Mount Barker is a quiet, characterful town in Western Australia's Great Southern region — known for its rolling farmland, cool-climate wines, and relaxed lifestyle. For homeowners here, securing the right home and contents insurance is an important part of protecting what is likely their most valuable asset. This article takes a close look at a recent insurance quote for a four-bedroom, two-bathroom free standing home in Mount Barker (postcode 6324), breaking down whether the price is competitive and what factors are shaping the premium.

---

Is This Quote Fair?

The annual premium for this home and contents policy came in at $1,633 per year (or $159 per month), covering a building sum insured of $852,000 and $80,000 worth of contents. The building excess is $2,000 and the contents excess is $1,000.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb median premium for Mount Barker sits at $1,623 per year, meaning this quote is almost exactly in line with what most local homeowners are paying. It's comfortably within the middle range of the market — sitting between the 25th percentile ($1,101/yr) and the 75th percentile ($2,087/yr).

In other words, this isn't a bargain-basement price, but it's far from the top of the market either. Given the property's elevated construction, pool, and solar panels — all of which can nudge premiums upward — landing near the median is a reasonable outcome. There's still room to potentially improve, particularly if the homeowner shops around or adjusts their excess levels.

---

How Mount Barker Compares

One of the most striking takeaways from this quote is just how favourably Mount Barker compares to broader benchmarks. Here's a quick snapshot:

| Benchmark | Average Premium |

|---|---|

| Mount Barker (suburb average) | $1,715/yr |

| Mount Barker (suburb median) | $1,623/yr |

| LGA — Denmark | $2,124/yr |

| Western Australia (state average) | $2,144/yr |

| Western Australia (state median) | $1,944/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

Mount Barker homeowners are paying significantly less than the Western Australian state average of $2,144 per year and even more so compared to the national average of $2,965 per year. The suburb average of $1,715 is well below both benchmarks, suggesting that insurers view Mount Barker as a relatively lower-risk location compared to many other parts of Australia.

Interestingly, the local government area (LGA) of Denmark has an average premium of $2,124 — noticeably higher than Mount Barker's own suburb average. This suggests that risk profiles can vary meaningfully even within the same LGA, and that Mount Barker itself is priced more favourably than some surrounding areas.

For context, the suburb sample size used in this analysis is 30 quotes, which provides a reasonable basis for comparison, though it's worth noting that individual premiums can vary considerably depending on the specific insurer, policy features, and property details.

---

Property Features That Affect Your Premium

Several characteristics of this property are worth understanding in the context of insurance pricing.

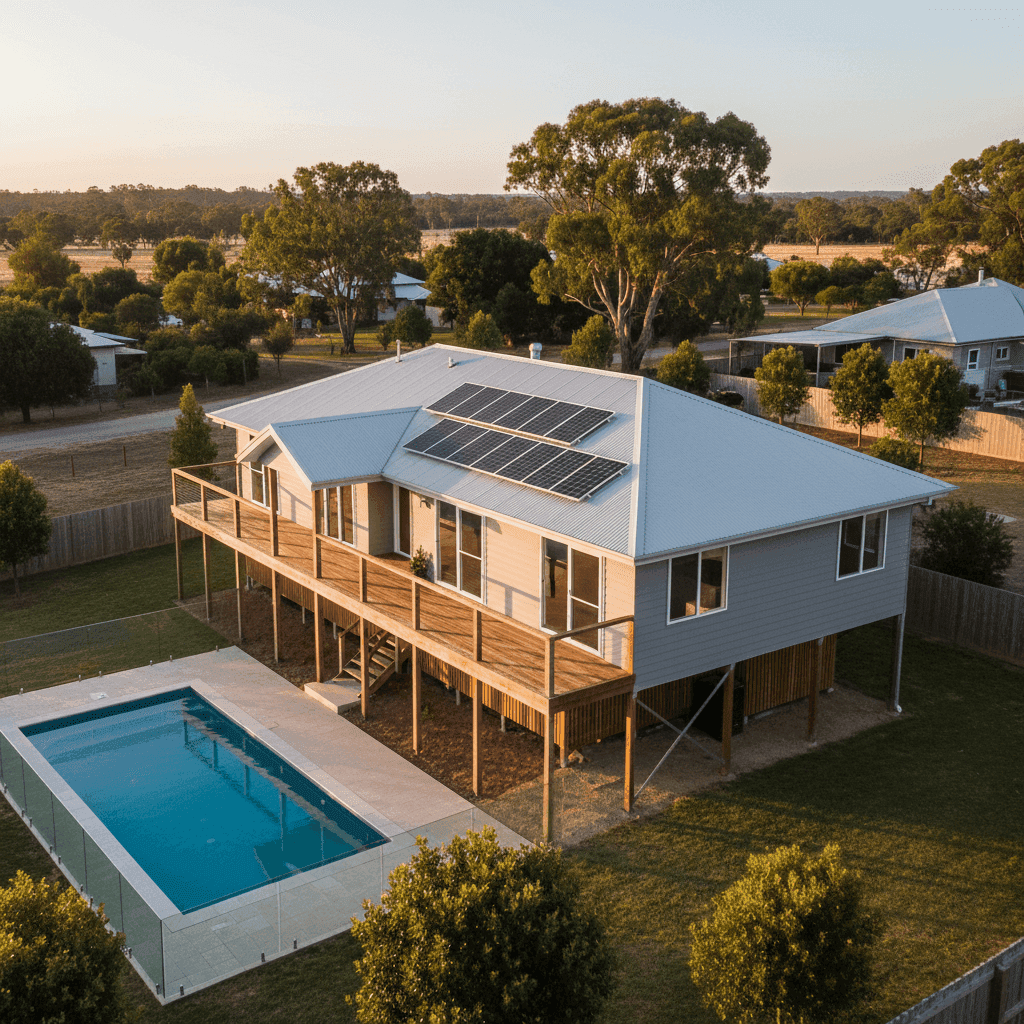

Elevated Foundation (Poles)

This home is elevated by at least one metre on a pole foundation — a construction style that can cut both ways when it comes to insurance. On the positive side, elevation typically reduces flood and stormwater inundation risk. However, elevated homes can be more expensive to repair or rebuild, which may influence the building sum insured and, in turn, the premium. The $852,000 sum insured reflects the cost to rebuild, not the market value of the property.

Hardiplank / Hardiflex External Walls

Fibre cement cladding such as Hardiplank and Hardiflex is a popular choice in regional WA. It's durable, low-maintenance, and performs reasonably well in fire-prone environments — which can be a positive signal for insurers. Compared to older timber weatherboard homes, this material profile is generally viewed as lower risk.

Steel / Colorbond Roof

Colorbond roofing is widely regarded as one of the most resilient roofing options available in Australia. It handles heat, wind, and rain well, and is resistant to corrosion — all factors that tend to be viewed favourably by insurers when assessing risk.

Swimming Pool

The presence of a pool adds to the contents and liability risk profile of a property. Pools require their own maintenance and carry an inherent liability exposure. This is one feature that can nudge premiums upward, and it's worth confirming your policy includes appropriate liability cover.

Solar Panels

Solar panels are increasingly common across regional WA, and most home insurance policies cover them as a fixture of the building. However, it's important to confirm this with your insurer — some policies treat solar systems differently, particularly if they are leased rather than owned outright.

Timber / Laminate Flooring

Timber and laminate floors are considered standard in most policies, though they can be more costly to replace than tiles if water damage occurs. This is a minor factor in premium pricing but worth noting when assessing your contents cover.

---

Tips for Homeowners in Mount Barker

1. Review your building sum insured regularly Construction costs have risen significantly in recent years across regional WA. A sum insured of $852,000 may be appropriate today, but it's worth reassessing annually to ensure it still reflects the true cost to rebuild. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Consider adjusting your excess This policy carries a $2,000 building excess and a $1,000 contents excess. Opting for a higher excess is one of the most straightforward ways to reduce your annual premium. If you have a healthy emergency fund, this trade-off can make financial sense.

3. Shop around at renewal time Loyalty doesn't always pay in insurance. With 30 quotes in the suburb sample ranging from around $1,101 to $2,087 per year, there's clearly meaningful variation in what insurers are charging for similar properties in Mount Barker. Comparing quotes at CoverClub takes only a few minutes and could save you hundreds.

4. Check your pool and solar panel cover Given that this property has both a pool and solar panels, it's worth reading the fine print on your policy. Confirm that your solar system is covered for accidental damage and storm events, and that your liability cover extends to the pool area. If you have guests or young children visiting, this peace of mind is invaluable.

---

Ready to Compare?

Whether you're renewing an existing policy or shopping for the first time, comparing quotes is the single best way to make sure you're not overpaying. Get a home and contents insurance quote at CoverClub and see how your premium stacks up against others in Mount Barker and across WA. It's free, fast, and could make a real difference to your household budget.