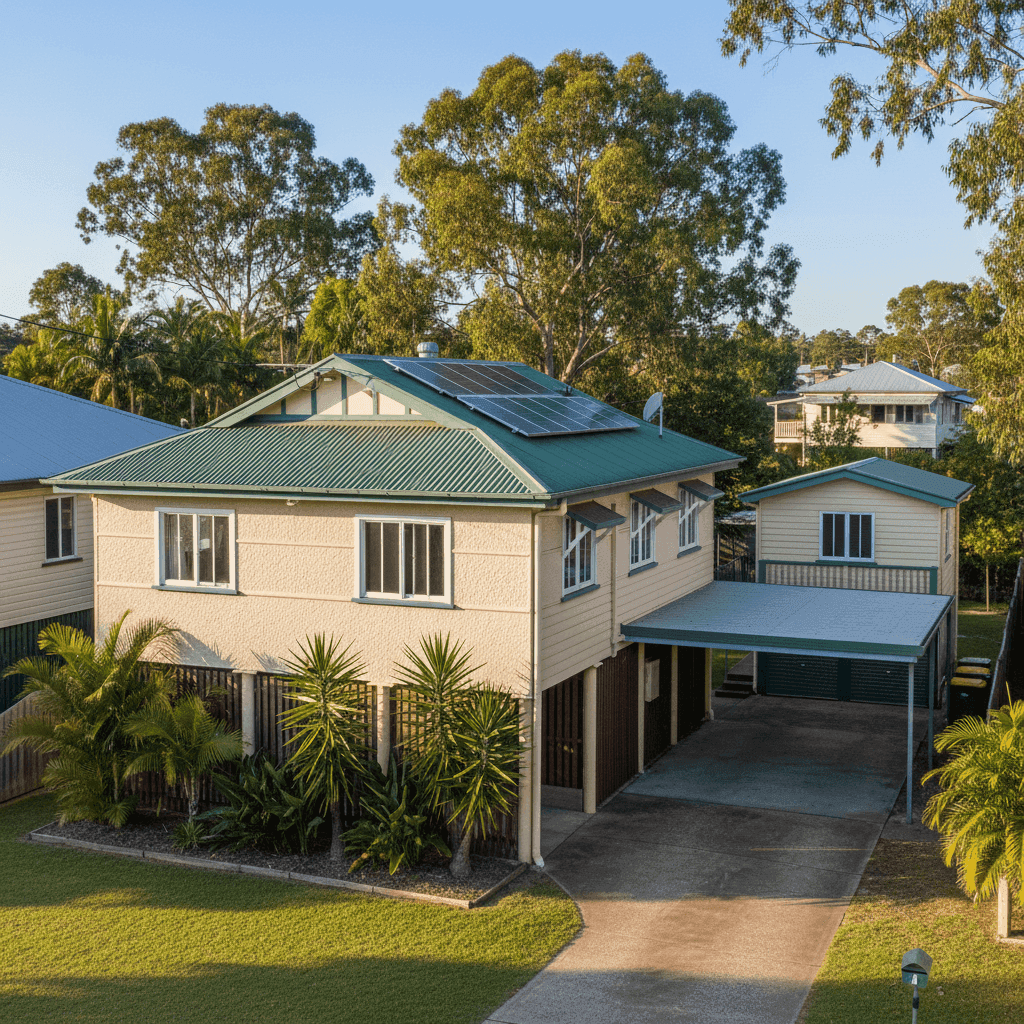

Murarrie is a well-established suburb sitting just seven kilometres east of the Brisbane CBD, popular with families drawn to its leafy streets, proximity to the Gateway Motorway, and a mix of older character homes. This article takes a close look at a real home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Murarrie (postcode 4172) — examining whether the price stacks up, how it compares to local and national benchmarks, and what property-specific factors are likely driving the cost.

---

Is This Quote Fair?

The annual premium for this property came in at $4,035 per year (or $387 per month), covering a building sum insured of $734,000 and contents valued at $50,000, each with a $1,000 excess.

Our price rating for this quote is Expensive — above average for the Murarrie area.

To put that in perspective: the suburb average premium sits at $2,308 per year, and the suburb median is even lower at $1,904. This quote lands well above both figures, and also above the suburb's 75th percentile of $3,267 — meaning it's pricier than at least three-quarters of comparable quotes we've seen for this postcode.

That said, context matters. The building sum insured here ($734,000) is substantial, which will naturally push premiums higher than properties insured for less. The presence of a granny flat, solar panels, ducted climate control, and the property's fibro asbestos construction all add layers of risk and replacement cost that insurers price carefully. So while the premium is on the higher end, it's not without explanation.

The key takeaway: this quote is above average for the suburb, but the property itself has features that justify some of that uplift. The question is whether you could find the same level of cover for less — and that's exactly where comparison shopping pays off.

---

How Murarrie Compares

Understanding where Murarrie sits in the broader insurance landscape helps frame whether this quote is a local anomaly or part of a wider trend. Here's how the numbers break down:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Murarrie (4172) | $2,308/yr | $1,904/yr |

| Queensland | $9,129/yr | $3,903/yr |

| National | $5,347/yr | $2,764/yr |

| Brisbane LGA | $16,277/yr | — |

A few things stand out here. Queensland's average premium of $9,129 is remarkably high — driven largely by cyclone-prone regions in Far North Queensland, where premiums can be extreme. Murarrie, fortunately, is not classified as a cyclone risk area, which keeps local premiums considerably more grounded.

The Brisbane LGA average of $16,277 looks alarming at first glance, but this figure is heavily skewed by high-value properties and flood-affected suburbs across the broader council area. Murarrie's own suburb averages are far more modest.

Compared to the national median of $2,764, this quote at $4,035 is still above average — but not dramatically so when you factor in the property's size, age, and construction materials.

---

Property Features That Affect Your Premium

Several characteristics of this property are likely influencing the premium, some significantly:

Fibro Asbestos External Walls

This is one of the most impactful factors. Homes built with fibro asbestos (common in Queensland homes constructed before the mid-1980s) are more expensive to insure because repairs or rebuilding require specialist licensed contractors and careful asbestos removal and disposal. Insurers factor in these elevated remediation costs, and it's reflected in the premium.

Construction Year: 1970

Older homes generally attract higher premiums. A home built in 1970 may have ageing plumbing, wiring, and structural elements that increase the likelihood of a claim. Insurers view pre-1980s construction as higher risk, particularly when combined with materials like fibro.

Stump Foundation

Homes on stumps (common in Queensland's older housing stock) can be more vulnerable to movement, moisture, and pest damage over time. Some insurers price this risk into the base premium.

Granny Flat

The presence of a granny flat increases the total insurable value of the property and adds complexity to a claim. This is typically reflected in a higher building sum insured and, consequently, a higher premium.

Solar Panels

While solar panels are a great investment for energy savings, they add to the replacement cost of the roof and can complicate claims involving storm or hail damage. Insurers account for this in their pricing.

Ducted Climate Control

Ducted systems are expensive to repair or replace, and their inclusion in the building sum insured contributes to a higher overall coverage amount.

Building Sum Insured: $734,000

At 214 square metres, the per-square-metre rebuild cost implied here is around $3,430 — which is on the higher end but not unreasonable for a home with a granny flat, ducted systems, and the added cost of asbestos-compliant construction.

---

Tips for Homeowners in Murarrie

If you're looking to get better value on your home insurance, here are some practical steps worth considering:

- Shop around — seriously. This quote came in above the suburb's 75th percentile. That means there's a real chance you could find comparable cover for several hundred dollars less per year. Use a comparison service like CoverClub to see multiple quotes side by side.

- Review your building sum insured. Make sure your sum insured reflects the actual cost to rebuild — not the market value of the property. Overinsuring can push your premium up unnecessarily, while underinsuring leaves you exposed. Consider getting a professional building valuation if you're unsure.

- Ask about asbestos disclosure and specialist cover. Not all insurers treat fibro asbestos homes the same way. Some may exclude or limit asbestos-related claims, while others offer more comprehensive cover. Always read the Product Disclosure Statement (PDS) carefully and ask your insurer directly about how they handle asbestos remediation.

- Consider a higher excess to lower your premium. Both the building and contents excess on this policy sit at $1,000. Opting for a higher excess (say, $2,000 or $2,500) could meaningfully reduce your annual premium — just make sure you're comfortable covering that amount out of pocket if you need to claim.

---

Compare Your Home Insurance Today

Whether you're renewing your policy or shopping for the first time, it pays to compare. The difference between the cheapest and most expensive quotes for a home like this in Murarrie can be thousands of dollars per year — for what is often very similar cover.

Get a home insurance quote at CoverClub and see how your current premium stacks up against the market. It takes just a few minutes, and you might be surprised at what you find.

For more data on insurance costs in this area, visit our Murarrie suburb stats page or explore Queensland-wide premium trends.