Mudgeeraba is a leafy, family-friendly suburb nestled in the Gold Coast hinterland, offering a relaxed lifestyle just a short drive from the coast. It's also a suburb where property values — and therefore insurance costs — carry some real weight. This article takes a close look at a home and contents insurance quote for a four-bedroom, two-bathroom free standing home in Mudgeeraba (postcode 4213), breaking down whether the premium stacks up against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $3,703 per year (or around $362 per month), covering a building sum insured of $801,000 and contents valued at $179,000, each with a $1,000 excess. Our price rating for this quote is FAIR — Around Average.

That rating reflects a premium that sits comfortably within the middle range of what Mudgeeraba homeowners are paying. It's not the cheapest quote you'll find in the suburb, but it's far from the top end either. Given the property's size (235 sqm), its construction materials, and the added complexity of features like a pool and solar panels, a premium in this range is broadly reasonable.

For homeowners wondering whether to accept a quote at this level or shop around, the "fair" rating suggests there's likely some room to find a better deal — but you're not being dramatically overcharged.

---

How Mudgeeraba Compares

Understanding where your premium sits relative to others is key to making an informed decision. Here's how this quote measures up:

| Benchmark | Premium |

|---|---|

| This Quote | $3,703/yr |

| Mudgeeraba Suburb Average | $3,275/yr |

| Mudgeeraba Suburb Median | $3,175/yr |

| Mudgeeraba 25th Percentile | $2,498/yr |

| Mudgeeraba 75th Percentile | $3,719/yr |

| Gold Coast LGA Average | $8,161/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

(Based on 64 quotes collected for the Mudgeeraba area. View full [Mudgeeraba suburb insurance stats](https://coverclub.com.au/stats/QLD/4213/mudgeeraba).)

A few things stand out here. First, this quote is above the suburb average and median — sitting roughly $428/yr above the average and $528/yr above the median for the area. That said, it falls just under the 75th percentile of $3,719/yr, meaning around three-quarters of Mudgeeraba quotes are at or below this level.

Second, the Gold Coast LGA average of $8,161/yr and the QLD state average of $9,129/yr look dramatically higher — but these figures are heavily influenced by coastal and high-risk properties across the region (think beachfront homes, flood-prone areas, and cyclone-exposed zones). Mudgeeraba, being inland and not in a designated cyclone risk area, generally attracts more moderate premiums.

Nationally, the picture is similarly skewed. The national average of $5,347/yr is pulled up by high-risk regions, while the national median of $2,764/yr is lower than this quote — reflecting how many Australian homeowners in lower-risk areas pay less. For QLD-wide context, the state median of $3,903/yr is actually slightly above this quote, which is a reassuring sign.

---

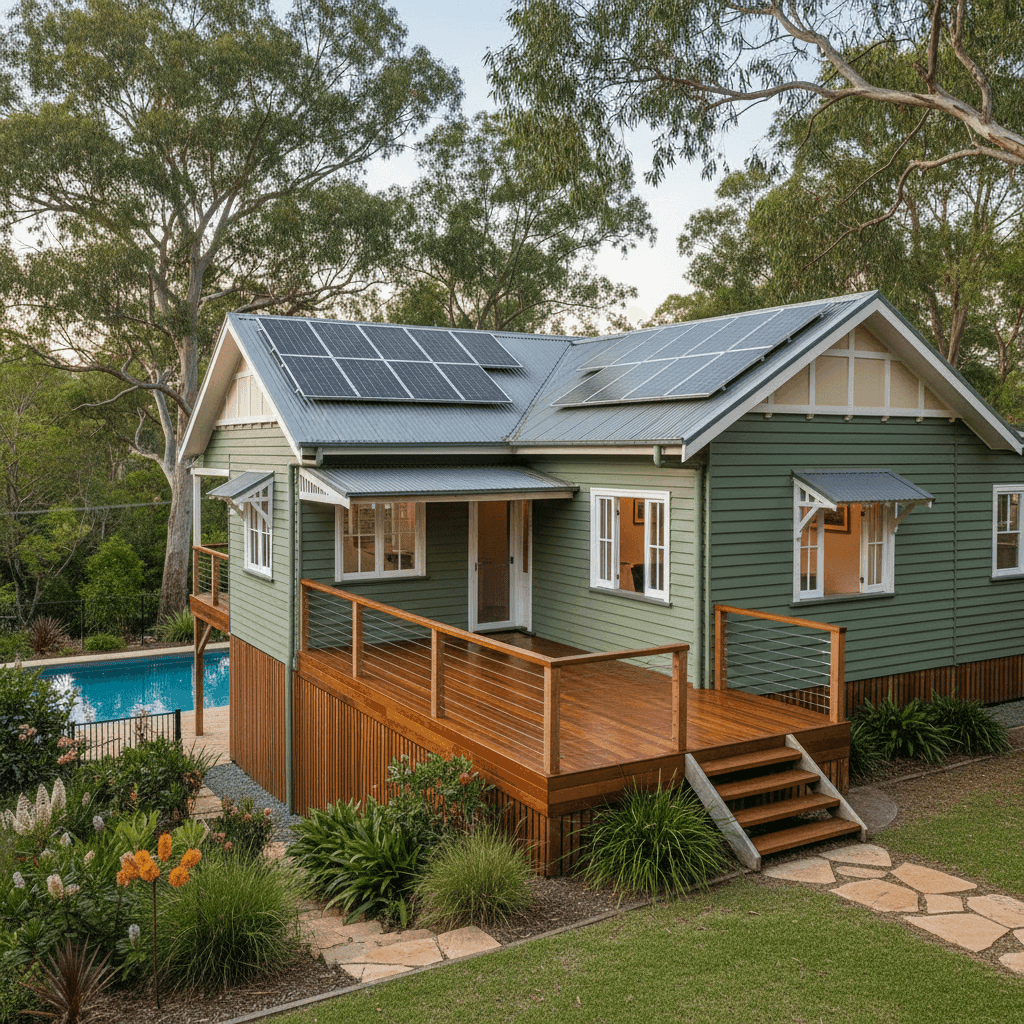

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on what insurers charge. Here's a breakdown of the key factors at play:

Weatherboard Timber Walls

Weatherboard wood is a classic Australian construction style, but it does carry a higher fire risk than brick or rendered masonry. Insurers typically price timber-framed and timber-clad homes at a slight premium to reflect the elevated risk of fire spread and the cost of repairs or replacement.

Steel / Colorbond Roof

On the positive side, a Colorbond steel roof is generally viewed favourably by insurers. It's durable, resistant to ember attack, and performs well in storms — all factors that can help moderate your premium compared to older or more vulnerable roofing materials.

Stump Foundation

A home on stumps (also known as a raised or pier foundation) can be more susceptible to movement, particularly in areas with reactive soils or moisture variation. It also increases the risk profile for certain events like storm surge or flooding, though Mudgeeraba's inland location mitigates some of this concern.

Timber / Laminate Flooring

Timber and laminate floors are considered a moderate-cost finish. They're not as expensive to replace as polished hardwood or high-end tiles, but they do add to the overall contents and fixtures valuation.

Swimming Pool

A pool adds both value and liability to a property. Insurers factor in the cost of pool fencing compliance, equipment replacement (pumps, filters, heating), and the liability risk associated with pool ownership. Expect the pool to contribute meaningfully to your overall premium.

Solar Panels

Solar panels are an increasingly common feature in Queensland, but they do add to the replacement cost of a home. A quality solar system can cost $8,000–$20,000+ to replace, and insurers will factor this into the building sum insured and premium calculation.

No Cyclone Risk

Being outside a designated cyclone risk area is a notable advantage for Mudgeeraba homeowners. Cyclone-prone areas in QLD can attract significantly higher premiums due to the catastrophic damage potential. This property avoids that loading entirely.

---

Tips for Homeowners in Mudgeeraba

If you're looking to get better value on your home and contents insurance, here are four practical steps worth considering:

- Review your building sum insured regularly. With construction costs rising sharply across Australia, it's easy to find yourself underinsured. Make sure your $801,000 building sum reflects current rebuild costs — not the purchase price or market value of the home.

- Bundle your home and contents cover. Most insurers offer a discount when you combine building and contents insurance under a single policy. If you're currently holding them separately, consolidating could save you a meaningful amount each year.

- Increase your excess to reduce your premium. If you have a solid emergency fund and are unlikely to make small claims, opting for a higher excess (say, $2,000 instead of $1,000) can noticeably reduce your annual premium. Just make sure the saving is worth the extra out-of-pocket risk.

- Compare quotes annually. Loyalty doesn't always pay in the insurance world. Insurers frequently offer better rates to new customers, so it's worth shopping around at renewal time. Even a "fair" quote can often be beaten with a bit of research.

---

Compare Your Options with CoverClub

Whether you're reviewing an existing policy or shopping for cover on a new property, getting multiple quotes is the single best way to ensure you're not overpaying. At CoverClub, we make it easy to compare home and contents insurance options tailored to your property and location. Get a quote today and see how much you could save.