Morayfield, nestled in Queensland's Moreton Bay region, is a well-established suburb popular with families drawn to its affordable housing, good schools, and easy access to the Bruce Highway. If you own a free-standing home here, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your household budget. This article breaks down a recent quote for a four-bedroom brick veneer home in Morayfield and puts the numbers in context.

---

Is This Quote Fair?

The quote in question comes in at $2,447 per year (or $235 per month) for combined home and contents cover, with a building sum insured of $715,000 and contents valued at $150,000. Both the building and contents excess are set at $2,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb average premium for Morayfield sits at $2,390 per year, meaning this quote is only about $57 above the local average — a difference of roughly 2.4%. That's well within normal variation and not a cause for concern.

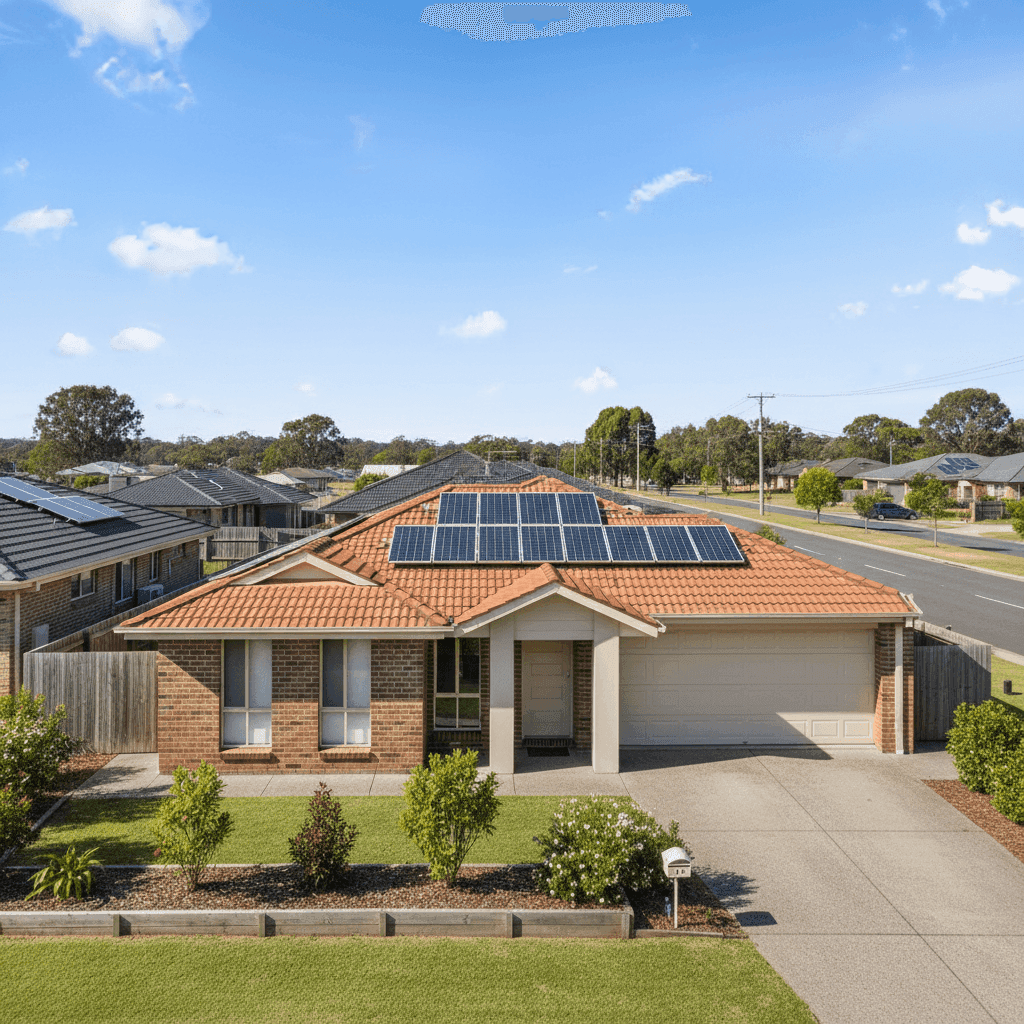

What does this mean in practice? You're not getting a bargain-basement deal, but you're also not being overcharged. For a property of this size and specification — 214 sqm, tiled roof, brick veneer walls, slab foundation, ducted climate control, and solar panels — a premium in this range is a reasonable reflection of the risk profile and replacement cost involved.

---

How Morayfield Compares

To put this quote in proper perspective, it helps to zoom out and look at the broader pricing landscape. You can explore the full breakdown on the Morayfield suburb stats page.

| Benchmark | Premium |

|---|---|

| This quote | $2,447/yr |

| Morayfield suburb average | $2,390/yr |

| Morayfield suburb median | $2,231/yr |

| Morayfield 25th percentile | $1,495/yr |

| Morayfield 75th percentile | $3,063/yr |

| Moreton Bay LGA average | $3,435/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

A few things stand out here. First, this quote sits comfortably below the Moreton Bay LGA average of $3,435 — suggesting that Morayfield, as a suburb within the region, benefits from relatively lower risk pricing compared to some of its neighbours.

Second, the Queensland state average of $9,129 per year is strikingly high. This is largely driven by premium-heavy coastal and far-north Queensland postcodes — think Cairns, Townsville, and the Whitsundays — where cyclone risk dramatically inflates insurance costs. Morayfield is not classified as a cyclone risk area, which is a significant advantage. You can see how Queensland compares overall on the QLD state stats page.

At the national level, the average premium of $5,347 and median of $2,764 also reflect the outsized influence of high-risk regions. This quote comes in below the national median, which is a positive sign for Morayfield homeowners. Browse national home insurance stats to see how your state stacks up against the rest of Australia.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Understanding these can help you anticipate costs and make informed decisions.

Brick veneer construction is generally viewed favourably by insurers. It offers solid structural integrity and good fire resistance, which typically translates to more competitive premiums compared to weatherboard or timber-framed homes.

Tiled roof is another positive factor. Concrete or terracotta tiles are durable and perform well in hail and moderate weather events. They're considered lower risk than corrugated iron or older materials, and most insurers price them accordingly.

Slab foundation is standard for Queensland homes built in the 2000s and is generally straightforward to insure. There's no elevated subfloor space to worry about, which simplifies the risk assessment.

Solar panels are worth noting. While they add value to the property and reduce energy costs, they do represent an additional asset that needs to be covered. Some insurers include solar panels under the building sum insured automatically; others treat them as an optional extra. It's worth confirming this is adequately covered under your policy.

Ducted climate control adds to the replacement value of the home. This kind of fixed installation is typically covered under building insurance, but it's one of those features that can be easy to underestimate when calculating your sum insured.

Building sum insured of $715,000 for a 214 sqm home works out to roughly $3,340 per square metre — a figure that aligns with current construction costs in South East Queensland, particularly given the quality of fittings and inclusions described. Ensuring your sum insured accurately reflects rebuild costs (not market value) is critical to avoiding underinsurance.

---

Tips for Homeowners in Morayfield

1. Review your sum insured annually Construction costs in Queensland have risen sharply over the past few years due to labour shortages and material price increases. What was an adequate sum insured two years ago may no longer cover a full rebuild today. Use a building cost calculator or speak with a quantity surveyor to validate your figure each year.

2. Confirm solar panel coverage With solar panels on the roof, check your policy wording carefully. Are the panels, inverter, and associated wiring all included under the building definition? If not, you may need to list them separately or adjust your sum insured to account for their replacement value.

3. Consider your excess level carefully Both the building and contents excess on this policy are set at $2,000. While a higher excess generally lowers your premium, you need to be comfortable covering that amount out of pocket in the event of a claim. If $2,000 feels steep, it's worth modelling what a lower excess would cost in additional premium — the difference is sometimes smaller than you'd expect.

4. Shop around at renewal time A "Fair" rating means this quote is competitive, but it's not necessarily the best available. Insurers reprice their books regularly, and loyalty doesn't always pay. Getting two or three comparable quotes at renewal takes minimal effort and can yield meaningful savings without sacrificing cover quality.

---

Compare Home Insurance Quotes in Morayfield

Whether you're renewing an existing policy or insuring a new home, it pays to see what's available across multiple insurers. CoverClub makes it easy to compare home and contents quotes tailored to your property and postcode. Get a quote today and find out if you could be paying less — or getting more cover — for your Morayfield home.