If you own a free standing home in Murarrie, QLD 4172, you've probably noticed that home insurance isn't cheap — and a recent quote analysed by CoverClub confirms that premiums in this inner-east Brisbane suburb can vary significantly depending on your property's characteristics. This article breaks down a real quote for a four-bedroom, three-bathroom home and puts the numbers into context so you can make a more informed decision at renewal time.

---

Is This Quote Fair?

The quote in question comes in at $4,035 per year (or $387/month) for combined Home and Contents cover, with a $734,000 building sum insured and $50,000 in contents. CoverClub's pricing engine rates this as Expensive — Above Average.

To understand why, it helps to look at what "above average" actually means in Murarrie. The suburb average premium sits at around $2,308/yr, and the median is even lower at $1,904/yr. This quote is nearly 75% above the suburb average and more than double the median — a meaningful gap that warrants some scrutiny.

That said, context matters. This property has several features that insurers treat as higher risk, which we'll unpack below. It's also worth noting that the 75th percentile for Murarrie is $3,267/yr, meaning a quarter of quotes in the area already exceed that figure. At $4,035, this quote sits above even that upper band — so while it's not an outlier in the broader Queensland or national sense, it is on the expensive side for this particular suburb.

---

How Murarrie Compares

Murarrie sits within the Brisbane LGA, and the numbers here tell an interesting story:

| Benchmark | Premium |

|---|---|

| This quote | $4,035/yr |

| Murarrie suburb average | $2,308/yr |

| Murarrie suburb median | $1,904/yr |

| Brisbane LGA average | $16,277/yr |

| QLD state average | $9,129/yr |

| QLD state median | $3,903/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

Zooming out to the Queensland state level, this quote actually looks quite reasonable. The QLD state average of $9,129/yr is more than double this premium, largely driven by high-risk cyclone and flood zones in regional and northern Queensland. The state median of $3,903/yr is closer to this quote, suggesting that for a mid-range Queensland property, $4,035 isn't dramatically out of step.

Compared to national figures, the story is similar — the national average of $5,347/yr and median of $2,764/yr bracket this quote neatly, placing it in the upper-middle range nationally.

The Brisbane LGA average of $16,277/yr is strikingly high, though this figure is likely skewed by a small number of very high-value or high-risk properties. It shouldn't be taken as a typical benchmark for most Brisbane homeowners.

For a deeper look at how Murarrie properties are priced, visit the Murarrie suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular home are likely pushing the premium above the suburb norm. Here's what insurers are likely factoring in:

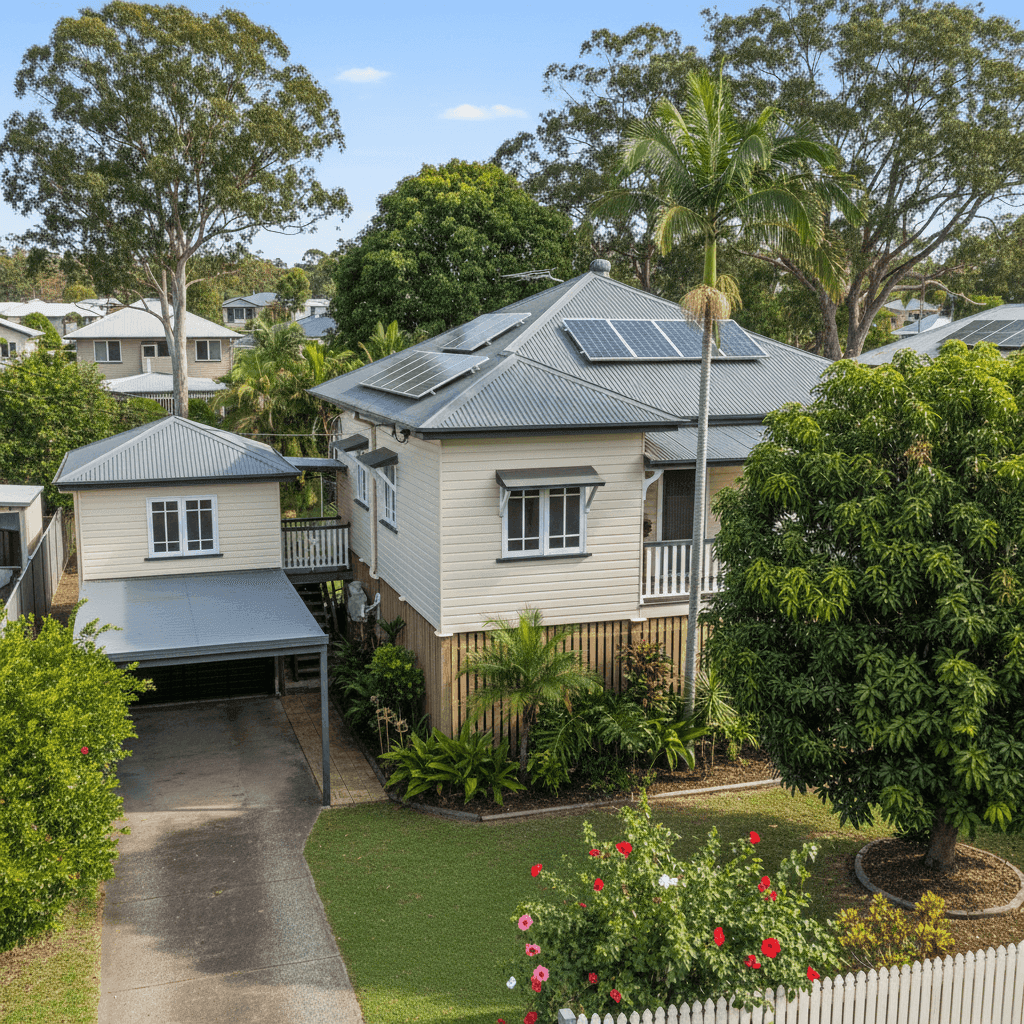

Fibro Asbestos External Walls

This is one of the most significant premium drivers. Homes built with fibro asbestos cladding — common in Queensland homes constructed around the 1970s — are more expensive to insure because repairs and rebuilds must comply with strict asbestos handling regulations. Licensed removal and disposal adds considerable cost to any claim, and insurers price accordingly.

Stump Foundation

Homes on stumps (also known as high-set or Queenslander-style foundations) are a staple of the Brisbane landscape, but they do carry specific risks — including potential for subfloor damage, termite ingress, and structural movement. Some insurers apply a loading for stump foundations, particularly on older homes.

Age of Construction (1970)

At over 50 years old, this home is considered an older dwelling by most insurers. Older properties can have outdated wiring, plumbing, and structural components that increase the likelihood and cost of a claim. The combination of age and fibro asbestos construction is a double risk flag for many underwriters.

Granny Flat

The presence of a granny flat increases the total insured area and the complexity of the risk. Whether it's used for family, rental, or storage, it adds to the rebuild cost and potential liability exposure — both of which are reflected in the premium.

Solar Panels

Solar panels are an asset worth insuring, but they also add to the replacement cost of the building. Damage from storms, hail, or fire can make solar systems expensive to repair or replace, and this is factored into the building sum insured and premium.

Ducted Climate Control

Ducted air conditioning systems are costly to replace and are typically included in the building sum insured. Their presence contributes to a higher overall rebuild cost estimate.

Building Sum Insured: $734,000

At 214 sqm, this equates to roughly $3,430 per square metre — a reasonable figure for a home with the above features, particularly given asbestos remediation costs. However, it's worth having this figure independently validated to ensure you're neither over- nor under-insured.

---

Tips for Homeowners in Murarrie

1. Get multiple quotes before renewing With a premium sitting above the suburb average, this is exactly the scenario where comparison shopping pays off. Insurers assess fibro asbestos and stump foundations very differently — some specialise in older homes and price them more competitively. Get a quote through CoverClub to see how other insurers price your specific property.

2. Review your building sum insured carefully Older homes with asbestos cladding can be genuinely expensive to rebuild due to remediation requirements, so under-insuring is a real risk. However, over-insuring also costs you money in premiums. Consider commissioning a professional building replacement cost assessment every few years to keep your sum insured accurate.

3. Ask about asbestos-specific policy terms Not all policies treat asbestos the same way. Some have exclusions or sub-limits for asbestos-related damage or removal. Before committing to a policy, read the Product Disclosure Statement (PDS) carefully and ask your insurer directly how they handle asbestos in a claim scenario.

4. Consider your excess strategically Both the building and contents excess on this quote are set at $1,000. Opting for a higher voluntary excess (say, $2,000 or $2,500) can meaningfully reduce your annual premium. If you have an emergency fund and are unlikely to make small claims, this trade-off can save you hundreds per year.

---

Compare Your Options with CoverClub

Whether you're renewing your existing policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up against real quotes from across Murarrie and Queensland. With suburb-level data and transparent comparisons, you'll know whether you're getting a fair deal — or paying too much. Start your comparison today and take the guesswork out of home insurance.