Mountain Creek is a well-established residential suburb on Queensland's Sunshine Coast, known for its family-friendly streets, proximity to the coast, and a mix of modern and late-1990s housing stock. If you own a free standing home here, understanding what you should be paying for home and contents insurance — and why — can save you hundreds of dollars a year.

This article breaks down a real home insurance quote for a 3-bedroom, 2-bathroom brick veneer home in Mountain Creek (postcode 4557), compares it against local, state, and national benchmarks, and offers practical tips to help you get the best value cover.

---

Is This Quote Fair?

The quote in question is $2,620 per year (or $251/month) for combined home and contents insurance, covering a building sum insured of $677,000 and contents valued at $50,000, each with a $1,000 excess.

Our price rating for this quote is CHEAP — Below Average, which is genuinely good news for the homeowner. At $2,620 annually, this premium sits well below the suburb median of $4,760/yr, meaning more than half of comparable Mountain Creek properties are paying considerably more for similar cover.

To put it plainly: this is a competitive result. The homeowner is getting solid coverage — building and contents combined — at a price that undercuts most of their neighbours. That said, "cheap" doesn't always mean the right policy, so it's still worth checking what's included, particularly around storm and water damage events, which are relevant on the Sunshine Coast.

---

How Mountain Creek Compares

Understanding where this quote sits relative to broader benchmarks gives important context. Here's how the numbers stack up:

| Benchmark | Premium |

|---|---|

| This Quote | $2,620/yr |

| Mountain Creek Suburb Median | $4,760/yr |

| Mountain Creek Suburb Average | $41,962/yr |

| Mountain Creek 25th Percentile | $3,392/yr |

| Mountain Creek 75th Percentile | $8,820/yr |

| QLD State Median | $3,903/yr |

| QLD State Average | $9,129/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

| Sunshine Coast LGA Average | $7,249/yr |

A few things stand out here. First, the suburb average of $41,962/yr is dramatically higher than the median of $4,760/yr — a sign that a small number of very high-risk or high-value properties in Mountain Creek are pulling the average upward significantly. The median is always the more reliable figure for a typical homeowner.

This quote of $2,620/yr is even below the national median of $2,764/yr, which is remarkable given that Queensland properties — particularly on the Sunshine Coast — tend to attract higher premiums than the national norm due to weather-related risks. It also sits well below the QLD state median of $3,903/yr and the Sunshine Coast LGA average of $7,249/yr.

You can explore the full breakdown of insurance pricing trends for this postcode at the Mountain Creek suburb stats page, or compare against national averages to see how Queensland stacks up against the rest of Australia.

---

Property Features That Affect Your Premium

Several characteristics of this particular property work in the homeowner's favour when it comes to pricing:

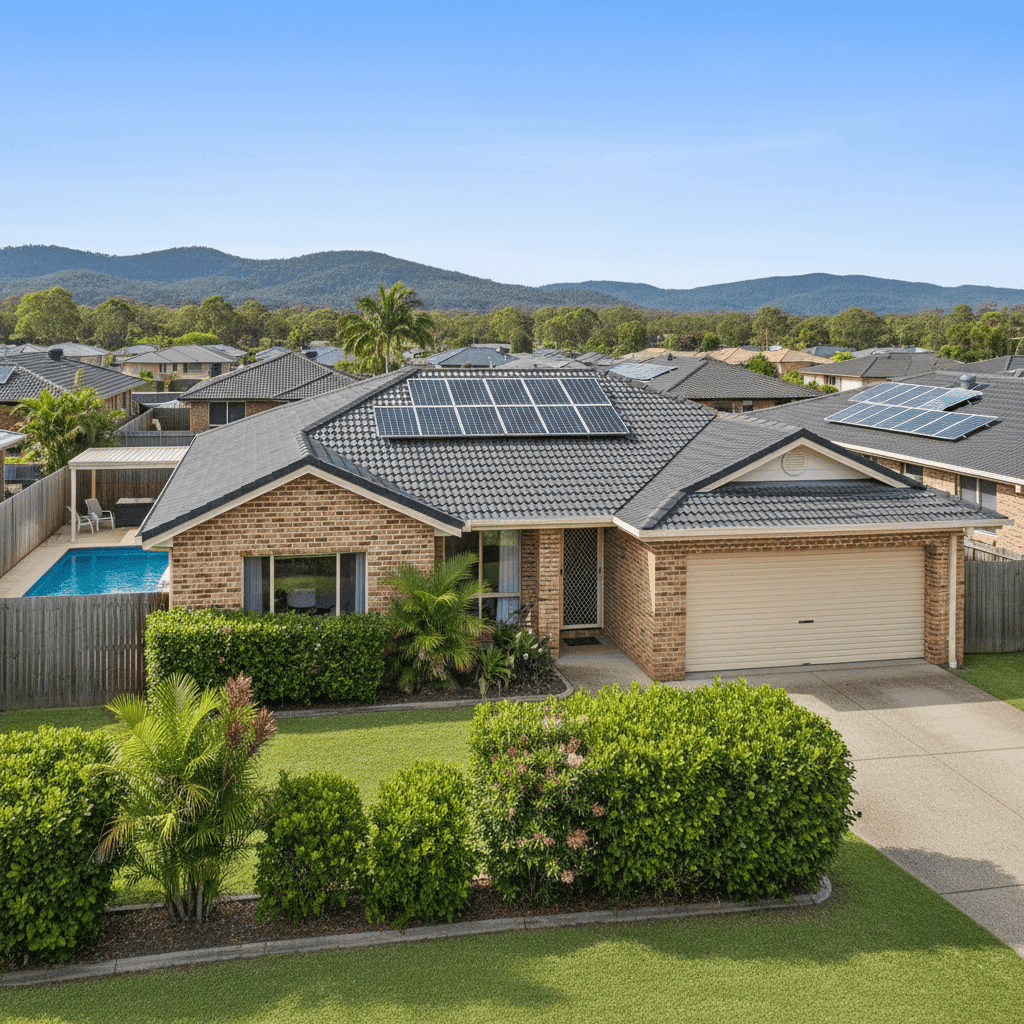

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is generally viewed favourably by insurers. Both materials offer good fire resistance and durability, and are less susceptible to wind damage than lightweight cladding or metal roofing in some configurations. This combination is a staple of late-1990s Queensland residential construction and is well understood by underwriters.

Slab Foundation A concrete slab foundation is standard for homes of this era and is considered low-risk by most insurers. It eliminates concerns around subfloor flooding or pest damage that can affect older homes on timber stumps.

Timber/Laminate Flooring While aesthetically popular, timber and laminate floors can be more susceptible to water damage than tiles. This is worth keeping in mind — ensure your policy has strong coverage for water ingress and internal flooding events.

Swimming Pool A pool adds both value and a degree of liability risk to a property. Some insurers factor this into their pricing; others include pool structures under the building sum insured. It's worth confirming your pool equipment, fencing, and surrounds are adequately covered under your building policy.

Solar Panels The property has solar panels installed, which are typically covered under the building sum insured — but not always automatically. Check that your insurer explicitly covers solar panel systems, including inverters and mounting hardware, and that the $677,000 building sum insured accounts for their replacement value.

Ducted Climate Control Ducted air conditioning is a fixed installation and should be included in the building sum insured. Given the Sunshine Coast climate, this is a significant asset — confirm it's listed or captured within your building coverage.

No Cyclone Risk Mountain Creek falls outside the designated cyclone risk zone, which is a meaningful factor in keeping premiums lower than properties further north in Queensland. Cyclone-rated cover adds considerable cost, so this is a genuine pricing advantage for Sunshine Coast homeowners compared to, say, Cairns or Townsville.

---

Tips for Homeowners in Mountain Creek

1. Review your building sum insured annually Construction costs have risen sharply in recent years across Queensland. A home built in 1999 at 214 sqm could cost significantly more to rebuild today than it did even three years ago. Make sure your $677,000 sum insured reflects current rebuild costs — not just the market value of the land and home combined. Underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panels and pool equipment are explicitly covered Don't assume these are automatically included. Ask your insurer directly whether solar panels (including the inverter) and pool equipment are covered under the building policy, and whether there are any sub-limits that apply.

3. Check storm and water damage inclusions Even outside the cyclone zone, the Sunshine Coast experiences significant rainfall and storm events. Review your policy's definitions around storm damage, rainwater run-off, and gradual water damage — these are common exclusions that catch homeowners off guard at claim time.

4. Compare quotes before renewing This quote is priced below average, but premiums shift each year. Insurers often increase renewals quietly, and loyalty doesn't always translate to the best deal. Set a reminder to compare quotes at CoverClub before your renewal date each year — even a 10–15 minute comparison could save you hundreds.

---

Get a Quote for Your Mountain Creek Home

Whether you're a first-time buyer or a long-term homeowner in Mountain Creek, it pays to know what the market looks like before accepting any renewal. CoverClub makes it easy to compare home and contents insurance quotes tailored to your specific property — so you can see exactly where your premium sits relative to your suburb, your state, and the national picture.

Get a quote for your Mountain Creek home today and find out if you're paying a fair price — or if there's a better deal waiting for you.