Mudgeeraba is one of the Gold Coast hinterland's most sought-after pockets — a leafy, semi-rural suburb that blends lifestyle appeal with suburban convenience. For owners of a free standing home in this part of Queensland, understanding what drives home insurance costs is just as important as knowing what the policy actually covers. This article breaks down a real home and contents insurance quote for a five-bedroom property in Mudgeeraba (postcode 4213), benchmarks it against local, state, and national figures, and offers practical advice for getting the best value on your cover.

---

Is This Quote Fair?

The annual premium on this quote comes in at $3,653 per year (or $350 per month), with a building sum insured of $1,121,000 and $50,000 in contents cover. Both the building and contents excess are set at $1,000.

CoverClub's pricing engine rates this quote as Fair — Around Average, and the numbers back that up. At $3,653, the premium sits comfortably within the middle band of what Mudgeeraba homeowners are currently paying. It's above the suburb's 25th percentile ($2,498/yr) but well below the 75th percentile ($3,719/yr), placing it squarely in the middle of the local market.

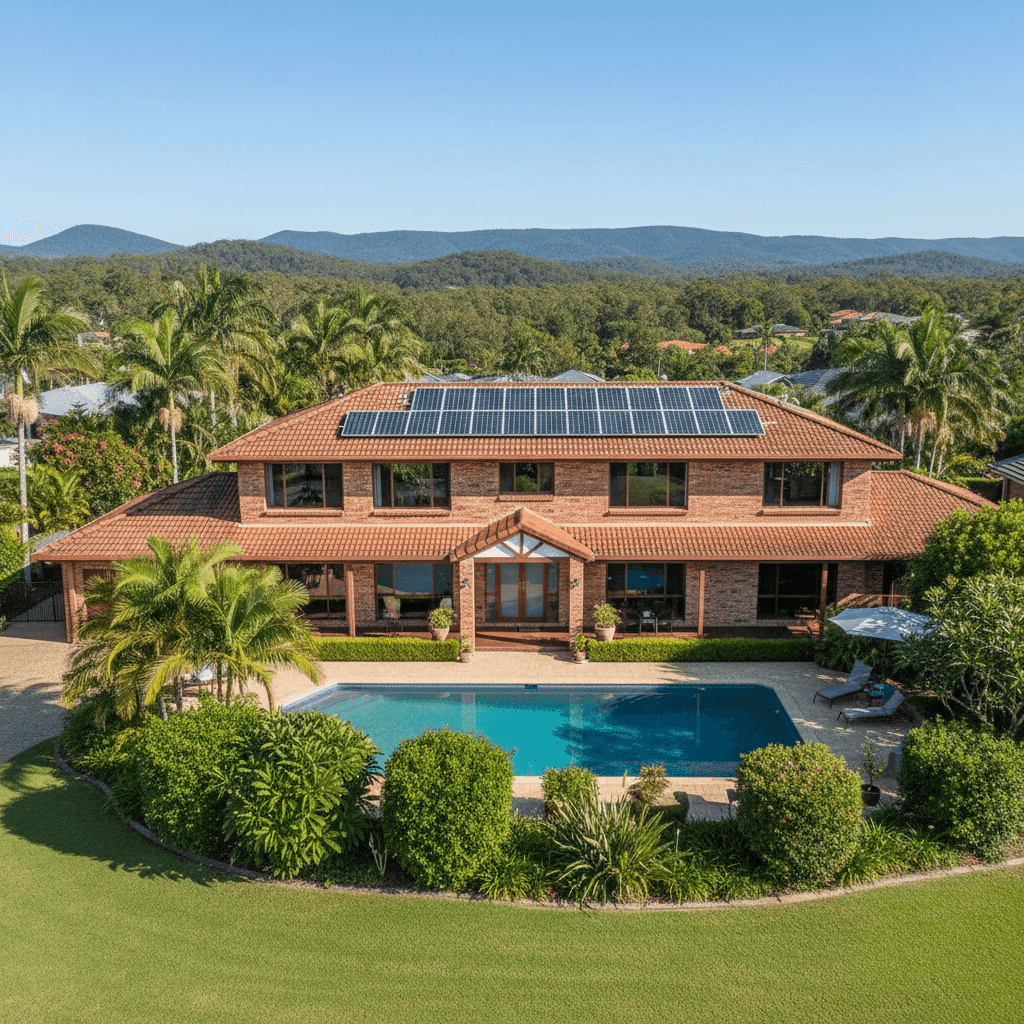

For a 325 sqm double brick home with a pool, solar panels, and ducted climate control, a "fair" rating is actually a reasonable outcome. Larger, well-appointed properties naturally attract higher premiums, and this quote reflects the added replacement cost complexity that comes with those features — without tipping into overpriced territory.

---

How Mudgeeraba Compares

To put this quote in proper context, it helps to look at the broader pricing landscape across suburb, state, and national benchmarks.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Mudgeeraba (4213) | $3,275/yr | $3,175/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

A few things stand out here. First, the Queensland state average of $9,129 per year looks alarming at first glance — but it's heavily skewed by high-risk coastal and cyclone-prone areas in Far North Queensland, where premiums can be eye-watering. The state median of $3,903 is a far more representative figure for southeast Queensland suburbs like Mudgeeraba.

Second, the national average of $5,347 is similarly distorted by extreme-risk postcodes. The national median of $2,764 is closer to reality for most Australian homeowners, though it reflects a wide mix of property types, sizes, and risk profiles.

Within the Gold Coast LGA, the average premium sits at $8,161 per year — again, pulled upward by beachfront and flood-prone properties closer to the coast. Mudgeeraba's own suburb average of $3,275 tells a more accurate story: this is a relatively affordable area to insure compared to many Gold Coast postcodes.

At $3,653, this quote is $378 above the suburb average — a modest premium that's largely explained by the property's size and additional features rather than any elevated risk profile.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful impact on what insurers charge.

Double Brick Construction Double brick walls are generally viewed favourably by insurers. They offer strong resistance to fire, wind, and impact damage, and tend to hold up well over time. This construction type can help moderate premiums compared to timber or lightweight cladding alternatives.

Tiled Roof Terracotta or concrete tile roofing is considered a durable, low-risk choice in southeast Queensland. Unlike metal roofing, tiles perform well in hail events and are not prone to the corrosion issues sometimes seen in coastal environments. This is a positive factor for insurers.

Slab Foundation A concrete slab foundation is a standard and well-regarded construction method in Queensland's climate. It reduces the risk of subfloor moisture issues and is generally straightforward to assess for insurers.

Swimming Pool Pools add to the overall replacement cost of a property, which is reflected in the building sum insured. Insurers also factor in liability considerations. Ensuring your sum insured adequately accounts for the pool's reinstatement value is essential.

Solar Panels A 2011-era home with solar panels is a common combination in southeast Queensland. Solar systems add to the building replacement cost and can be damaged in severe weather events. It's worth confirming with your insurer that panels are explicitly included in your building cover and that the sum insured reflects their current replacement value.

Ducted Climate Control Ducted air conditioning systems are a significant fixed asset within the home. Like solar panels, they contribute to the overall building replacement cost and should be factored into your sum insured calculation.

No Cyclone Risk Mudgeeraba is not classified as a cyclone risk area, which is a notable advantage. Cyclone loading is one of the single largest premium drivers in Queensland, so properties outside designated risk zones benefit from significantly lower base rates.

---

Tips for Homeowners in Mudgeeraba

1. Review Your Building Sum Insured Regularly At $1,121,000, the building sum insured on this quote is substantial — and rightly so for a 325 sqm property with quality inclusions. However, construction costs have risen sharply in recent years. Make sure your sum insured is recalculated annually using a current building cost estimator, rather than relying on automatic indexation alone. Underinsurance is one of the most common and costly mistakes Australian homeowners make.

2. Don't Overlook Contents Cover $50,000 in contents cover is on the modest side for a five-bedroom home. Take the time to complete a proper home contents inventory — including furniture, appliances, electronics, clothing, and outdoor items like patio furniture and garden equipment. Many homeowners are surprised to find their contents are worth significantly more than their initial estimate.

3. Ask About Bundling Discounts Many insurers offer discounts when you combine building and contents cover under a single policy (as this quote does) or when you hold multiple policies with the same provider. It's worth asking your insurer directly what discounts apply to your situation.

4. Compare Quotes Before Renewing The home insurance market is competitive, and loyalty doesn't always pay. Insurers often offer sharper pricing to new customers than to existing ones. Before accepting your renewal quote each year, take 10 minutes to compare quotes on CoverClub to make sure you're not paying more than you need to. Even a "fair" quote can sometimes be beaten with the right comparison.

---

Ready to Compare?

Whether you're reviewing your current policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up. Check Mudgeeraba suburb stats or get a personalised quote in minutes — no jargon, no pressure, just clear pricing from a range of Australian insurers.