If you own a free standing home in Mount Louisa, QLD 4814, you already know that insuring a property in Townsville's north-western suburbs comes with its own set of considerations — cyclone exposure chief among them. This article breaks down a real building insurance quote for a four-bedroom, two-bathroom concrete home in the area, and puts the $3,020 annual premium into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes, broadly speaking — this quote has been rated Fair (Around Average), and the numbers back that up.

At $3,020 per year (or roughly $295 per month), this building-only policy sits comfortably below the Mount Louisa suburb average of $4,336/yr and also comes in under the suburb median of $3,405. In fact, it lands just above the 25th percentile of $2,865 — meaning this homeowner is paying less than the majority of comparable quotes sampled in the area, while still being within a reasonable range of what most locals pay.

That said, "fair" doesn't mean "the best available." There's still meaningful room between this premium and the cheapest quotes on the market in Mount Louisa, so it's always worth shopping around before renewing.

---

How Mount Louisa Compares

To really appreciate where this quote sits, it helps to zoom out and look at the broader picture.

| Benchmark | Premium |

|---|---|

| This quote | $3,020/yr |

| Mount Louisa suburb average | $4,336/yr |

| Mount Louisa suburb median | $3,405/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| Townsville LGA average | $7,258/yr |

A few things stand out here. First, the Townsville LGA average of $7,258 is extraordinarily high — more than double this quote and well above even the Queensland state average of $4,547. This reflects the significant cyclone and weather risk that insurers price into properties across the broader Townsville region. Mount Louisa, as a suburb within that LGA, benefits from some variation at the local level, but the elevated risk profile is undeniable.

Second, this quote is actually very close to the national average of $2,965 — which is somewhat surprising given the cyclone-prone location. This suggests the property's construction attributes (more on those below) are doing some heavy lifting in keeping the premium competitive.

The suburb sample size of 15 quotes is relatively modest, so averages can shift as more data comes in. You can track the latest figures on the Mount Louisa insurance stats page.

---

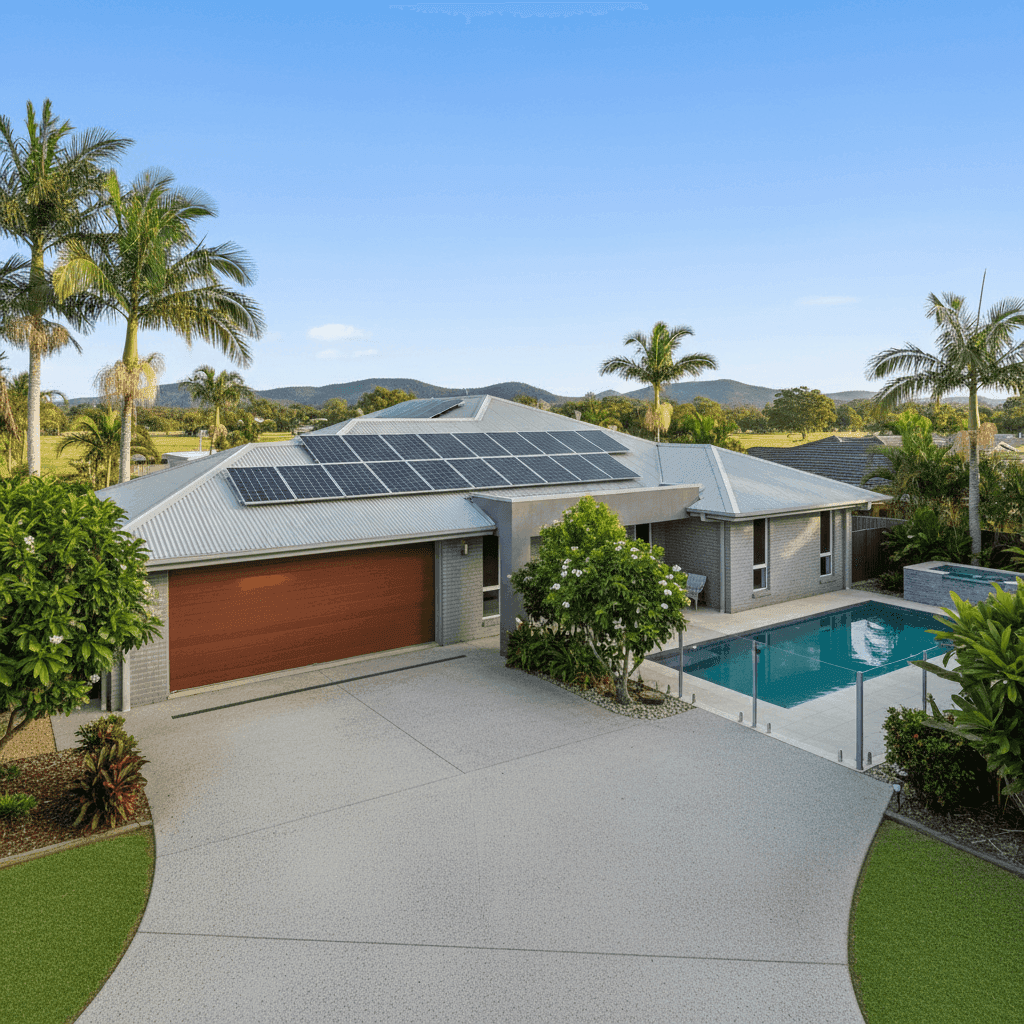

Property Features That Affect Your Premium

This particular home has several characteristics that insurers assess closely. Here's how they likely influence the final premium:

🏗️ Concrete Walls & Colorbond Roof

Concrete external walls are among the most resilient construction materials available, offering strong resistance to wind, impact, and fire. Combined with a steel Colorbond roof — which is well-regarded for its durability in high-wind and cyclone-prone environments — this home presents a lower structural risk profile than timber-framed or brick-veneer alternatives. These features almost certainly contribute to a more competitive premium.

🏠 Slab Foundation & Tile Flooring

A concrete slab foundation provides excellent stability and reduces the risk of subsidence or flood-related underfloor damage. Tiled flooring throughout is similarly practical — it's durable, easy to repair, and less susceptible to water damage than carpet or timber. Both factors are viewed favourably by underwriters.

☀️ Solar Panels

Solar panels add value to the property but also introduce some risk — they can be damaged by hail, high winds, or cyclone debris. Homeowners should confirm whether their policy covers solar panels as part of the building sum insured or whether a separate endorsement is required.

🏊 Swimming Pool

A pool increases the replacement cost of the property and is typically included in the building sum insured. It also introduces liability considerations, though these are generally covered under building policies. The $956,000 sum insured on this policy appears to account for the pool and other permanent fixtures.

❄️ Ducted Climate Control

Ducted air conditioning systems are a significant fixed asset in Queensland homes. As a built-in system, it's generally covered under building insurance, but it's worth checking the policy schedule to confirm coverage limits for mechanical breakdown versus storm or cyclone damage.

🌀 Cyclone Risk Area

Mount Louisa sits within a designated cyclone risk zone, and this is perhaps the single biggest factor driving insurance costs in the region. Insurers apply cyclone-specific excess clauses and loading to premiums in these areas. The $2,000 building excess on this policy is worth noting — in cyclone-prone areas, some policies carry a separate (and often higher) cyclone excess on top of the standard excess, so it's critical to read the Product Disclosure Statement carefully.

---

Tips for Homeowners in Mount Louisa

Whether you're reviewing your current policy or shopping for a new one, here are four practical steps to make sure you're getting the best deal:

- Check for a separate cyclone excess. Many insurers in North Queensland apply a dedicated cyclone excess that's separate from — and often much higher than — the standard building excess. Make sure you know what you'd actually pay out of pocket after a cyclone event before you commit to a policy.

- Review your sum insured annually. Construction costs in Queensland have risen sharply in recent years. A sum insured of $956,000 may be appropriate today, but underinsurance is a real risk if building costs continue to climb. Use a building cost calculator or speak to a quantity surveyor to validate your figure each year.

- Confirm solar panel coverage. Solar panels are a significant investment, and not all policies cover them automatically or to their full replacement value. Ask your insurer specifically how panels are covered — particularly for cyclone and hail damage.

- Compare quotes before renewing. Loyalty rarely pays in the insurance market. Given that this suburb's average premium is $1,316 higher than this quote, there's clearly wide variation in what insurers charge for the same property. Running a fresh comparison at renewal could save you hundreds of dollars.

---

Compare Your Home Insurance Quote Today

Whether you're a Mount Louisa local or looking at property elsewhere in Queensland, CoverClub makes it easy to see how your premium stacks up. Get a building insurance quote now and compare it instantly against suburb, state, and national benchmarks — so you always know if you're paying a fair price.