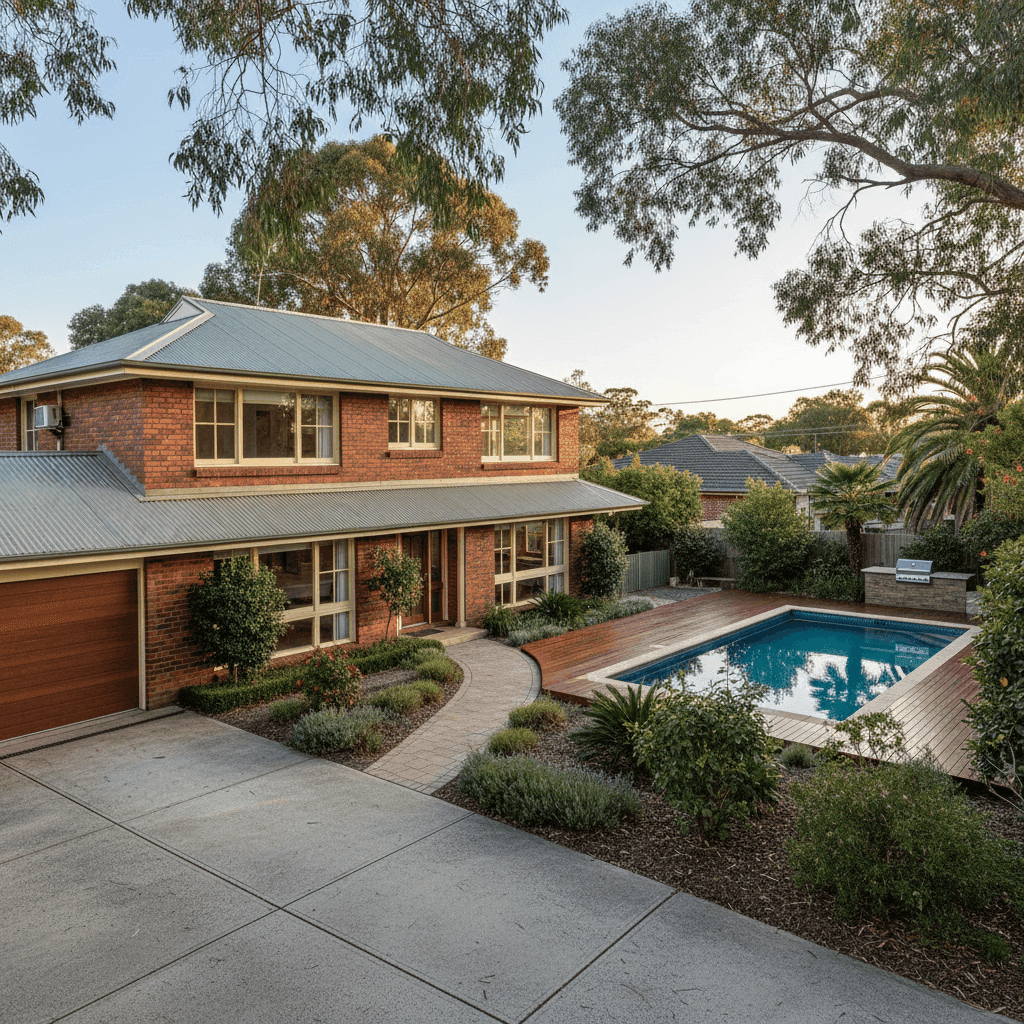

Mount Eliza is one of the Mornington Peninsula's most sought-after suburbs — a leafy, coastal community with a mix of established homes and prestige properties. For owners of a three-bedroom, free-standing home in this area, understanding what you should be paying for home and contents insurance is just as important as choosing the right policy. This article breaks down a real quote for a property in Mount Eliza, compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value on your cover.

---

Is This Quote Fair?

The quote in question sits at $1,533 per year (or $147/month) for combined home and contents insurance, covering a building sum insured of $637,000 and contents valued at $80,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is FAIR — Around Average, which is a solid outcome for a property of this type and age.

To put that in context, the 25th percentile of quotes we've seen for Mount Eliza (VIC 3930) sits at $1,494/yr, meaning this quote is only marginally above the cheapest quarter of the market. The suburb median is $1,874/yr, so this homeowner is paying noticeably less than half of their neighbours. That's a meaningful saving worth acknowledging.

It's also worth noting that a "Fair" rating doesn't mean you can't do better — it simply means the quote is competitive without being exceptional. There may still be room to improve, particularly if the homeowner hasn't recently shopped around or reviewed their sum insured.

---

How Mount Eliza Compares

One of the most useful ways to assess any insurance quote is to zoom out and look at the broader picture. Here's how this quote stacks up across different comparison points:

| Benchmark | Premium |

|---|---|

| This Quote | $1,533/yr |

| Suburb 25th Percentile | $1,494/yr |

| Suburb Median | $1,874/yr |

| Suburb Average | $2,346/yr |

| Suburb 75th Percentile | $3,366/yr |

| LGA Average (Mornington Peninsula) | $2,652/yr |

| VIC State Average | $3,000/yr |

| VIC State Median | $2,718/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

A few things stand out here. First, this quote is 35% below the Mount Eliza suburb average and nearly 44% below the broader Mornington Peninsula LGA average. Second, compared to the Victorian state average of $3,000/yr, this quote represents a saving of roughly $1,467 annually — that's real money back in your pocket.

When you look at the national picture, the contrast is even more striking. The national average of $5,347/yr reflects the outsized impact of high-risk regions — particularly in Queensland and northern Australia, where cyclone and flood exposure drives premiums significantly higher. Mount Eliza, by comparison, benefits from a relatively benign risk profile, which helps keep premiums more manageable.

Based on a sample of 27 quotes for the suburb, the spread is wide — from $1,494/yr at the 25th percentile to $3,366/yr at the 75th. That's a range of nearly $1,900, which underscores just how much variation exists between insurers for the same suburb. Shopping around genuinely pays off here.

---

Property Features That Affect Your Premium

Several characteristics of this property influence the premium, both positively and negatively. Here's what matters most:

Brick Veneer Walls Brick veneer is one of the most common — and insurer-friendly — external wall types in Victoria. It offers good fire resistance and durability, which generally attracts more competitive premiums compared to timber-clad or fibre cement homes.

Steel/Colorbond Roof A Colorbond roof is viewed favourably by most insurers. It's lightweight, resistant to fire and corrosion, and requires relatively little maintenance. This is a positive factor for the premium.

Stump Foundation The property sits on stumps, which is common for homes built in the 1970s in Victoria. While stumps can be a maintenance consideration (particularly older hardwood or concrete stumps that may need relevelling), they don't typically attract a significant premium penalty — and can actually make the home more resilient to certain ground movement events.

Timber/Laminate Flooring Timber and laminate floors are a factor in contents and building replacement costs. Above-average fittings quality — as noted for this property — will push the sum insured higher, but it also ensures the home can be properly rebuilt to its current standard in the event of a total loss.

Swimming Pool A pool adds liability exposure and increases the overall replacement cost of the property. Insurers factor this in, and it's one reason why premiums in pool-owning households tend to trend slightly higher. Ensuring your policy explicitly covers pool infrastructure (fencing, pumps, filtration systems) is worth confirming.

Ducted Climate Control Ducted heating and cooling systems are a fixed building asset that contributes to the rebuild cost. At $637,000 sum insured for a 139 sqm home, the coverage appears to account appropriately for the quality of inclusions.

Construction Year: 1972 A home built in 1972 is over 50 years old. Older homes can attract slightly higher premiums due to ageing infrastructure (wiring, plumbing), though the brick veneer and Colorbond roof suggest the property has been well-maintained or updated over time.

---

Tips for Homeowners in Mount Eliza

1. Review Your Sum Insured Regularly Building costs have risen sharply in Victoria over the past few years. A sum insured of $637,000 for a 139 sqm home with above-average fittings seems reasonable, but it's worth checking against current construction cost estimates annually. Being underinsured is one of the most common — and costly — mistakes homeowners make.

2. Don't Overlook Pool and Liability Cover If you have a swimming pool, make sure your policy includes public liability cover that explicitly addresses pool-related incidents. Check whether pool equipment is covered under building or contents, and confirm there are no exclusions tied to pool fencing compliance.

3. Compare at Renewal, Not Just at Purchase Insurance loyalty rarely pays. The wide premium spread in Mount Eliza — from $1,494 to $3,366/yr for similar properties — shows that different insurers price this suburb very differently. Set a reminder to compare quotes at least 30 days before your renewal date.

4. Check Your Excess Strategy Both excesses on this policy are set at $1,000. Increasing your excess can reduce your annual premium, while lowering it means less out-of-pocket cost at claim time. Think about your financial buffer and choose an excess level that reflects your actual risk tolerance, not just the default.

---

Ready to Compare Home Insurance in Mount Eliza?

Whether you're renewing an existing policy or insuring a new purchase, it pays to see what the market is offering. CoverClub makes it easy to compare home and contents quotes tailored to your property's specific features and location. Get a quote today and see how your current premium stacks up — you might be surprised at the savings available.

For more data on insurance costs in your area, visit the Mount Eliza suburb stats page or explore the full Victorian overview.