your level of cover.

---

Ready to Find a Better Rate?

Whether you're happy with your current insurer or looking to switch, it pays to see what else is on the market. Get a home insurance quote through CoverClub and compare your options in minutes — no obligation, no hassle. With data from dozens of properties across Morayfield and the broader Moreton Bay region, CoverClub helps you understand whether you're getting a genuinely competitive deal.