Mudgeeraba is a well-established suburb nestled in the Gold Coast hinterland, offering residents a relaxed lifestyle with easy access to both coastal amenities and lush green surrounds. It's also a suburb where home insurance costs can vary considerably — making it well worth understanding exactly what you're paying and why. This article breaks down a real home and contents insurance quote for a four-bedroom, free-standing home in Mudgeeraba (postcode 4213), and puts the numbers into context using suburb, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $2,333 per year (or $224 per month), covering both building and contents for a property with a building sum insured of $621,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Our price rating for this quote is CHEAP — below the suburb average — and the data backs that up clearly. Based on 64 quotes collected for Mudgeeraba, the suburb average sits at $3,275 per year and the median at $3,175 per year. This quote falls well below both figures, and it also sits beneath the suburb's 25th percentile of $2,498 per year — meaning it's cheaper than at least three-quarters of comparable quotes in the area.

For homeowners, this is an encouraging result. It suggests the combination of property characteristics, insurer pricing, and coverage structure has produced a genuinely competitive outcome. That said, cheapest doesn't always mean best — it's important to ensure the policy terms, exclusions, and coverage limits actually suit your needs.

---

How Mudgeeraba Compares

To put this quote in broader perspective, it helps to look beyond the suburb level.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,333 |

| Mudgeeraba Suburb Average | $3,275 |

| Mudgeeraba Suburb Median | $3,175 |

| Mudgeeraba 25th Percentile | $2,498 |

| Gold Coast LGA Average | $8,161 |

| QLD State Average | $9,129 |

| QLD State Median | $3,903 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. First, the Queensland state average of $9,129 per year is extraordinarily high — a figure heavily skewed by cyclone-prone and flood-affected regions in Far North Queensland and other high-risk areas. The state median of $3,903 is a more representative figure for most QLD homeowners, and even against that benchmark, this Mudgeeraba quote performs strongly.

The Gold Coast LGA average of $8,161 may seem surprising at first glance, but it reflects the wide diversity of properties across the region — from beachfront homes with storm and flood exposure, to elevated hinterland properties like those in Mudgeeraba. This particular suburb tends to fare better on risk assessments than many coastal Gold Coast locations.

Compared to national figures, the quote also holds up well. The national average of $5,347 is more than double this premium, and even the national median of $2,764 is slightly higher. All told, this is a strong result by almost any measure.

---

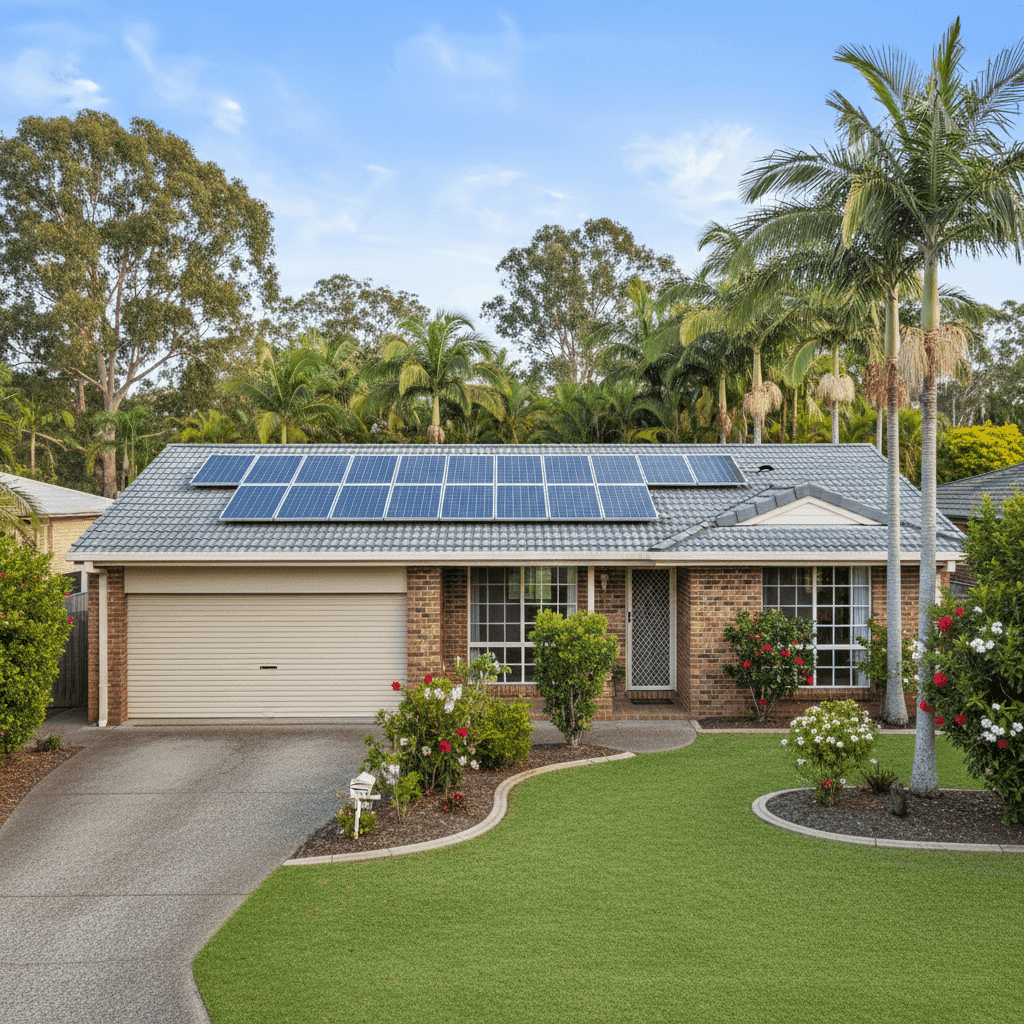

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its competitive premium.

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and structural durability compared to timber-framed or weatherboard homes, which can translate into lower building premiums.

Tiled roof is another positive factor. Tiles are durable, long-lasting, and perform well in most weather conditions. They're considered lower risk than older corrugated iron or fibrous cement roofing materials.

Slab foundation is the most common foundation type for homes built in Queensland from the 1980s onwards, and it's generally straightforward for insurers to assess. There are no elevated subfloor spaces that might be vulnerable to flooding or pest damage.

Construction year of 1995 places the home in a period when building codes were reasonably robust. It's old enough to have some character but new enough to avoid many of the structural concerns associated with pre-1970s construction.

Solar panels are worth noting. While they add value to the home, they can slightly increase the sum insured required to cover the full replacement cost of the building. It's worth confirming with your insurer that your solar system is explicitly covered under the building policy.

Ducted climate control is a significant fixed asset and should be factored into your building sum insured. At $621,000, the building cover here appears well-calibrated for a 214 sqm home of this specification in the current construction cost environment.

Vinyl flooring throughout is a practical, cost-effective choice and generally doesn't significantly affect premiums one way or another — though it's worth noting that contents cover would typically not extend to fixed flooring, which falls under the building policy.

One thing notably absent from this property's risk profile: no cyclone risk area designation. Mudgeeraba sits far enough inland that it avoids the cyclone loading applied to many coastal and northern Queensland properties — a meaningful saving for homeowners in this area.

---

Tips for Homeowners in Mudgeeraba

1. Review your building sum insured regularly. Construction costs in South East Queensland have risen sharply in recent years. A sum insured that was accurate two or three years ago may no longer reflect the full cost of rebuilding your home. Use a building cost calculator or speak with a quantity surveyor to ensure you're not underinsured.

2. Confirm your solar panels are covered. Not all policies automatically include solar panel systems in building cover. Check your Product Disclosure Statement (PDS) to confirm your panels — and any associated inverter or battery storage — are explicitly listed and covered for accidental damage, storm, and theft.

3. Don't overlook contents coverage. A contents value of $50,000 is relatively modest for a four-bedroom home. Take stock of your furniture, appliances, electronics, clothing, and valuables. Many homeowners underestimate their contents and find themselves out of pocket after a claim. A home contents calculator can help you arrive at a more accurate figure.

4. Compare quotes at renewal — every year. Even if you're happy with your current insurer, the home insurance market is competitive and pricing changes frequently. Comparing quotes annually takes only a few minutes and could save you hundreds of dollars. Get a fresh quote at CoverClub to see what's available for your property right now.

---

See How Your Home Compares

Whether you're a first-time buyer or a long-term Mudgeeraba resident, understanding the insurance landscape in your suburb is a smart first step to making sure you're getting value for money. You can explore detailed pricing data for Mudgeeraba and postcode 4213 on CoverClub, or browse Queensland-wide statistics to see how your area stacks up.

Ready to find out what you could be paying? Compare home and contents insurance quotes at CoverClub — it's free, fast, and built specifically for Australian homeowners.