Mount Eliza is one of the Mornington Peninsula's most sought-after suburbs — a leafy, coastal community that blends relaxed lifestyle living with proximity to Melbourne. For homeowners here, protecting a well-built, free-standing property is a serious financial consideration. This article takes a close look at a recent building insurance quote for a four-bedroom, three-bathroom brick veneer home in Mount Eliza, comparing it against local, state, and national benchmarks to help you understand whether you're getting a fair deal.

---

Is This Quote Fair?

The quote in question comes in at $1,324 per year (or $138 per month) for building-only cover on a home insured for $736,000. Our price rating for this quote is CHEAP — below average — and the data backs that up convincingly.

To put it in perspective, the average building insurance premium across Mount Eliza sits at $3,816 per year, with a median of $3,570. Even the most competitively priced quarter of quotes in the suburb (the 25th percentile) averages $3,228 per year. This quote comes in at roughly 65% below the suburb median — a remarkable result for a property of this size and specification.

It's worth noting the building excess on this policy is set at $5,000, which is on the higher end. A higher excess is one way insurers reduce the upfront premium, so homeowners should be comfortable covering that amount out of pocket in the event of a claim. If you'd prefer a lower excess, expect the annual premium to rise accordingly.

That said, even accounting for the elevated excess, this quote represents genuinely strong value for a 235 sqm home in a premium suburb.

---

How Mount Eliza Compares

Mount Eliza's insurance pricing sits notably higher than broader benchmarks — a reflection of the suburb's elevated property values, coastal adjacency, and the higher rebuild costs that come with quality construction in the area.

Here's how the numbers stack up:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Mount Eliza (3930) | $3,816/yr | $3,570/yr |

| Mornington Peninsula LGA | $2,652/yr | — |

| Victoria (VIC) | $2,921/yr | $2,694/yr |

| National | $2,965/yr | $2,716/yr |

Interestingly, Victorian premiums sit close to the national average, but Mount Eliza premiums run significantly higher than both — nearly 30% above the state average and around 29% above the national average. This is consistent with what we see across high-value coastal suburbs on the Mornington Peninsula, where rebuild costs and land values push sum-insured figures — and therefore premiums — upward.

The suburb sample of 40 quotes gives us a solid picture of the local market, with a 75th percentile of $4,559 per year showing just how high premiums can climb for properties in this area. Against that backdrop, the $1,324 quote analysed here is exceptional.

---

Property Features That Affect Your Premium

Several characteristics of this property influence how insurers assess risk and calculate premiums. Here's what's relevant:

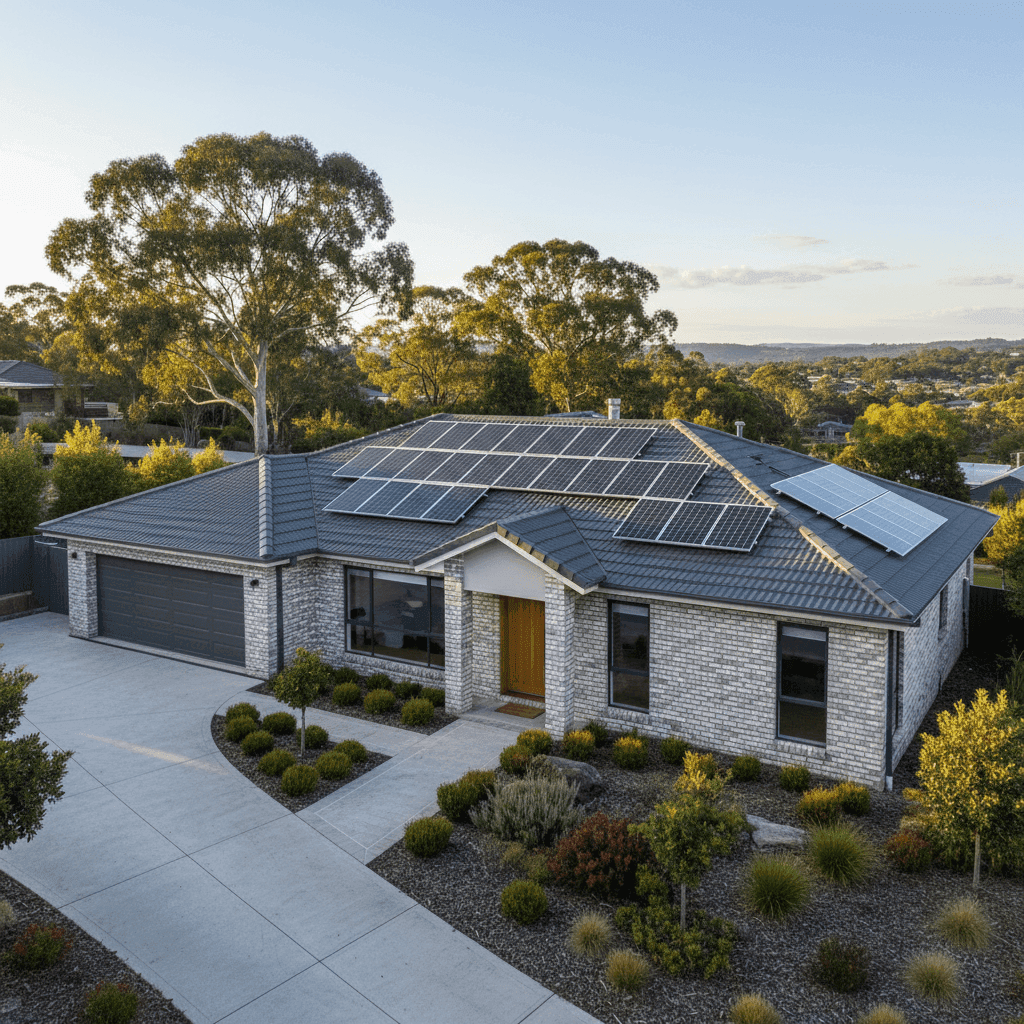

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. These materials are durable, fire-resistant, and widely understood by assessors — which typically translates to more competitive premiums compared to lightweight cladding or older roofing materials like iron or asbestos.

Slab Foundation A concrete slab foundation is the standard for homes built in this era and is considered low-risk. It's less susceptible to subsidence issues than older pier-and-beam foundations, which can be a factor in some parts of Victoria.

Construction Year: 2010 A home built in 2010 benefits from modern building codes introduced after significant updates to Australian Standards. This means better structural integrity, improved fire resistance, and more predictable rebuild costs — all of which can work in your favour when insurers price the risk.

Solar Panels This property has solar panels installed, which is increasingly common across Victoria. Solar panels can add to the replacement cost of a home, and it's important to confirm with your insurer that they are explicitly covered under your building policy. Most modern policies include them, but the sum insured should reflect their value.

Ducted Climate Control Ducted heating and cooling systems are a fixed building asset and should be included in your building sum insured. At 235 sqm, a full ducted system represents a meaningful portion of rebuild cost — something to keep in mind when reviewing whether $736,000 in cover is adequate.

Timber & Laminate Flooring While flooring is typically a building element, the type of flooring can influence rebuild cost estimates. Timber and laminate finishes are mid-range in cost and are factored into standard construction calculators.

No Pool, Standard Fittings The absence of a pool removes a common liability consideration, and standard fittings quality keeps rebuild costs within predictable ranges — both factors that support a more straightforward risk assessment.

---

Tips for Homeowners in Mount Eliza

1. Regularly review your sum insured Building costs have risen sharply across Victoria in recent years. A sum insured set a few years ago may no longer reflect the true cost of rebuilding your home. Use a quantity surveyor or your insurer's rebuild cost calculator to check your coverage annually — underinsurance is a real risk in a suburb where quality construction is the norm.

2. Factor in your excess before choosing a policy This quote carries a $5,000 building excess, which meaningfully reduces the premium. If you're comparing policies, always look at the total cost of ownership — a low premium with a very high excess may not represent the best value if you'd struggle to cover that amount after a significant event.

3. Confirm solar panels are covered If you have solar panels (as this property does), ask your insurer explicitly whether they're included in your building cover and whether the sum insured accounts for their replacement value. Panel costs and installation fees can run into the tens of thousands.

4. Compare quotes — the spread in Mount Eliza is wide With premiums ranging from around $3,228 at the 25th percentile to $4,559 at the 75th percentile, there's clearly significant variation among insurers for similar properties in this suburb. Shopping around can make a substantial difference. Get a quote through CoverClub to see what multiple insurers will offer for your specific property.

---

Ready to See What Your Home Would Cost to Insure?

Whether you're a long-time Mount Eliza resident or new to the area, it pays to know where your premium stands relative to the market. CoverClub makes it easy to compare building and contents insurance quotes side by side, with transparent pricing data drawn from real quotes across your suburb, state, and nationally. Start your comparison today and make sure you're not paying more than you need to.