If you own a free standing home in Morningside, QLD 4170, you've probably wondered whether you're paying a fair price for your home insurance — or whether there's room to save. This article breaks down a real home and contents insurance quote for a five-bedroom, three-bathroom property in the suburb, comparing it against local, state, and national benchmarks to help you make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $3,058 per year (or $299/month) for combined home and contents cover, with a building sum insured of $969,000 and contents valued at $100,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average.

That assessment holds up well when you look at the numbers. The suburb average for Morningside sits at $2,795/year, and the median is $2,561/year, based on a sample of 39 quotes. At $3,058, this quote is modestly above the suburb average — roughly 9% higher — which places it comfortably within the upper-middle range for the area. Specifically, it falls just below the 75th percentile of $3,114/year, meaning around three-quarters of comparable quotes in the suburb come in cheaper, but only just.

This isn't a red flag. A larger-than-average home (315 sqm), a pool, solar panels, and premium features like ducted climate control all contribute to a higher rebuilding cost and replacement value, which naturally pushes the premium upward. Given the property's characteristics, paying slightly above the suburb median is entirely reasonable.

---

How Morningside Compares

To put this quote in broader context, it's worth zooming out to state-level and national benchmarks.

| Benchmark | Average | Median |

|---|---|---|

| Morningside (4170) | $2,795/yr | $2,561/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. The Queensland state average of $9,129/year is extraordinarily high — but this figure is heavily skewed by cyclone-prone regions in Far North Queensland, where premiums can be eye-watering. The state median of $3,903/year is a more useful reference point, and against that figure, this Morningside quote looks quite competitive.

It's also worth noting that the LGA average for Brisbane is $16,277/year — an average that is almost certainly distorted by a small number of very high-risk or high-value properties. The national average of $5,347/year tells a similar story, with medians being a far more reliable guide than averages when the data contains extreme outliers.

Against the national median of $2,764/year, this quote is about 10.6% higher — again, not unreasonable for a well-appointed, larger-than-average home with additional features.

For homeowners in Morningside, the takeaway is positive: you're in a suburb where insurance premiums are relatively affordable compared to much of Queensland, and this quote reflects that broader trend.

---

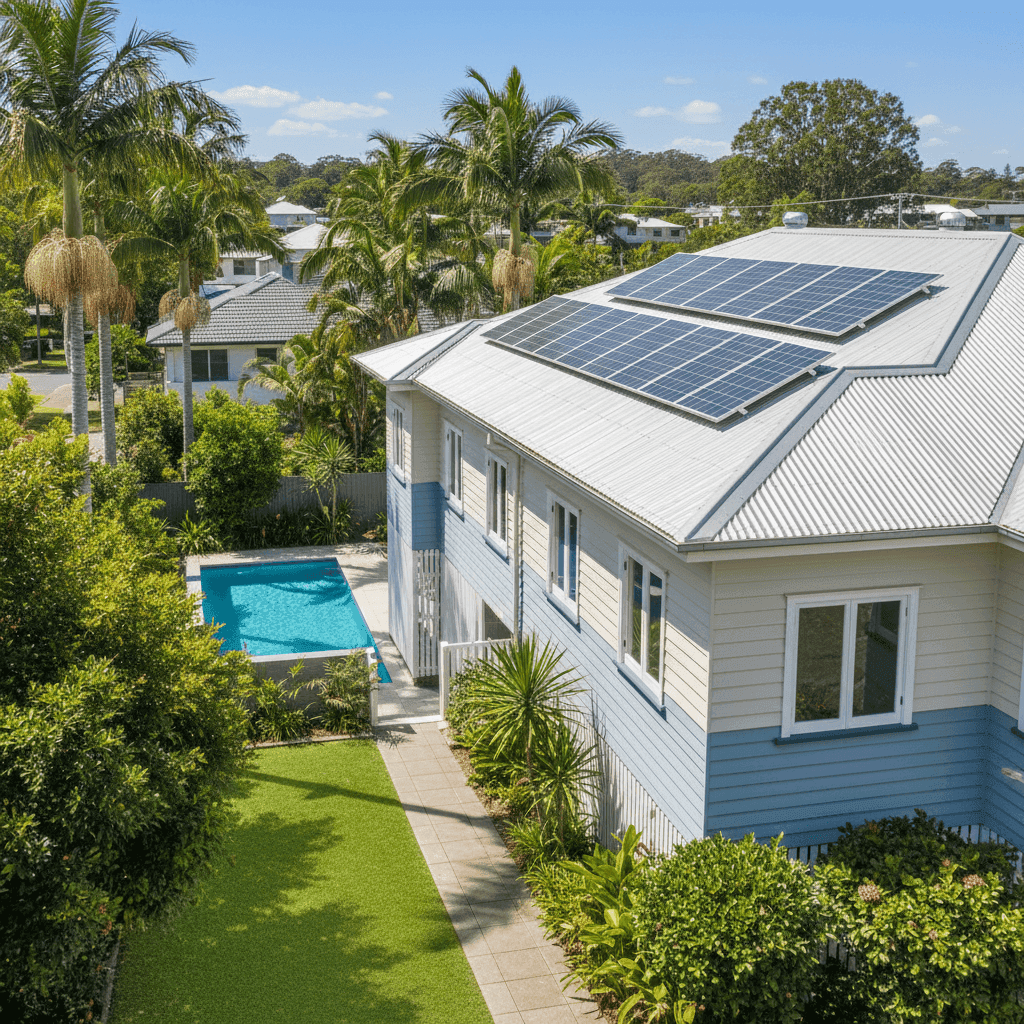

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on the premium quoted.

Size and sum insured: At 315 sqm with a building sum insured of $969,000, this is a substantial home. Larger homes cost more to rebuild, and insurers price accordingly. Ensuring your sum insured accurately reflects current construction costs is critical — underinsurance is a common and costly mistake.

Weatherboard timber walls: Weatherboard construction is charming and common in Brisbane's inner suburbs, but it does carry a higher fire risk than brick veneer or double brick. Some insurers price this risk into their premiums, so it's worth shopping around to find a provider who assesses timber homes competitively.

Steel/Colorbond roof: This is generally viewed favourably by insurers. Colorbond roofing is durable, low-maintenance, and performs well in storms — a meaningful consideration in South East Queensland's storm season.

Concrete slab foundation: Slab foundations are considered stable and are typically associated with lower subsidence risk, which can work in your favour at renewal time.

Swimming pool: Pools add liability exposure and replacement cost to a policy. They're a standard inclusion in many Brisbane homes, but they do nudge premiums upward.

Solar panels: Solar systems are increasingly common, but they represent a meaningful asset that needs to be covered. Ensure your sum insured accounts for the replacement cost of your panels — many homeowners forget to factor this in.

Ducted climate control: Ducted systems are expensive to replace and are typically covered under building insurance. Again, this supports a higher sum insured and contributes to a slightly elevated premium.

No cyclone risk: Morningside is not classified as a cyclone risk area, which is a significant premium advantage compared to properties further north in Queensland.

---

Tips for Homeowners in Morningside

1. Review your sum insured annually Construction costs in South East Queensland have risen sharply in recent years. A building sum insured that was accurate two years ago may no longer reflect what it would actually cost to rebuild your home today. Use a building cost calculator or speak with a quantity surveyor to keep your figure current.

2. Shop around — especially for weatherboard homes Not all insurers assess timber-framed or weatherboard homes the same way. Some apply a higher loading for fire risk; others are more competitive. Comparing multiple quotes through a platform like CoverClub can surface meaningful savings without you having to call around individually.

3. Check that your pool and solar panels are explicitly covered Read your Product Disclosure Statement (PDS) carefully to confirm that your pool equipment and solar panels are included in your building cover. Some policies have sub-limits or exclusions that could leave you underinsured after a storm or hail event.

4. Consider your excess strategically Both excesses on this policy are set at $1,000. Opting for a higher voluntary excess can reduce your annual premium — but only makes sense if you have the cash reserves to cover it in the event of a claim. For a home of this value, a $1,000 excess is reasonable, but it's worth modelling the trade-off at renewal.

---

Compare Your Quote with CoverClub

Whether you're renewing your policy or shopping around for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub makes it easy to benchmark your premium against real data from properties in your suburb and across Australia — so you can walk into renewal negotiations with confidence. Enter your address today and see how your quote stacks up.