If you own a free standing home in Moree, NSW 2400, you've probably wondered whether you're paying a fair price for home insurance — or whether there's a better deal out there. In this article, we break down a real home and contents insurance quote for a four-bedroom property in Moree, compare it against local, state, and national benchmarks, and share some practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

The quote in question comes in at $3,641 per year (or $342/month) for a combined home and contents policy. The building is insured for $650,000, with $50,000 in contents cover. Both the building and contents excess are set at $5,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. When compared against the suburb-level statistics for Moree (NSW 2400), this premium sits comfortably between the 25th percentile ($2,538/yr) and the 75th percentile ($5,113/yr), and comes in just below the suburb median of $3,822/yr. That means this homeowner is paying slightly less than the typical Moree policyholder — which is a reasonable outcome.

It's worth noting that the suburb average premium is a striking $43,287/yr, but this figure is heavily skewed by outlier quotes in the dataset (only 18 quotes were sampled). The median is a far more reliable indicator of what most Moree residents are actually paying, and at $3,822/yr, it puts this quote in a solid position.

---

How Moree Compares

Understanding where Moree sits relative to broader benchmarks is useful context for any homeowner reviewing their policy.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Moree (NSW 2400) | $43,287/yr* | $3,822/yr |

| New South Wales | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

\Suburb average is skewed by a small sample size of 18 quotes.*

Compared to the NSW state median of $3,770/yr, this quote is almost identical — just $129 more per year. Against the national median of $2,764/yr, it's notably higher, though this is expected given the property's size, age, and regional location.

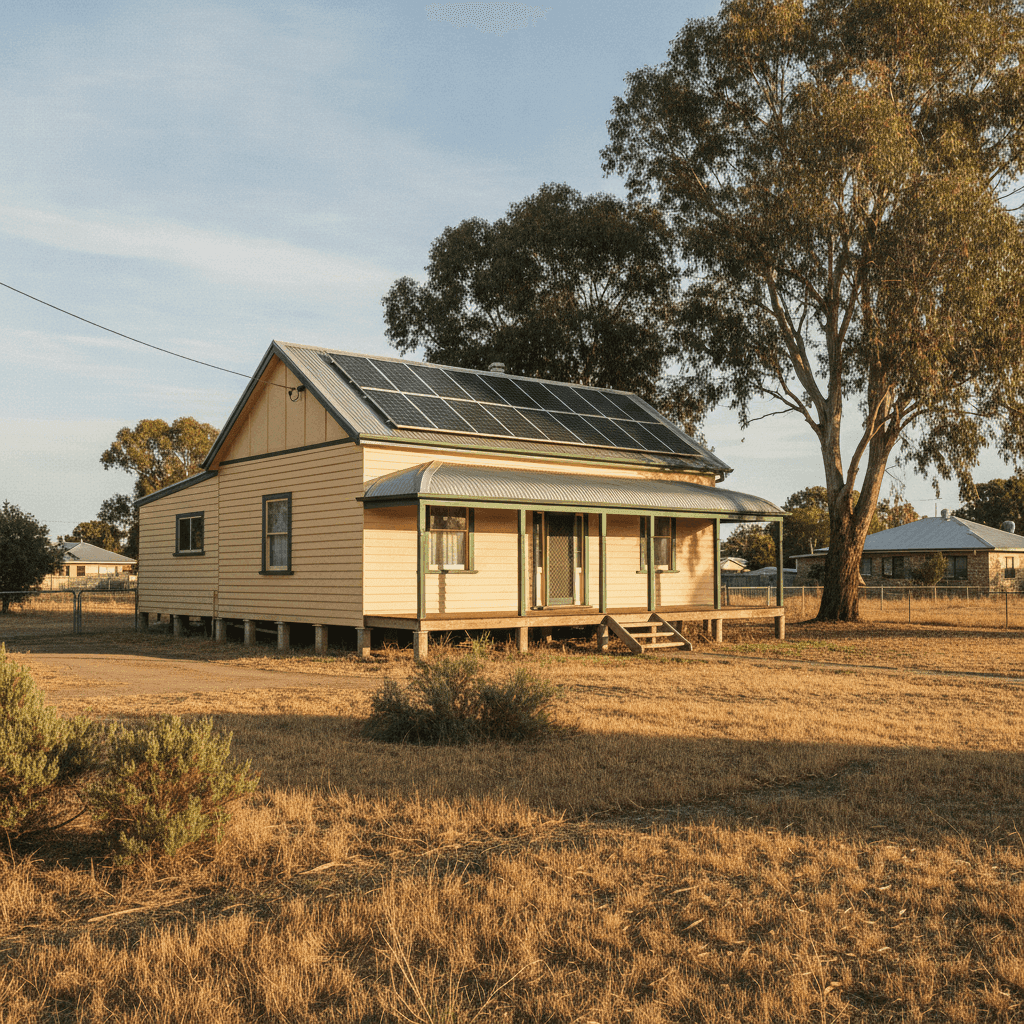

Regional NSW properties — particularly those in agricultural towns like Moree — often attract slightly higher premiums than the national median due to factors like distance from emergency services, local weather patterns (including flooding risk along the Mehi River), and the age of the housing stock. All things considered, $3,641/yr for a 205 sqm, four-bedroom home with solar panels and ducted climate control is a reasonable outcome.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted. Here's how each one plays into the pricing:

Weatherboard Timber Walls

Weatherboard construction is one of the most common wall types in older Australian homes, but it does carry a higher fire risk compared to brick or rendered masonry. Insurers typically price this in, particularly in regional areas where fire response times may be longer.

Steel / Colorbond Roof

Colorbond roofing is generally viewed favourably by insurers. It's durable, resistant to corrosion, and performs well in high-wind events. This is a positive factor for the premium compared to, say, terracotta tiles, which are heavier and more prone to storm damage.

Stump Foundation

Homes built on stumps (common in regional NSW, especially for pre-1980s construction) can be more susceptible to movement and moisture-related damage. This can influence premiums slightly upward, though it also allows for easier underfloor inspections and maintenance.

Construction Year: 1975

At roughly 50 years old, this home predates many modern building codes. Older homes can present higher replacement costs and a greater likelihood of outdated electrical wiring or plumbing — factors that insurers account for when calculating risk.

Solar Panels

The presence of rooftop solar panels adds to the replacement value of the home. Policies that include solar cover ensure panels are protected against storm, hail, and fire damage — a smart inclusion for any home with this technology.

Ducted Climate Control

Ducted air conditioning systems are expensive to repair or replace. Their inclusion in the sum insured helps ensure the building cover is adequate and reduces the risk of being underinsured.

Sum Insured: $650,000

For a 205 sqm home in regional NSW, a $650,000 building sum insured is substantial. It's important that this figure reflects the rebuild cost (not the market value), including demolition, materials, and labour. Given the age and construction type, getting a professional building valuation periodically is worthwhile.

---

Tips for Homeowners in Moree

Whether you're reviewing an existing policy or shopping for a new one, here are four practical steps Moree homeowners can take to manage their insurance costs and coverage:

- Review your sum insured annually. Construction costs have risen significantly in recent years. If your building sum insured hasn't been updated recently, you may be underinsured — or overpaying for cover that doesn't reflect current rebuild costs. Use a building cost calculator or consult a quantity surveyor.

- Consider your excess carefully. This quote carries a $5,000 excess on both building and contents. While a higher excess generally reduces your premium, make sure it's an amount you can genuinely afford to pay out of pocket in the event of a claim. If cash flow is a concern, a lower excess may be worth the slightly higher annual cost.

- Protect your weatherboard exterior. Regular maintenance — painting, replacing rotting boards, and sealing gaps — not only extends the life of your home but can also demonstrate to insurers that the property is well maintained. Some insurers factor in property condition when assessing risk.

- Shop around at renewal time. Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for the same level of cover. Use a comparison tool like CoverClub to benchmark your renewal quote against the market before you commit.

---

Get a Better Deal on Home Insurance

Whether this quote is your current policy or one you're considering, it's always worth comparing your options. CoverClub makes it easy to see how your premium stacks up against other homeowners in Moree and across NSW — and to find a policy that gives you the right cover at a competitive price.