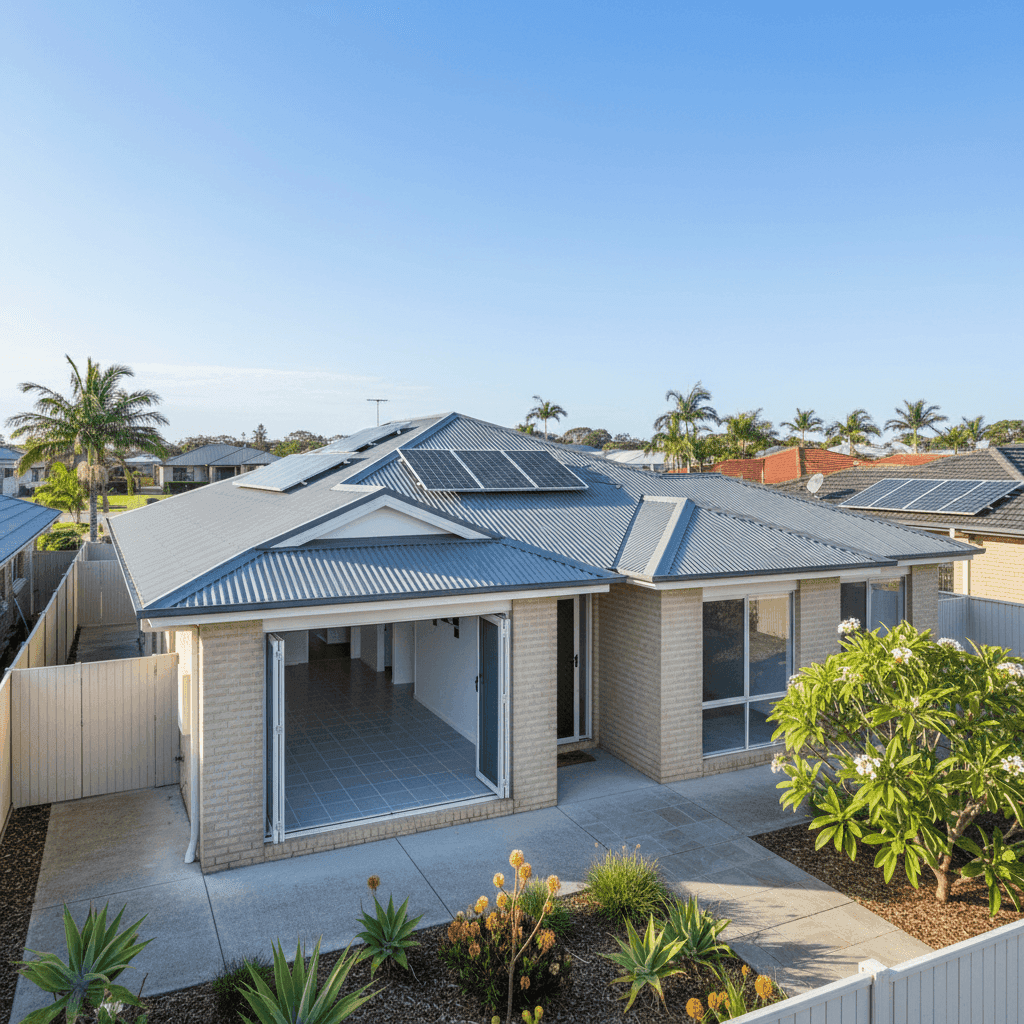

Mulambin is a coastal suburb in the Livingstone local government area on Queensland's Capricorn Coast — a beautiful part of the world, but one that comes with some serious insurance considerations. This analysis looks at a home and contents insurance quote for a three-bedroom, two-bathroom free standing home in Mulambin (postcode 4703), breaking down whether the premium is competitive and what's driving the cost.

---

Is This Quote Fair?

The quoted annual premium for this property is $4,332 per year (or $408 per month), covering both building (sum insured: $615,000) and contents ($50,000 in value). Based on our pricing data, this quote is rated Expensive — above average for the area.

To put that in perspective: the suburb average premium for Mulambin sits at $2,854 per year, and the median is even lower at $2,421. That means this quote is running roughly 52% above the suburb average and nearly 79% above the suburb median. Even accounting for the higher building sum insured and the specific risk profile of this property, that's a meaningful gap worth investigating.

That said, it's important to read this in context. The sample size for Mulambin is relatively small (eight quotes), so suburb-level averages can shift significantly with just a few outliers. The 75th percentile for the suburb is $2,628 — meaning this quote sits well above even the most expensive quarter of comparable properties in the area. That's a strong signal that shopping around could yield real savings.

---

How Mulambin Compares

Understanding where Mulambin sits in the broader insurance landscape helps put this quote in perspective.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Mulambin (4703) | $2,854/yr | $2,421/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Livingstone LGA | $13,146/yr | — |

A few things stand out here. Queensland's average premium of $9,129 is dramatically higher than the national average of $5,347 — a reflection of the state's elevated exposure to cyclones, flooding, and severe weather events. However, the median figures tell a more nuanced story: Queensland's median of $3,903 is closer to the national median of $2,764, suggesting that a smaller number of very high-risk properties are pulling the state average upward.

The Livingstone LGA average of $13,146 is particularly striking — one of the highest we see across Queensland. This is largely driven by the cyclone risk classification that applies to much of the Capricorn Coast, which significantly inflates premiums for properties in this region.

Compared to the LGA average, this quote of $4,332 actually looks relatively modest. But compared to the suburb and national medians, there's still room to find a better deal.

You can explore the full data for Mulambin on CoverClub's suburb stats page, or browse Queensland-wide insurance statistics and national benchmarks for broader context.

---

Property Features That Affect Your Premium

Several characteristics of this property directly influence how insurers assess risk and calculate premiums.

Cyclone Risk Area This is arguably the single biggest factor. Mulambin falls within a designated cyclone risk zone, which triggers significant premium loadings with most insurers. Policies in these areas typically include specific cyclone excess clauses and stricter eligibility criteria. Not all insurers price cyclone risk the same way, which is one reason why quotes can vary enormously for the same property.

Brick Veneer Walls & Colorbond Roof Brick veneer is generally viewed favourably by insurers — it's durable, fire-resistant, and holds up well in high-wind events. The steel Colorbond roof is similarly well-regarded for its resilience, particularly in coastal and cyclone-prone environments. These construction materials can work in your favour when it comes to premium pricing.

Slab Foundation A concrete slab foundation is considered low-risk by most insurers. It reduces exposure to subsidence and pest-related structural issues, and it's the most common foundation type for modern builds in Queensland.

Built in 2013 At just over a decade old, this home is relatively new. Newer properties tend to attract lower premiums than older homes, as they're built to more recent cyclone and building code standards — a meaningful advantage in a high-wind-risk area like the Capricorn Coast.

Solar Panels Solar panels are an increasingly common feature, but they do add to the replacement cost of a home. Insurers factor in the cost of reinstating panels after a storm or hail event, so it's worth confirming your building sum insured accounts for this.

Ducted Climate Control Ducted air conditioning systems are another item that contributes to building replacement costs. These systems can be expensive to repair or replace, particularly after cyclone or storm damage.

Building Sum Insured: $615,000 The building sum insured of $615,000 for a 139 sqm home works out to roughly $4,424 per square metre — on the higher end of the scale. It's worth reviewing whether this figure accurately reflects current construction costs in the area. Underinsurance is a serious risk, but overinsurance can unnecessarily inflate your premium. Consider getting a building valuation to confirm the right figure.

---

Tips for Homeowners in Mulambin

1. Compare multiple quotes — especially in cyclone zones Insurers price cyclone risk very differently, and the spread between the cheapest and most expensive quote for the same property can be thousands of dollars. Don't accept a renewal without running a fresh comparison. Get a quote through CoverClub to see how your current premium stacks up.

2. Review your building sum insured annually Construction costs in Queensland have risen significantly in recent years. If your sum insured hasn't kept pace, you could be underinsured — meaning you'd receive less than you need to fully rebuild after a major event. Equally, if your sum insured is too high, you're paying more than necessary. An independent building valuation every few years is money well spent.

3. Ask about cyclone-specific excess clauses Many policies in cyclone-risk areas apply a separate, higher excess for cyclone-related claims. This can sometimes be $2,500 or more, on top of your standard excess. Make sure you understand exactly what you're covered for — and what you'd be out of pocket — before committing to a policy.

4. Consider your contents cover carefully The $50,000 contents value included in this quote is a reasonable starting point, but it's easy to underestimate what you own. Do a room-by-room audit of your belongings — furniture, electronics, clothing, appliances, and valuables — to make sure your cover reflects reality. Underinsured contents can leave you significantly out of pocket after a theft or storm event.

---

Ready to Find a Better Deal?

Whether you're renewing your existing policy or shopping around for the first time, comparing quotes is the most effective way to make sure you're not overpaying. CoverClub makes it easy to see how your premium compares to others in your suburb, your local government area, and across Queensland.

Start comparing home insurance quotes at CoverClub — it takes just a few minutes and could save you hundreds of dollars a year.