Mountain Creek is a well-established residential suburb on Queensland's Sunshine Coast, sitting just inland from Mooloolaba and a short drive from the beach. It's a popular choice for families, with tree-lined streets, good schools, and the kind of relaxed lifestyle that draws people to South East Queensland. For homeowners here, understanding what you should be paying for home insurance — and why — can make a real difference to your household budget.

This article takes a close look at a recent home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Mountain Creek, breaking down whether the price is fair, how it sits against local and national benchmarks, and what property features are likely influencing the premium.

---

Is This Quote Fair?

The quote in question comes in at $2,501 per year (or $244 per month) for combined home and contents cover, with a building sum insured of $663,000 and $50,000 in contents cover. Both the building and contents excess are set at $1,000.

Our pricing engine rates this quote as CHEAP — below average for the area. That's genuinely good news for the homeowner. To put it in perspective:

- The suburb median for Mountain Creek (QLD 4557) sits at $4,760/yr

- The suburb average is a much higher $41,962/yr — heavily skewed by outlier quotes

- The Queensland state median is $3,903/yr

- The national median across Australia is $2,764/yr

At $2,501/yr, this quote sits below the national median and well under the suburb median. For a property of this size and specification, that represents solid value. The relatively low premium likely reflects a combination of favourable property characteristics and the fact that Mountain Creek sits outside designated cyclone risk zones — a major cost driver in many other parts of Queensland.

---

How Mountain Creek Compares

Mountain Creek's insurance data tells an interesting story. With a suburb average of $41,962/yr based on 26 quotes, the mean is clearly being pulled upward by a small number of very high-premium properties. The median of $4,760/yr is a far more useful reference point for typical homeowners in the area.

Here's how the numbers stack up across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,501 |

| Suburb Median (Mountain Creek) | $4,760 |

| Suburb 25th Percentile | $3,392 |

| LGA Average (Sunshine Coast) | $7,249 |

| QLD State Median | $3,903 |

| National Median | $2,764 |

| National Average | $5,347 |

Remarkably, this quote even comes in below the suburb's 25th percentile of $3,392/yr — meaning it's cheaper than at least 75% of quotes sampled in the postcode. You can explore broader Queensland insurance pricing trends and national home insurance data to see how your own situation compares.

The Sunshine Coast LGA average of $7,249/yr highlights how much variability exists across the region. Coastal and flood-prone pockets can attract significantly higher premiums, which drags up LGA-wide figures even when inland suburbs like Mountain Creek fare much better.

---

Property Features That Affect Your Premium

Several characteristics of this property work in the homeowner's favour when it comes to pricing:

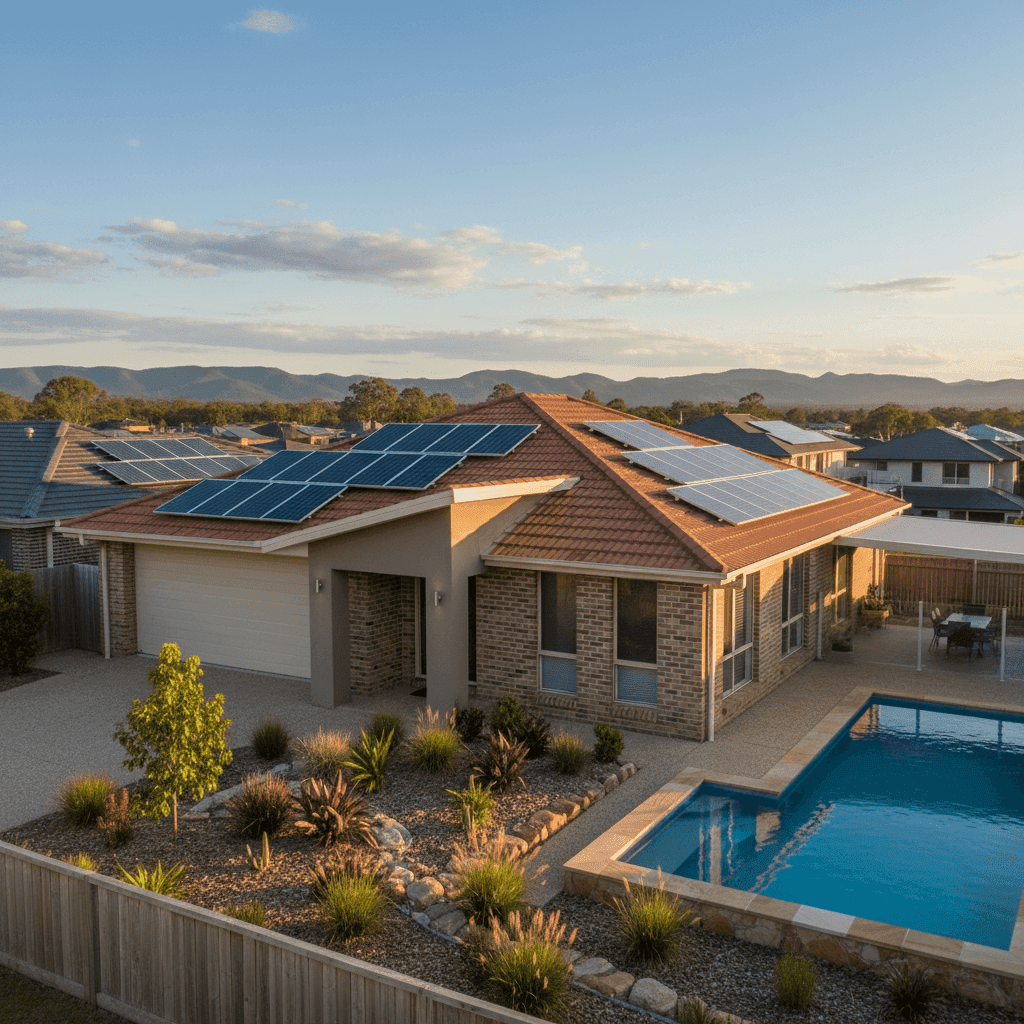

Brick Veneer Construction Brick veneer walls are generally viewed favourably by insurers. They offer solid resistance to everyday weather events and are considered lower risk than timber-framed cladding or weatherboard exteriors. This tends to translate into more competitive premiums.

Tiled Roof Concrete or terracotta tile roofs are durable and widely accepted by insurers as a standard, lower-risk roofing material. They perform well in storms and have a long service life, both of which reduce the likelihood of a claim.

Slab Foundation A concrete slab foundation is one of the most common and insurer-friendly foundation types in Queensland. It carries minimal risk of subsidence or movement compared to older stumped or pier-and-beam foundations.

No Cyclone Risk Mountain Creek falls outside Queensland's designated cyclone risk zones, which is a significant premium advantage. Properties in North Queensland or coastal Far North QLD can pay dramatically more due to cyclone loading in their premiums.

Swimming Pool The presence of a pool adds some liability exposure and replacement cost to the policy, which can nudge premiums upward slightly. Pools also require safety compliance under Queensland law, so ensuring yours meets current fence and gate standards is important both for safety and insurability.

Solar Panels Solar panels are now a standard inclusion on many Australian homes, but they do add to the replacement cost of a building. Most insurers cover panels as part of the building sum insured, so it's worth confirming your $663,000 building cover adequately accounts for the panels' reinstallation value.

Timber and Laminate Flooring Timber and laminate floors can be more susceptible to water damage than tiles, which may be a minor factor in contents or internal finishes claims. Ensuring your sum insured reflects the cost of replacing these floors is worthwhile.

1999 Construction At around 25 years old, the home is relatively modern and built to standards that predate but are reasonably close to current building codes. This is generally seen as a neutral-to-positive factor by underwriters.

---

Tips for Homeowners in Mountain Creek

1. Don't underinsure your building With construction costs rising sharply in recent years, a sum insured set even a few years ago may no longer reflect today's rebuild cost. At 214 sqm, this home's $663,000 building cover works out to roughly $3,098/sqm — reasonable for a brick veneer build with a pool and solar, but worth reviewing annually as labour and materials costs shift.

2. Confirm your solar panels are covered Check your policy wording to ensure solar panels are explicitly included in your building cover and that the sum insured accounts for their full replacement value, including inverters and installation labour.

3. Keep your pool compliant Queensland has strict pool safety laws. A non-compliant pool fence or gate can create issues at claim time. Staying up to date with inspections and certifications isn't just a legal obligation — it protects your coverage.

4. Compare quotes at renewal Even if you're already on a competitive premium, the insurance market changes every year. Insurers reprice based on claims data, reinsurance costs, and weather events. Running a fresh comparison at renewal — even when you're happy with your current insurer — is one of the simplest ways to stay on the right side of the market.

---

Ready to See What You Could Pay?

Whether you're a Mountain Creek local or shopping for cover elsewhere on the Sunshine Coast, CoverClub makes it easy to compare home and contents insurance quotes in minutes. Our tools draw on real pricing data so you can see exactly how your quote stacks up — not just against a single insurer, but against the broader market.

Get a home insurance quote at CoverClub and find out if you're paying a fair price for your home.