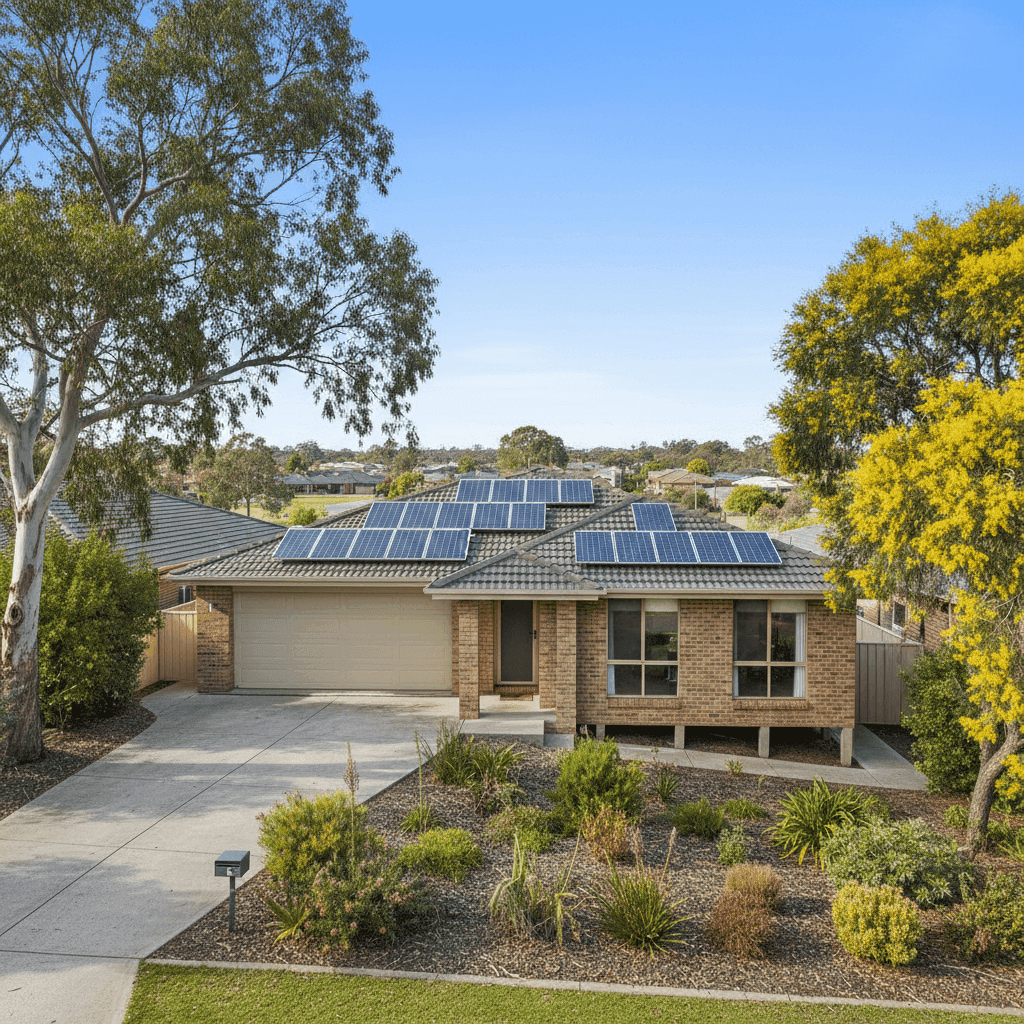

If you own a free standing home in Morisset, NSW 2264, you already know it's a relaxed lakeside community on the western shore of Lake Macquarie — but when the home insurance renewal lands in your letterbox, it can feel anything but relaxing. This article breaks down a real building-only insurance quote for a four-bedroom, four-bathroom brick veneer home in Morisset, comparing it against suburb, state, and national benchmarks so you can make a genuinely informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,828 per year (or $374 per month) for building-only cover, with a $1,000 building excess and a sum insured of $858,000. Our price rating for this quote is Expensive — Above Average.

To put that in perspective, the suburb average for Morisset sits at just $1,966 per year, and the median is even lower at $1,662 per year. That means this particular quote is nearly double the typical premium paid by other homeowners in the same postcode. Even looking at the 75th percentile — the upper end of what most locals pay — the figure is $2,772 per year, still well below this quote.

So what's driving the higher price? A combination of factors is likely at play: the property's age (built in 1983), its stump foundation, timber and laminate flooring, and a relatively high sum insured of $858,000 all contribute to a more complex risk profile in the eyes of insurers. Above-average fittings quality also pushes the rebuild cost — and therefore the premium — upward.

That said, a premium nearly double the suburb average is a strong signal to shop around. One quote from one insurer is rarely the whole story.

---

How Morisset Compares

Understanding where Morisset sits within the broader insurance landscape helps frame whether a high quote is a local quirk or a wider trend.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Morisset (NSW 2264) | $1,966/yr | $1,662/yr |

| NSW (State) | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

| Lake Macquarie LGA | $11,064/yr | — |

A few things stand out here. The NSW state average of $9,528 per year is extraordinarily high — driven largely by elevated premiums in flood-prone, cyclone-risk, and high-value coastal areas across the state. The state median of $3,770 is a more realistic anchor for typical NSW homeowners, and the quote of $3,828 sits just slightly above that median.

Compared to the national average of $5,347 and a national median of $2,764, this quote is above the national midpoint but well below the national average — suggesting the property carries some genuine risk factors, but isn't in the extreme tier.

Interestingly, the Lake Macquarie LGA average of $11,064 per year is remarkably high, which likely reflects the diversity of properties across the LGA — including waterfront homes and areas with flood or storm surge exposure. Morisset's own suburb-level data tells a more modest story, with most locals paying under $2,800 per year.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth examining through an insurer's lens:

Brick veneer construction is generally viewed favourably by insurers — it's durable, fire-resistant, and widely understood. However, it can be more expensive to repair or rebuild than some modern lightweight materials, which can push premiums up when paired with a high sum insured.

Concrete roof tiles are similarly solid performers in terms of durability and weather resistance. Unlike Colorbond or terracotta, concrete tiles are less prone to wind uplift, which is a positive from a risk perspective.

Stump foundation is a notable factor. Homes on stumps — particularly older ones built in 1983 — can be more susceptible to movement, moisture ingress, and termite activity. Insurers may price in additional risk for this foundation type, especially when combined with timber and laminate flooring, which is more vulnerable to water damage than concrete slab flooring.

Solar panels add value to the property and, in some policies, need to be specifically included in the sum insured to be covered. It's worth confirming your policy explicitly covers solar panel damage from storms, hail, or fire.

Ducted climate control is another above-average feature that contributes to the rebuild cost. Systems like these are expensive to replace, and their inclusion in the sum insured is appropriate — but it does lift the overall insured value.

Above-average fittings quality — think stone benchtops, quality cabinetry, and premium fixtures — means the cost to reinstate the home to its current standard is higher than a comparable home with standard fittings. This is accurately reflected in the $858,000 sum insured, but it also means the premium will be higher.

---

Tips for Homeowners in Morisset

1. Get at least three competing quotes. With this quote sitting nearly double the suburb average, there's a real opportunity to find better value. Use a comparison tool like CoverClub to pull multiple quotes side by side without having to ring around individually.

2. Review your sum insured carefully. At $858,000, the sum insured is substantial. Make sure it reflects the actual cost to rebuild — not the market value of the land. Overcooking the sum insured unnecessarily inflates your premium, while underinsuring leaves you exposed. A quantity surveyor or online rebuild calculator can help you land on the right figure.

3. Check your solar panel coverage. Many standard building policies cover solar panels as a fixture, but some have specific exclusions or sub-limits. Given the prevalence of solar in Morisset and across the Lake Macquarie region, it's worth asking your insurer directly whether storm and hail damage to panels is included.

4. Consider your excess strategically. This quote carries a $1,000 building excess. Opting for a higher voluntary excess — say, $2,000 or $2,500 — can meaningfully reduce your annual premium. If you're in a position to self-insure smaller claims, this trade-off often makes financial sense over the long term.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, CoverClub makes it easy to see how your quote stacks up. Our suburb-level data and real quote comparisons mean you're not flying blind. Get a quote for your Morisset home today and find out if you're paying a fair price — or leaving money on the table.