Murarrie is a well-established inner-east Brisbane suburb sitting just a few kilometres from the CBD, popular with families thanks to its leafy streets and proximity to the Gateway Motorway and Moreton Bay. For owners of a free-standing home in this area, understanding what drives your home insurance premium — and whether the figure on your renewal notice is actually competitive — can make a real difference to your household budget.

This article breaks down a recent home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Murarrie (postcode 4172), compares it against suburb, state and national benchmarks, and offers practical guidance for getting better value on your cover.

---

Is This Quote Fair?

The quote in question comes in at $4,035 per year (or $387 per month) for combined home and contents cover, with a building sum insured of $734,000 and contents valued at $50,000. Both the building and contents excess are set at $1,000.

Based on our pricing data, this quote is rated Expensive — Above Average for the Murarrie area. That doesn't necessarily mean you're being ripped off, but it does mean it's worth understanding why the premium sits where it does, and whether there's room to bring it down.

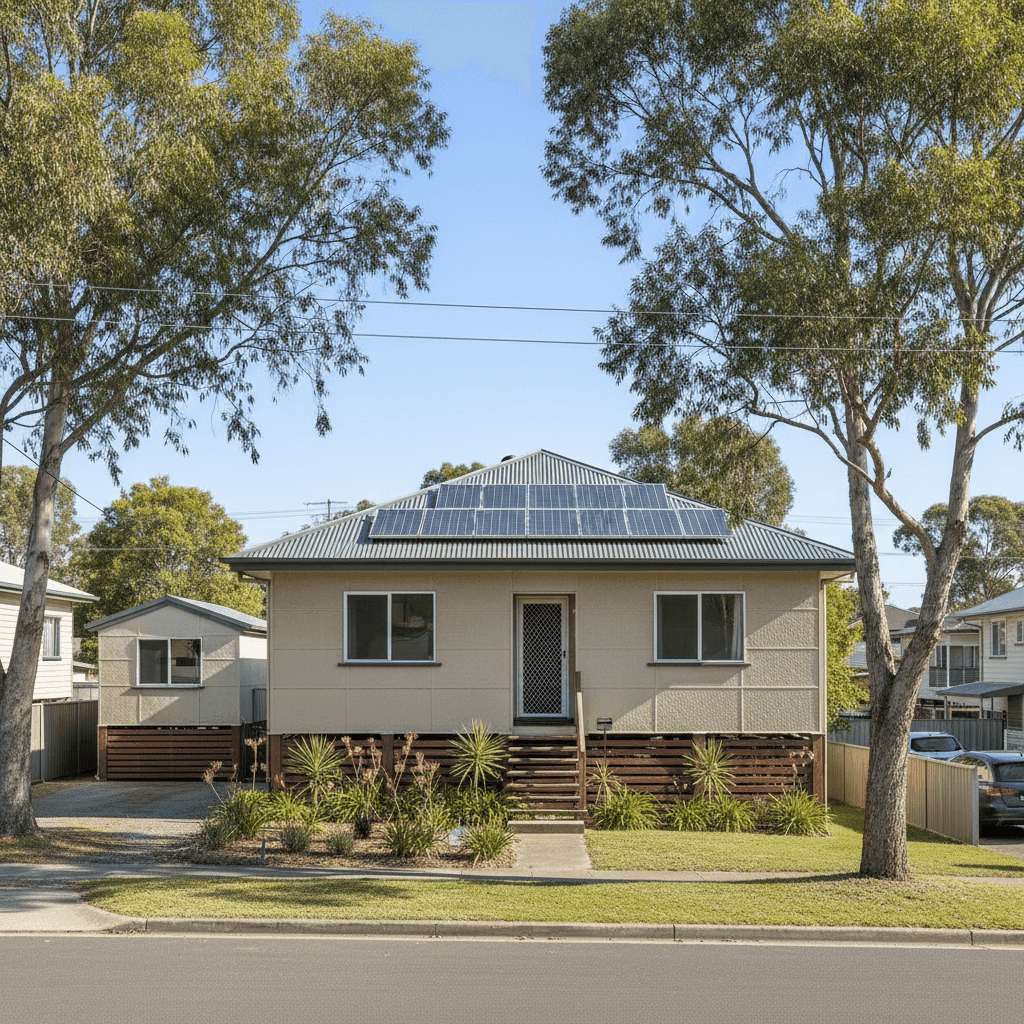

Several factors can legitimately push a premium above the suburb average: the size of the dwelling (214 sqm is a solid footprint), the building sum insured ($734,000 is substantial), the presence of a granny flat, ducted climate control, and solar panels all add to the replacement cost equation. Older construction materials — in this case, fibro asbestos external walls — also attract attention from underwriters due to the complexity and cost of repairs or rebuilds.

That said, a premium sitting meaningfully above the suburb average is always worth scrutinising. Comparing quotes in Murarrie is a straightforward way to see whether another insurer would price this risk more competitively.

---

How Murarrie Compares

Here's how this quote stacks up against the broader market:

| Benchmark | Premium |

|---|---|

| This quote | $4,035/yr |

| Murarrie suburb average | $2,308/yr |

| Murarrie suburb median | $1,904/yr |

| Murarrie 75th percentile | $3,267/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Brisbane LGA average | $16,277/yr |

A few things stand out here. While this quote is above the Murarrie suburb average and median, it's actually below both the Queensland state average and the national average — and dramatically below the Brisbane LGA average of $16,277. That last figure is heavily skewed by flood-prone and high-risk properties across the broader Brisbane council area, so it's not the most useful comparison point for Murarrie specifically.

The more telling comparison is against the suburb's 75th percentile of $3,267. This quote exceeds even that upper threshold, which suggests it's on the pricier end even among more complex properties in the area. Homeowners in a similar situation should be actively shopping around.

You can explore Queensland-wide insurance pricing data or national home insurance benchmarks to get a fuller picture of where your premium sits in the broader market.

---

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on the premium:

Fibro Asbestos External Walls

This is one of the most significant rating factors for older Queensland homes. Fibro asbestos (fibrous cement sheeting containing asbestos, common in homes built before the mid-1980s) requires specialist handling during any repair or rebuild. Insurers factor in the additional cost of safe removal, disposal and replacement with compliant modern materials — all of which inflates the premium compared to a brick or weatherboard home.

Construction Era (1970)

Homes built in the 1970s often have older electrical wiring, plumbing and structural systems that may not meet current building codes. Insurers view this as a higher risk for claims, particularly related to electrical faults or water damage.

Stump Foundation

Homes on stumps are common in Queensland and generally well-understood by local insurers. However, they can be more susceptible to certain types of damage (including movement and pest ingress), which may contribute modestly to the premium.

Granny Flat

The presence of a granny flat effectively increases the insurable footprint of the property. Whether it's used for family, rented out, or sits vacant, it adds to the replacement cost and the risk profile.

Solar Panels & Ducted Climate Control

Both of these add to the overall replacement cost of the home. Solar systems in particular can be expensive to replace and are increasingly factored into building sum insured calculations.

Building Sum Insured ($734,000)

At 214 sqm with a granny flat and quality fixtures, a $734,000 building sum insured is reasonable — but it's worth periodically reviewing this figure to ensure it accurately reflects current rebuild costs rather than market value. Underinsurance is a common issue in Australia, so it's important not to simply reduce this figure to lower your premium without careful consideration.

---

Tips for Homeowners in Murarrie

1. Get multiple quotes — every year The insurance market is competitive, and premiums can vary significantly between providers for the same property. Don't let your policy auto-renew without checking whether a better rate is available. Run a comparison at CoverClub to see what other insurers are offering for your home.

2. Review your building sum insured carefully Make sure your sum insured reflects the actual cost to rebuild your home — not its market value. Given the granny flat, solar panels, ducted air conditioning and the complexity of asbestos-containing materials, a professional building valuation every few years is a worthwhile investment.

3. Ask about asbestos disclosure and its impact Some insurers penalise fibro asbestos walls more heavily than others. When comparing quotes, be transparent about the wall construction and ask each insurer directly how they rate it. Specialist or Queensland-focused insurers may have more competitive pricing for pre-1980s homes.

4. Consider your excess strategically Both excesses on this policy are set at $1,000. Increasing your excess — particularly on the contents side if you have lower-value items — can reduce your annual premium. Just make sure the saving justifies the additional out-of-pocket cost in the event of a claim.

---

Ready to Compare?

If your home insurance premium is sitting above what you'd expect, you don't have to accept it. CoverClub makes it easy to compare quotes from multiple Australian insurers in one place, so you can see exactly where you stand and make an informed decision. Get a home insurance quote today and find out if there's a better deal waiting for your Murarrie property.