If you own a free standing home in Moree, NSW 2400, you've probably wondered whether your home insurance premium is reasonable — or whether you're paying more than you should. Moree is a regional hub in the Gwydir region of northern New South Wales, known for its artesian hot springs, agricultural surrounds, and a housing stock that skews toward older, character-filled homes. In this analysis, we break down a real building insurance quote for a 3-bedroom, 2-bathroom property in Moree to help you understand what's driving the price and how it stacks up against the broader market.

---

Is This Quote Fair?

The quote in question comes in at $4,276 per year (or $403 per month) for building-only cover, with a $1,000 building excess and a sum insured of $589,000. Our price rating for this quote is FAIR — Around Average.

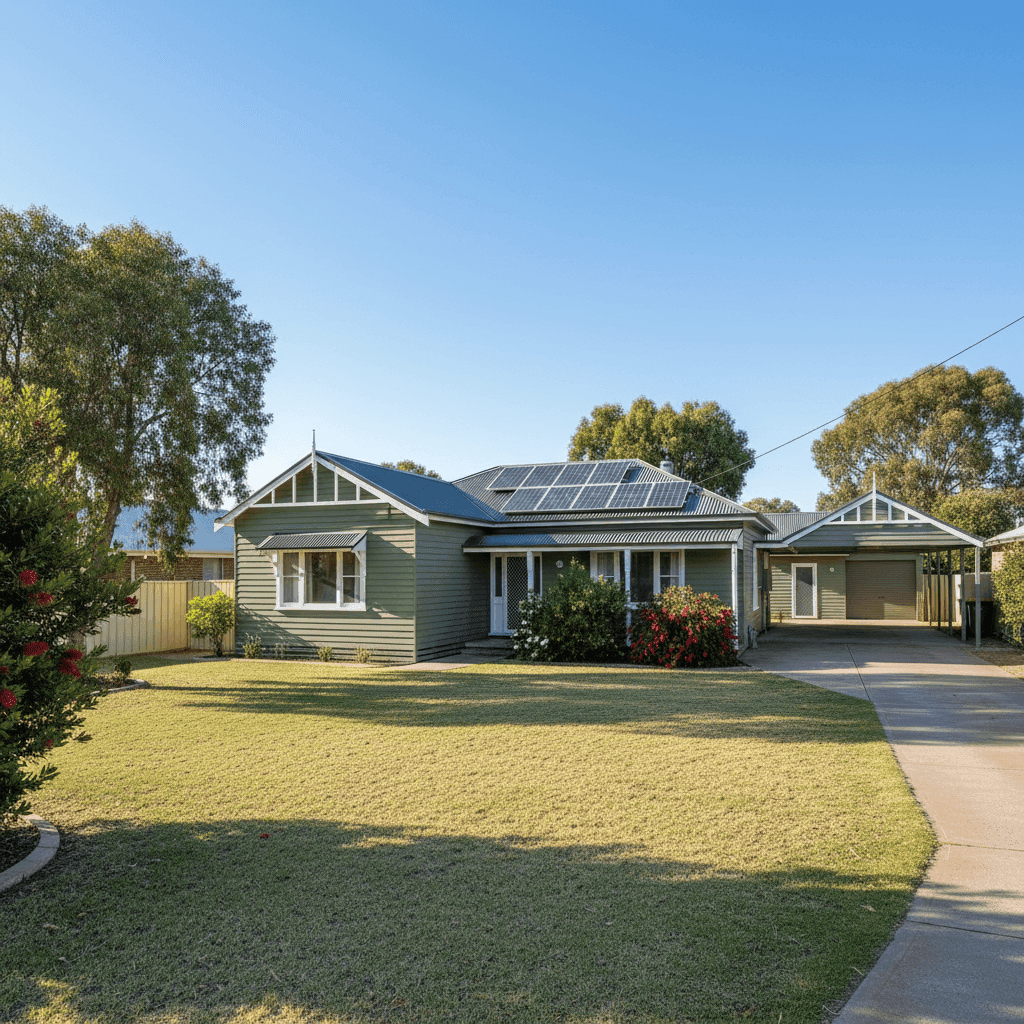

That rating reflects where this premium sits relative to comparable properties in the area. It's not a bargain, but it's also not an outlier. For a 1967-built weatherboard home with a granny flat and solar panels — features that each carry their own risk and replacement cost implications — landing near the middle of the market is a reasonable outcome.

The sum insured of $589,000 is worth noting. For a 186 sqm home with a granny flat and ducted climate control, this figure needs to cover full rebuild costs, not just the market value of the property. In regional NSW, construction costs have risen sharply in recent years, so ensuring your sum insured keeps pace with current building rates is critical.

---

How Moree Compares

To put this quote in context, here's how it measures up across different benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Moree (2400) | $43,287/yr | $3,822/yr |

| NSW | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out immediately. The suburb average of $43,287 is dramatically higher than the median of $3,822 — a strong signal that a small number of very high-value or high-risk properties are pulling the mean upward. With only 18 quotes in our Moree suburb dataset, a single outlier can have an outsized effect on the average. The median is a far more reliable benchmark here, and at $3,822, our quoted premium of $4,276 sits just above it — consistent with a "fair" rating.

The 25th–75th percentile range for Moree runs from $2,538 to $5,113 per year, which means this quote falls comfortably within the middle half of the market. That's a reassuring sign that the insurer has priced the risk in line with what others are paying for similar properties in the area.

Compared to the NSW state median of $3,770 and the national median of $2,764, Moree premiums are slightly elevated — reflecting the region's exposure to flood risk along the Mehi and Gwydir river systems, as well as the prevalence of older housing stock that can be more costly to rebuild to modern standards.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on what insurers charge. Here's what's most relevant:

Weatherboard Timber Walls

Weatherboard construction is one of the most significant premium drivers for older Australian homes. Timber is more susceptible to fire, termite damage, and general deterioration than brick or rendered concrete. Insurers price this risk accordingly, and it's a key reason why a 1967-built home in a regional area may attract a higher base rate than a newer brick veneer property.

Steel/Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, low-maintenance, and performs well in high-wind events. Compared to terracotta tiles or ageing fibrous cement, Colorbond roofing typically doesn't add a significant loading to premiums.

Slab Foundation

A concrete slab foundation is a neutral-to-positive factor in most assessments. It's structurally sound and not prone to the subsidence risks associated with older stumped or timber-framed foundations — which is particularly relevant in Moree, where expansive clay soils can cause movement over time.

Solar Panels

Solar panels are an increasingly common feature, but they do add to the rebuild cost of a home. Insurers need to account for the cost of replacing panels and associated inverter systems, which can add tens of thousands of dollars to a claim. Ensuring your sum insured reflects the replacement value of your solar system is important.

Granny Flat

The presence of a granny flat meaningfully increases both the rebuild cost and the complexity of a claim. Whether it's used for family, rental income, or storage, it adds floor area and fixtures that must be covered under your building policy. This is likely a contributing factor to the higher sum insured of $589,000.

Ducted Climate Control

Ducted air conditioning systems are expensive to replace and are embedded throughout the structure of the home. Like solar panels, they need to be factored into your sum insured — and they're one of the easier items to underinsure if you haven't reviewed your coverage recently.

---

Tips for Homeowners in Moree

1. Review Your Sum Insured Annually

Construction costs in regional NSW have increased significantly. If your sum insured hasn't been updated in the past 12–24 months, there's a real chance you're underinsured. Use a building cost calculator or speak with a local builder to get a current estimate of what it would cost to fully rebuild your home — including the granny flat.

2. Ask About Flood Cover Specifically

Moree sits within a floodplain, and flood cover is not always automatically included in a standard building policy. Check your Product Disclosure Statement carefully to confirm whether flood is covered, and if not, whether it can be added. This is one of the most common gaps in regional NSW home insurance.

3. Consider Your Excess Strategically

This quote carries a $1,000 excess. Opting for a higher excess — say $2,000 or $2,500 — can reduce your annual premium noticeably. If you have the savings to cover a larger out-of-pocket cost in the event of a claim, this can be a smart way to lower your ongoing costs.

4. Compare at Renewal, Not Just at Purchase

Many homeowners set and forget their insurance. But the market shifts, and so does your property's risk profile. Running a fresh comparison at each renewal — especially in a regional market like Moree where insurer appetite can vary — is one of the easiest ways to avoid overpaying.

---

Find a Better Deal with CoverClub

Whether this quote is the right fit for your home depends on your full circumstances — but knowing where you stand is the first step. CoverClub makes it easy to compare building insurance options for properties across regional NSW and beyond. Enter your address and get a quote today to see how your current premium stacks up and whether there's a better deal waiting for you.