Getting a competitive home insurance quote in North Queensland is no small feat. For homeowners in Mount Low, QLD 4818, a coastal suburb in the Townsville region, premiums can vary wildly depending on a property's age, construction, and exposure to natural hazards. This article takes a close look at a real quote for a three-bedroom, free-standing home in Mount Low — and unpacks what's driving the price.

---

Is This Quote Fair?

The quote in question comes in at $3,585 per year (or $359/month) for combined home and contents cover, with a building sum insured of $498,000 and contents valued at $83,000. The building excess is $3,000 and the contents excess sits at $1,000.

Our pricing model rates this quote as CHEAP — below average for the area. That's a meaningful finding, because insurance in Mount Low and the broader Townsville LGA is anything but cheap. The fact that this quote lands well below the local average suggests the policyholder is getting solid value relative to what most comparable properties are paying.

To put it in perspective: the suburb average premium in Mount Low is $7,931/year, and the median sits at $5,492/year. This quote falls below even the 25th percentile of $3,899/year, meaning it's cheaper than at least 75% of quotes sampled in the area. That's a strong result in a market where cyclone exposure and building costs consistently push premiums higher.

---

How Mount Low Compares

Understanding where Mount Low sits in the broader insurance landscape helps explain why even a "cheap" quote here might surprise homeowners who've only ever insured property in southern states.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,585 |

| Mount Low 25th Percentile | $3,899 |

| Mount Low Median | $5,492 |

| Mount Low Average | $7,931 |

| Mount Low 75th Percentile | $7,220 |

| Townsville LGA Average | $7,340 |

| QLD State Average | $4,547 |

| QLD State Median | $3,931 |

| National Average | $2,965 |

| National Median | $2,716 |

Compared to the Queensland state average of $4,547/year, this quote is noticeably cheaper — roughly 21% below the state average. Against the national average of $2,965/year, it does sit higher, which reflects the elevated risk profile of insuring property in cyclone-prone North Queensland.

The Townsville LGA average of $7,340/year is particularly telling. Across the region, homeowners are routinely paying double what this quote is offering. The gap between this result and the LGA average underscores just how much premiums can vary — and why comparing quotes is so important.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence what insurers charge. Here's how they play out:

Cyclone Risk Area

This is the single biggest factor. Mount Low falls within a designated cyclone risk zone, and insurers price this in significantly. Cyclone cover adds substantial cost to any policy in the region, and most standard policies include a separate cyclone excess. Homeowners in this area should always check whether their policy covers cyclone damage and what the specific excess conditions are.

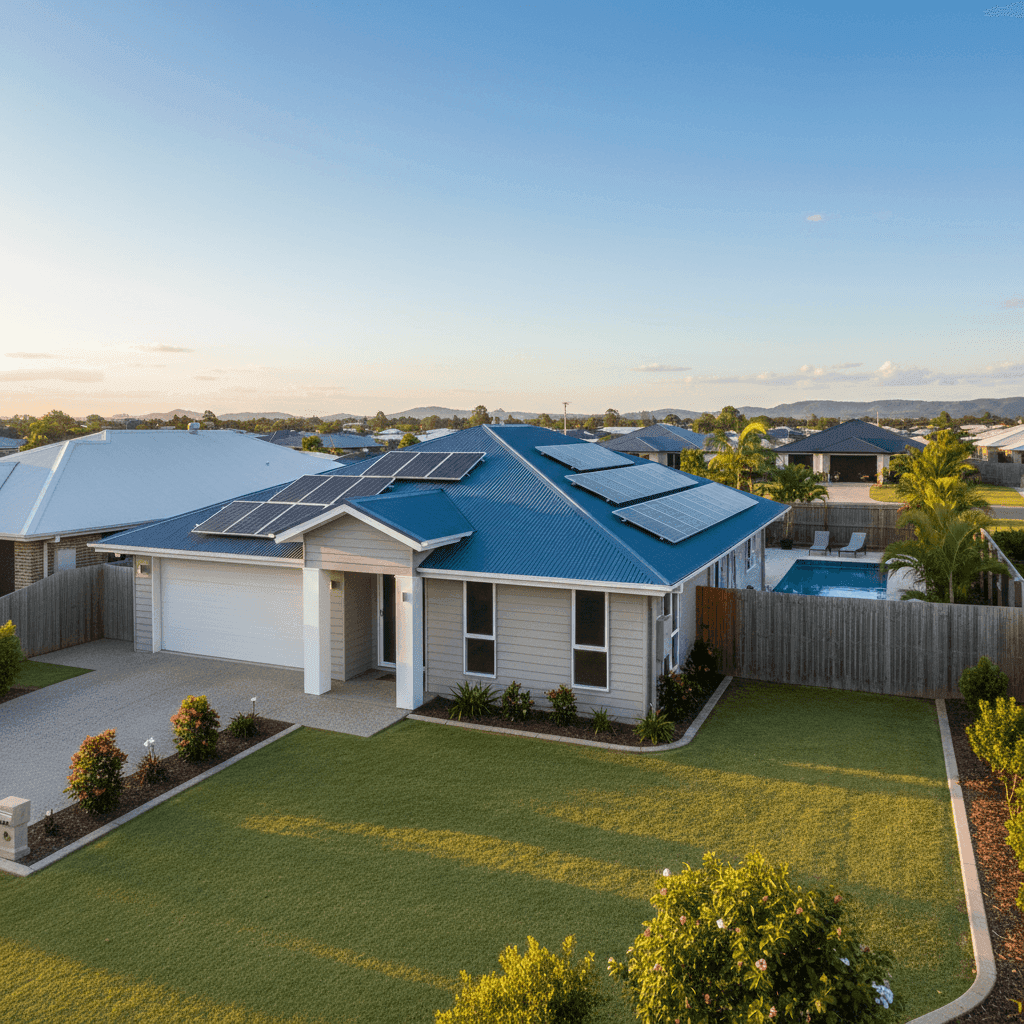

Construction: Hardiplank/Hardiflex Walls & Colorbond Roof

The external walls are Hardiplank Hardiflex — a fibre cement cladding that's widely used in Queensland and generally viewed favourably by insurers for its durability and fire resistance. Paired with a steel Colorbond roof, this construction type is considered robust and relatively low-risk compared to older materials like weatherboard or terracotta tiles, which can be more vulnerable to wind and storm damage.

Slab Foundation & Tiled Flooring

A concrete slab foundation is common in Queensland and is generally regarded as structurally sound and less prone to subsidence or termite ingress. Tile flooring is similarly practical in this climate — durable, easy to maintain, and less susceptible to moisture damage than timber or carpet.

Pool & Solar Panels

Both a swimming pool and solar panels are present on this property. Pools can add a modest amount to premiums due to liability considerations, while solar panels increase the insured value of the home and may add a small premium loading. It's worth confirming that your policy explicitly covers solar panels — not all standard policies do, and some require them to be listed separately.

Built in 1993

At around 30 years old, this home is neither brand new nor particularly aged. Properties from the early 1990s in Queensland were generally built to reasonable standards, though they predate some of the stricter cyclone-resistant building codes introduced after Cyclone Larry (2006) and updated post-Yasi (2011). Insurers may factor in the age and construction era when assessing risk.

Standard Fittings

With standard-quality fittings, the rebuild cost estimate of $498,000 for a 130 sqm home reflects current construction costs in regional Queensland, which have risen sharply in recent years. It's worth reviewing your sum insured regularly to ensure it keeps pace with building cost inflation.

---

Tips for Homeowners in Mount Low

1. Review your cyclone excess carefully Many insurers apply a separate, higher excess for cyclone-related claims — sometimes 1–2% of the sum insured. On a $498,000 policy, that could mean an out-of-pocket cost of $5,000–$10,000 before your insurer pays anything. Make sure you understand this before a storm season arrives.

2. Keep your sum insured up to date Construction costs in Queensland have increased significantly since 2020. If your building sum insured hasn't been reviewed recently, you may be underinsured. Use a building cost calculator or speak with a quantity surveyor to get a current estimate, and update your policy accordingly.

3. Confirm solar panel coverage If your solar system isn't explicitly listed in your policy schedule, it may not be covered — or may only be partially covered. Ask your insurer directly and get confirmation in writing. Given the cost of replacing a solar system, this is worth the five-minute phone call.

4. Compare quotes at renewal, every year As this quote demonstrates, premiums in Mount Low vary enormously — from under $3,900 at the 25th percentile to over $7,200 at the 75th percentile. Loyalty doesn't always pay in insurance. Shopping around at renewal could save thousands annually, particularly in a high-premium market like Townsville.

---

Compare Your Own Quote

Whether you're a first-time buyer or a long-time homeowner in Mount Low, it pays to know where your premium stands. CoverClub makes it easy to benchmark your quote against real data from your suburb, state, and across Australia. Get a quote today at CoverClub and see how your premium stacks up — you might be surprised by what you find.