Nestled in the Dandenong Ranges foothills of Victoria's Cardinia Shire, Mount Burnett is a semi-rural suburb that offers a peaceful, leafy lifestyle — but one that comes with its own set of insurance considerations. This article breaks down a recent home and contents insurance quote for a four-bedroom, free-standing weatherboard home in Mount Burnett VIC 3781, examining whether the premium is competitive, what's driving the cost, and what local homeowners can do to keep their cover affordable.

---

Is This Quote Fair?

The quoted annual premium of $4,020 per year (or $378/month) for a building sum insured of $829,000 and contents valued at $99,000 has been rated Expensive — above average for this area.

To put that in context, the VIC state average sits at $3,000 per year, with a state median of $2,718. That means this quote is roughly 34% above the state average and about 48% above the state median. Against the national average of $5,347 and national median of $2,764, the picture is more nuanced — it's well below the national average, but notably above the national median.

The Cardinia LGA average of $3,089 per year provides perhaps the most relevant local benchmark, and this quote sits around 30% above that figure. So while it's not in outlier territory on a national scale, it does appear on the higher end for this region of Victoria.

That said, several property-specific features — discussed below — go a long way toward explaining the elevated premium. This isn't necessarily a case of poor value; it may simply reflect the genuine risk profile of this particular home.

---

How Mount Burnett Compares

Without suburb-level aggregate data available for Mount Burnett specifically, we rely on the Cardinia LGA and broader VIC benchmarks to contextualise this quote.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $4,020 |

| Cardinia LGA Average | $3,089 |

| VIC State Average | $3,000 |

| VIC State Median | $2,718 |

| National Average | $5,347 |

| National Median | $2,764 |

Mount Burnett's semi-rural, bushland-adjacent character places it in a different risk category compared to metropolitan Melbourne suburbs. Properties in areas like this often face elevated exposure to bushfire, storm, and falling tree events — all of which influence how insurers price risk. The suburb's location within the Dandenong Ranges corridor is a key factor that underwriters pay close attention to.

Explore more data on home insurance costs across Victoria or check the national overview to see how different states compare.

---

Property Features That Affect Your Premium

Several characteristics of this particular home are likely contributing to the above-average premium. Here's a breakdown of the most significant factors:

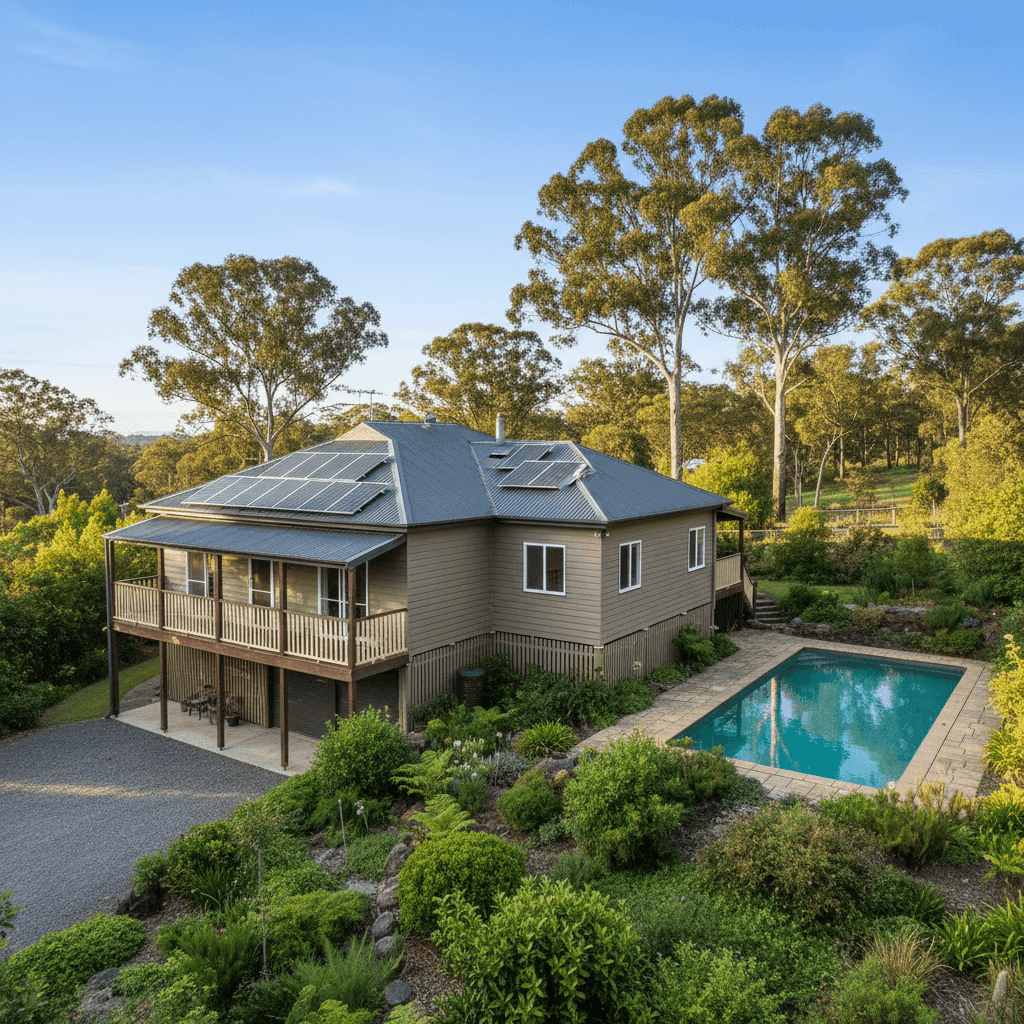

Weatherboard Timber Walls

Weatherboard construction is one of the most common wall types in older Victorian homes, but it is also considered higher risk by insurers — particularly in bushfire-prone regions. Timber is combustible and more vulnerable to fire spread than brick veneer or double-brick alternatives. This will almost certainly be pushing the premium upward.

Steel / Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, resistant to ember attack (a key consideration in bushfire-adjacent areas), and less prone to storm damage than terracotta or concrete tiles. This may be providing a modest offset to some of the other risk factors.

Stump Foundation (Elevated)

The home sits on stumps and is elevated by less than one metre. Elevated homes can be more exposed to wind damage but may also benefit from reduced flood risk in low-lying areas. Timber stumps in particular may require periodic maintenance and replacement, which factors into the overall rebuild cost and insurer risk assessment.

Timber / Laminate Flooring

Timber floors add to the overall rebuild value and are a consideration in the contents and building valuation. High-quality flooring can be expensive to replace, and this is reflected in the building sum insured of $829,000.

Pool, Solar Panels & Ducted Climate Control

These three features each add to the insured value of the property and can increase the premium. Swimming pools introduce liability considerations; solar panel systems (particularly inverters and mounting hardware) add to the replacement cost of the building; and ducted climate control systems are expensive to repair or replace. Together, these inclusions meaningfully contribute to the higher sum insured.

Building Size: 214 sqm

At 214 square metres, this is a generously sized home. Combined with five bathrooms and the premium fittings associated with a well-appointed property, the $829,000 building sum insured appears well-calibrated — though it's always worth checking that your sum insured reflects current construction costs, which have risen significantly in recent years.

---

Tips for Homeowners in Mount Burnett

1. Review Your Sum Insured Regularly

Construction costs in Victoria have increased substantially since 2020. If your building sum insured hasn't been updated recently, you may be underinsured — or conversely, paying for more cover than you need. Use a building cost calculator to verify your figure annually.

2. Consider Bushfire Mitigation Measures

If your property is in or near a Bushfire Attack Level (BAL) rated zone, taking active steps to reduce risk — such as maintaining a defendable space, installing ember-proof vents, or upgrading to fire-resistant materials — may qualify you for discounts with some insurers. It's worth asking directly.

3. Compare Multiple Quotes

The single most effective way to reduce your premium is to compare. A quote rated "expensive" for your area is a clear signal to shop around. Get a comparison quote through CoverClub to see what other insurers are offering for the same level of cover.

4. Assess Your Excess Settings

This policy carries a $5,000 excess for both building and contents — which is on the higher side. While a higher excess typically reduces your premium, it's important to ensure you could comfortably cover that amount in the event of a claim. If cash flow is a concern, a lower excess (even at a slightly higher premium) may be the smarter choice.

---

Compare Your Home Insurance Today

Whether you're a long-time Mount Burnett local or new to the area, it pays to make sure your home insurance is working as hard as you are. A quote rated above average is a prompt to explore your options — and you might be surprised by the savings available. Start a free comparison at CoverClub and see what's out there for your home and contents in Mount Burnett and across Victoria.