Mountain Creek is a well-established residential suburb on Queensland's Sunshine Coast, sitting just inland from Mooloolaba and a short drive from the region's famous beaches. It's a popular choice for families, thanks to its proximity to schools, parklands, and the University of the Sunshine Coast. For homeowners here, understanding what you should be paying for home insurance — and why — is an important part of protecting one of your biggest assets.

This article breaks down a real home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Mountain Creek, comparing it against local, state, and national benchmarks to help you understand whether it represents fair value.

---

Is This Quote Fair?

The quote in question comes in at $3,119 per year (or $299 per month) for combined home and contents cover, with a building sum insured of $728,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our pricing analysis rates this quote as CHEAP — below average for the area. That's a positive result for the homeowner. To put it in perspective:

- The suburb median for Mountain Creek is $4,760/yr — meaning this quote is roughly $1,641 cheaper than what half of comparable properties are paying.

- The suburb 25th percentile sits at $3,392/yr, so this quote even undercuts the cheapest quarter of local premiums by over $270.

- Against the QLD state median of $3,903/yr, this quote still comes in below the midpoint.

In short, this is a competitive result. It suggests the insurer has assessed the risk profile of this property favourably — which, as we'll explore below, is likely influenced by several of the home's physical characteristics.

---

How Mountain Creek Compares

Mountain Creek sits within the Sunshine Coast LGA, where the average premium is $7,249/yr. That figure is heavily skewed upward by high-risk or high-value properties in the region — particularly those closer to the coast or in cyclone-prone zones. The suburb average for Mountain Creek itself is a striking $41,962/yr, though this is almost certainly distorted by a small sample size (26 quotes) and a handful of outlier properties with very high sums insured or elevated risk profiles. The median of $4,760/yr is a far more reliable indicator of what most homeowners are actually paying.

Zooming out to the state level, Queensland premiums average $9,129/yr — one of the highest in the country, largely due to the prevalence of cyclone risk, flooding, and severe storm events across much of the state. Mountain Creek, however, is not classified as a cyclone risk area, which is a meaningful factor in keeping premiums more manageable here.

At the national level, the average premium is $5,347/yr and the median sits at $2,764/yr. The quote we're analysing falls neatly between the national median and average — a reasonable position for a well-appointed four-bedroom home with a pool and solar panels in a desirable coastal-adjacent suburb.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to insurance pricing:

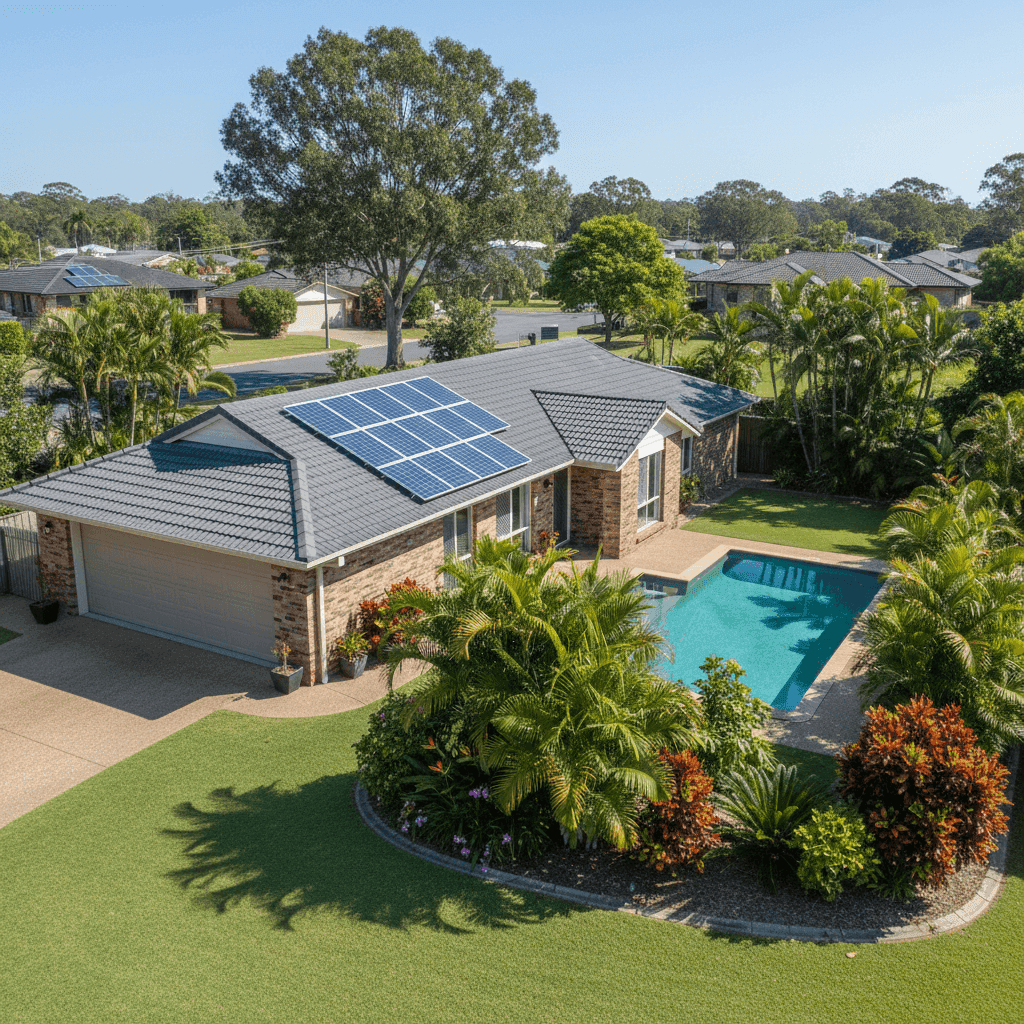

Brick Veneer Construction Brick veneer walls are generally viewed favourably by insurers. They offer solid resistance to fire and wind compared to lightweight cladding or weatherboard, and tend to hold up well in storm events — a key consideration on the Sunshine Coast.

Tiled Roof A tiled roof is another risk-positive feature. Tiles are durable, fire-resistant, and long-lasting when properly maintained. While they can be more expensive to repair after hail damage than metal roofing, they're broadly considered a lower-risk roofing material by most Australian insurers.

Concrete Slab Foundation A slab foundation offers good structural stability and reduces the risk of subsidence or pest-related damage that can affect older homes on stumps or piers. For a home built in 1989, a slab is a solid foundation — literally and figuratively.

Swimming Pool Pools add value to a property but also introduce liability considerations. Most home and contents policies include public liability cover, which is important when a pool is involved. Homeowners should confirm their policy's liability limits and ensure the pool complies with Queensland's strict pool fencing regulations.

Solar Panels Solar panels are increasingly common on Sunshine Coast homes, and most modern policies can cover them — though it's worth checking whether they're included under the building sum insured or require a separate endorsement. At $728,000 building cover, there should be adequate room to include the panels in the insured value.

No Cyclone Risk This is a significant premium driver across much of Queensland. Mountain Creek's classification as outside the cyclone risk zone removes a substantial loading that affects many coastal and northern Queensland properties.

Tiled Flooring Tiles throughout the home are a practical choice in Queensland's climate and are generally less susceptible to water damage than carpet or timber floors — a minor but positive factor for contents risk.

---

Tips for Homeowners in Mountain Creek

1. Review your building sum insured regularly Construction costs have risen sharply in recent years across Queensland. A sum insured of $728,000 for a 214 sqm brick veneer home is reasonable, but it's worth reassessing annually to ensure it reflects current rebuild costs — not just the market value of the land and home combined.

2. Check your pool liability cover Queensland has some of the strictest pool fencing laws in Australia. Beyond compliance, make sure your policy includes adequate public liability cover — typically at least $10 million — in case of an accident involving your pool.

3. Don't underestimate contents $50,000 in contents cover is on the modest side for a four-bedroom home. Take stock of your furniture, appliances, electronics, clothing, and valuables. Many homeowners find they're significantly underinsured when they actually tally up their possessions.

4. Compare quotes before renewing Even if your current premium is below average, insurers adjust their pricing models every year. What's cheap today may not be competitive at renewal. Use a comparison tool like CoverClub to benchmark your renewal quote against the market before you commit.

---

Ready to Compare Your Options?

Whether you're buying, renewing, or simply curious about what you should be paying, CoverClub makes it easy to compare home insurance quotes for properties across the Sunshine Coast and beyond. Get a quote today and see how your premium stacks up against your neighbours — you might be surprised by how much you could save.