If you own a free standing home in Mount Elliot, NSW 2250, you're likely no stranger to the task of making sure your biggest asset is properly protected. This Central Coast suburb sits within the Gosford area — a region known for its leafy streets, established homes, and proximity to both bushland and coast. All of those factors can play a meaningful role in what you pay for home and contents insurance.

In this article, we break down a real home insurance quote for a five-bedroom, two-bathroom free standing home in Mount Elliot, examining how the annual premium stacks up against state and national benchmarks — and what property features are likely pushing the price in either direction.

---

Is This Quote Fair?

The quote in question comes in at $6,353 per year (or $609 per month) for combined home and contents cover, with a building sum insured of $1,004,000 and contents valued at $50,000. Both the building and contents excess are set at $2,000.

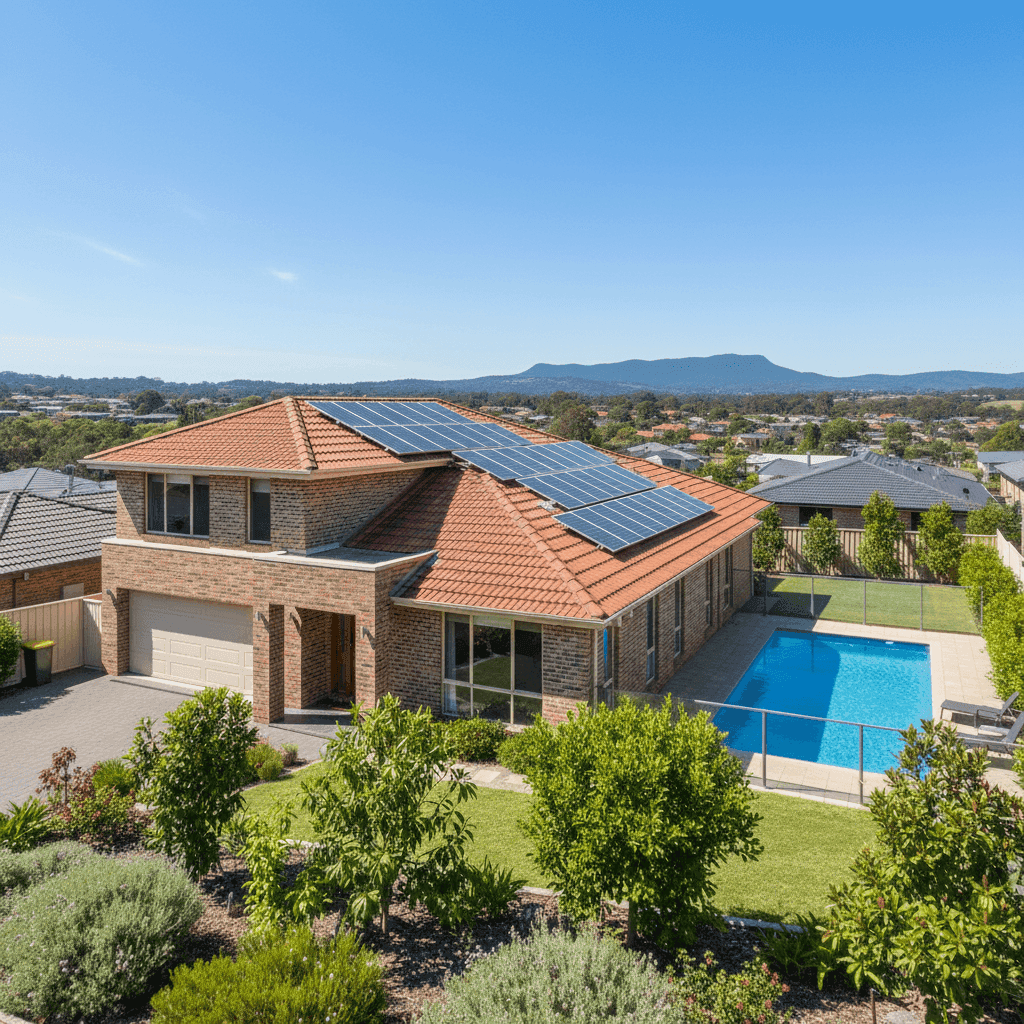

Our pricing analysis rates this quote as CHEAP — below average for the area. That's genuinely good news for the homeowner. When you consider the size of the property (235 sqm), its age (built in 1979), and the extras like a swimming pool and solar panels, landing below average is a solid outcome.

The below-average rating reflects a combination of favourable property characteristics and the insurer's risk assessment. It doesn't mean the cover is lacking — it simply means this particular property profile is attracting competitive pricing relative to what most Australians are paying.

---

How Mount Elliot Compares

Understanding where your premium sits in context makes it far easier to judge whether you're getting value. Here's how this quote compares across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $6,353 |

| NSW Average | $9,528 |

| NSW Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

| Hawkesbury LGA Average | $10,350 |

A few things stand out here. The quote sits 33% below the NSW state average of $9,528, and it also comes in below the NSW state benchmark for home insurance more broadly. Compared to the national average of $5,347, this quote is about 19% higher — but that's largely explained by the higher building sum insured of just over $1 million, which is above the typical insured value for an average Australian home.

The Hawkesbury LGA average of $10,350 per year is particularly telling. Properties in this LGA often attract elevated premiums due to flood exposure, bushfire risk, and older housing stock — so sitting well beneath that figure is a meaningful advantage for this Mount Elliot homeowner.

You can explore localised pricing data for this postcode at the Mount Elliot suburb stats page.

---

Property Features That Affect Your Premium

Every home tells its own risk story, and insurers price accordingly. Here's how the key features of this property are likely influencing the premium:

Brick Veneer Walls Brick veneer is generally viewed favourably by insurers. It offers solid fire resistance and durability compared to timber or weatherboard cladding, which can translate to lower premiums. For a home built in 1979, brick veneer construction is a common and well-regarded choice.

Tiled Roof Terracotta or concrete tiles are considered a lower-risk roofing material than, say, corrugated iron or older asbestos sheeting. Tiles are durable, fire-resistant, and widely accepted by insurers — a tick in the right column for this property.

Slab Foundation A concrete slab foundation is stable and typically associated with lower subsidence or movement risk compared to stumped or pier-and-beam homes. It also means no underfloor space for moisture or pest issues to develop undetected.

Swimming Pool A pool adds to the replacement cost of the property and introduces some liability considerations. Insurers will factor in the cost to repair or replace the pool and associated equipment, which contributes to a higher building sum insured.

Solar Panels Solar panels are increasingly common on Australian rooftops, and most insurers now account for them in the building sum insured. They add to the rebuild cost and can be damaged by hail or storms, so their presence is relevant to how the premium is calculated.

Slight Elevation (Less Than 1m) The property is noted as being slightly elevated — less than one metre. This modest elevation can provide some protection from surface water ingress during heavy rainfall, which may be a minor positive factor in flood-prone areas.

Built in 1979 Homes from this era can carry some additional risk due to ageing plumbing, wiring, and roofing materials. However, many 1970s homes have been well maintained or partially renovated, and brick veneer construction from this period tends to age reasonably well.

---

Tips for Homeowners in Mount Elliot

Whether you're reviewing your current policy or shopping around for the first time, here are four practical steps worth taking:

- Review your building sum insured annually. Construction costs have risen significantly in recent years. A sum insured of $1,004,000 for a 235 sqm home looks reasonable, but it's worth cross-checking against a building cost calculator each year to ensure you're not underinsured — or paying to insure more than you'd need to rebuild.

- Check what your policy says about your pool and solar panels. Not all policies treat these features the same way. Some insurers include solar panels under building cover automatically; others require them to be listed separately. Similarly, confirm whether pool equipment (pumps, filters, heating) is covered and up to what limit.

- Consider increasing your excess to reduce your premium. With both building and contents excesses set at $2,000, there may be room to adjust. Raising your excess can meaningfully lower your annual premium — just make sure you have the funds readily available if you need to make a claim.

- Compare quotes before your renewal date. The insurance market shifts constantly, and loyalty doesn't always pay. Use a comparison tool like CoverClub to check whether a better deal is available before automatically renewing with your current insurer.

---

Ready to Compare?

Whether this quote is your current policy or one you're considering, it pays to know your options. At CoverClub, we make it easy to compare home and contents insurance quotes across Australia — so you can be confident you're getting the right cover at a fair price.

Get a home insurance quote today and see how your property stacks up.