Murwillumbah is a charming hinterland town in the Tweed Valley of northern New South Wales, known for its lush green hills, heritage streetscapes, and proximity to both the Gold Coast and Byron Bay. It's also a suburb where home insurance costs can vary quite significantly — making it all the more important to understand what you're paying and why. This article breaks down a real home and contents insurance quote for a four-bedroom, three-bathroom free-standing home in Murwillumbah (postcode 2484), and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,629 per year (or $252/month), covering a building sum insured of $601,000 and contents valued at $23,000. Both the building and contents excess are set at $5,000.

Based on CoverClub's pricing data, this quote is rated CHEAP — below average for the area. That's genuinely good news for the homeowner. With a suburb average of $5,040/year and a suburb median of $3,576/year, this quote sits well below what most Murwillumbah residents are paying. In fact, it comes in beneath even the 25th percentile for the suburb ($3,439/year), meaning it's cheaper than at least 75% of comparable quotes collected in this postcode.

It's worth noting that the high excess ($5,000 for both building and contents) is likely a key driver of the lower premium. Choosing a higher excess reduces the insurer's risk exposure on smaller claims, which is reflected in a reduced upfront cost. This is a legitimate strategy for homeowners who are financially comfortable absorbing minor losses out of pocket, but it's important to go in with eyes open — if you need to claim, you'll need to cover that first $5,000 yourself.

---

How Murwillumbah Compares

To put this quote in perspective, here's how Murwillumbah stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $2,629/yr |

| Murwillumbah suburb average | $5,040/yr |

| Murwillumbah suburb median | $3,576/yr |

| Kyogle LGA average | $9,180/yr |

| NSW average | $9,528/yr |

| NSW median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

(Based on 34 quotes collected for the Murwillumbah 2484 postcode. [View full suburb stats](https://coverclub.com.au/stats/NSW/2484/murwillumbah).)

A few things stand out here. The NSW average premium of $9,528/year is extraordinarily high compared to the NSW median of $3,770 — a classic sign of a skewed distribution, where a small number of very expensive quotes (often for high-risk or high-value properties) drag the average upward. The median is almost always a more reliable indicator of what a typical homeowner pays.

Interestingly, the Kyogle LGA average of $9,180/year is also very elevated, which likely reflects the broader flood and storm risk profile of the Tweed and Richmond Valley region. Murwillumbah itself has experienced significant flood events, and insurers price that risk into their models — which makes a sub-$3,000 quote all the more noteworthy.

For broader context, you can explore NSW home insurance statistics or national home insurance benchmarks on CoverClub.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence how insurers calculate the premium.

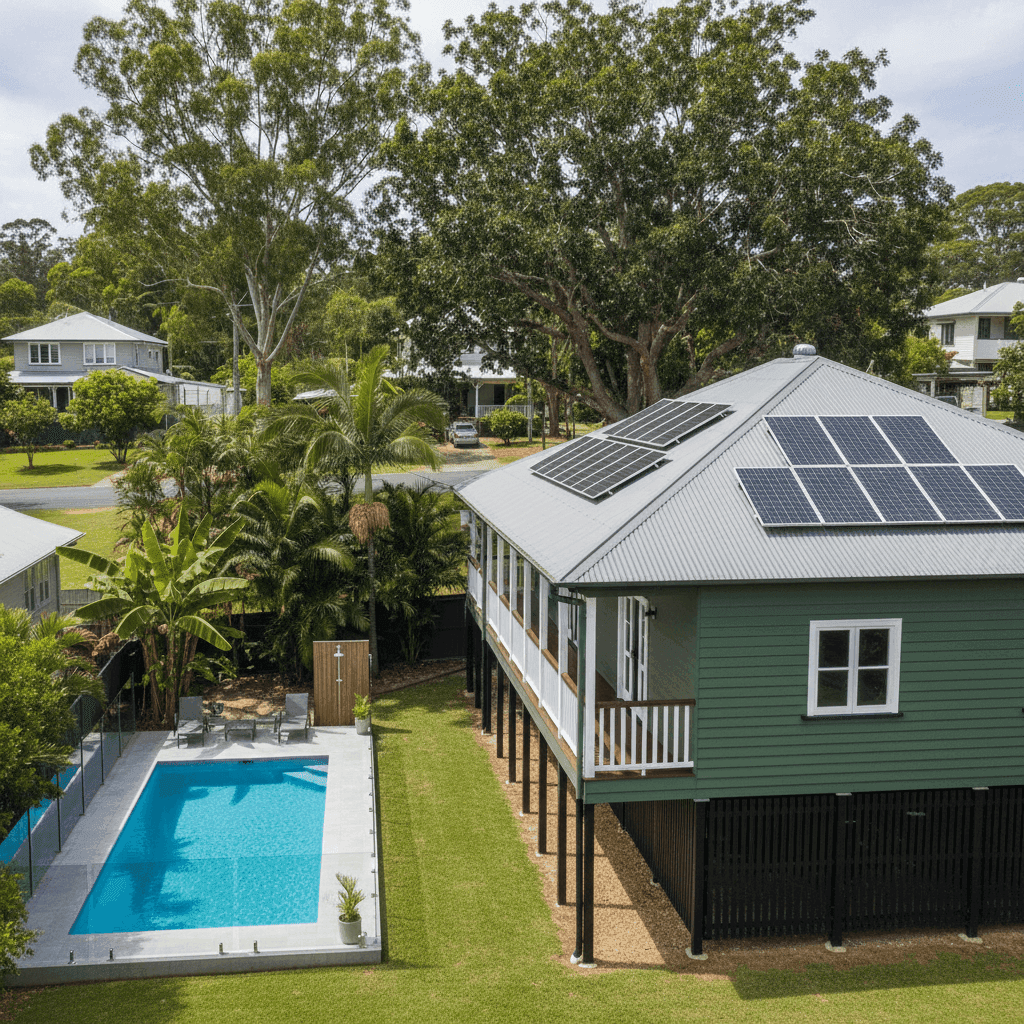

Weatherboard Timber Construction

The external walls are weatherboard wood — a construction type that's extremely common in older Australian homes, particularly in regional NSW. Timber weatherboard is generally considered higher risk than brick veneer or double brick, as it's more susceptible to fire, termite damage, and general weathering over time. Insurers typically apply a loading for this construction type, so it's somewhat surprising this quote is still rated as cheap.

Age of the Property

Built in 1946, this home is nearly 80 years old. Older homes often attract higher premiums due to ageing electrical systems, plumbing, and structural components that may be more prone to failure. The fact that this quote is competitively priced suggests the insurer may be comfortable with the property's condition or that other risk factors are mitigating the age loading.

Stump Foundation

The home sits on stumps, which is typical for older Queensland and northern NSW-style homes. Stumped foundations can be vulnerable to subsidence, moisture, and pest damage, but they also allow for better airflow and can be more resilient in flood events — a relevant consideration in the Tweed Valley.

Pool, Solar Panels & Ducted Climate Control

The presence of a swimming pool adds a small liability component to the policy. Solar panels on the roof are increasingly common and are generally covered under building insurance, though it's worth confirming the sum insured is adequate to replace them. Ducted climate control adds to the overall replacement value of the home, which is already captured in the $601,000 building sum insured.

No Cyclone Risk

Murwillumbah is not classified as a cyclone risk area, which helps keep premiums lower compared to properties in Far North Queensland or parts of WA. However, the region is still exposed to severe storms, heavy rainfall, and flooding — risks that are very much priced into local premiums.

---

Tips for Homeowners in Murwillumbah

1. Review your sum insured regularly At $601,000, the building sum insured needs to reflect the full cost of rebuilding — not the market value of the property. With construction costs rising across Australia, it's worth getting a building replacement estimate every year or two to avoid being underinsured. The Cordell Sum Sure Calculator is a free tool that can help.

2. Understand your flood cover Murwillumbah has a well-documented flood history, particularly along the Tweed River. Make sure your policy explicitly includes flood cover (not just storm or rainwater damage). Some policies treat these differently, and the distinction matters enormously when lodging a claim.

3. Consider whether a $5,000 excess is right for you The high excess on this policy is a big reason the premium is so competitive. If you'd struggle to cover a $5,000 outlay after a storm or break-in, it may be worth requesting quotes with a lower excess — even if the annual premium increases slightly. Finding the right balance is key.

4. Don't set and forget Insurance premiums change at renewal, sometimes significantly. Insurers often offer better rates to new customers than to existing ones. Make a habit of comparing quotes annually — even if you're happy with your current insurer, knowing what else is available gives you leverage to negotiate or switch.

---

Compare Home Insurance Quotes in Murwillumbah

Whether you're a first-time buyer or a long-term Murwillumbah resident, getting the right home and contents cover at a fair price takes a little homework. CoverClub makes it easy to compare quotes from multiple insurers in one place, so you can see exactly where your premium sits relative to the market. Get a home insurance quote today and find out if you're paying too much.