Myrtle Bank is a leafy, sought-after suburb in Adelaide's inner south, sitting within the City of Mitcham. Known for its period character homes, tree-lined streets, and proximity to the Mitcham Hills, it's a suburb where properties tend to be substantial — and where getting home insurance right really matters. This article breaks down a real home and contents insurance quote for a five-bedroom, free-standing home in Myrtle Bank (postcode 5064), and puts the numbers in context so you can judge whether your own premium is competitive.

---

Is This Quote Fair?

The annual premium on this quote comes in at $2,002 per year (or $196/month) for a home and contents policy covering a building sum insured of $1,088,000 and $50,000 worth of contents. Both the building and contents excesses are set at $1,000.

Our price rating for this quote is CHEAP — below average — which is genuinely good news for the homeowner. To put that in perspective:

- The South Australian state average premium is $2,433/yr — meaning this quote is around $431 cheaper than the typical SA policyholder pays.

- The LGA (Mitcham) average sits at $2,403/yr, so this quote also undercuts the local government area benchmark by a meaningful margin.

- Against the national average of $5,347/yr, this quote looks exceptionally competitive — less than 40% of what the average Australian homeowner pays across the country.

It's worth noting that averages can be skewed by high-risk regions (think cyclone-prone Queensland or flood-affected areas in NSW), so the national figure should be taken with some context. Still, even against the more moderate national median of $2,764/yr, this quote comes in noticeably below the midpoint.

For a property of this size and age, a sub-$2,100 annual premium represents solid value — particularly given the features on this home (more on those below).

---

How Myrtle Bank Compares

While suburb-level data for Myrtle Bank isn't available in sufficient volume to produce a statistically robust local average, we can draw on broader benchmarks to frame the picture. You can explore SA home insurance statistics and national home insurance data on CoverClub for the full picture.

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,002 |

| SA State Average | $2,433 |

| SA State Median | $1,679 |

| LGA (Mitcham) Average | $2,403 |

| National Average | $5,347 |

| National Median | $2,764 |

The SA median of $1,679/yr is lower than this quote, which is worth acknowledging — medians strip out the influence of very high and very low premiums, so roughly half of SA homeowners are paying less than $1,679. However, many of those properties will be smaller, newer, or carry lower sums insured. A five-bedroom home with a $1,088,000 building cover in an established suburb like Myrtle Bank is a materially different risk profile to the median SA property.

When you factor in the property's size, age, and features, landing at $2,002/yr is a genuinely competitive outcome. Check out the Myrtle Bank suburb stats page as more local data becomes available over time.

---

Property Features That Affect Your Premium

Several characteristics of this property will have influenced the premium — some favourably, some less so. Here's how the key features play out:

Double Brick Construction

Double brick is one of the most robust and fire-resistant wall materials available, and insurers generally view it favourably. It's structurally durable, offers good thermal performance, and tends to hold up well in storms. This construction type is common in Adelaide's older inner suburbs and typically attracts lower premiums compared to lightweight or clad alternatives.

Steel / Colorbond Roof

A Colorbond steel roof is considered a low-risk roofing material — it's durable, fire-resistant, and less prone to storm damage than older terracotta or concrete tiles. Replacing an ageing original roof with Colorbond is a common upgrade in heritage-era homes, and it can have a positive effect on premiums.

Stump Foundation

This is a 1930s home, so stump foundations are entirely expected. While stumps themselves aren't inherently problematic, older properties on stumps can be more susceptible to subsidence or movement over time — particularly in areas with reactive clay soils, which are common across parts of Adelaide. Some insurers factor this into their risk assessment.

Timber / Laminate Flooring

Timber floors in older homes can be a double-edged sword for insurers. On one hand, they're a desirable feature; on the other, they can be more susceptible to water damage and are costlier to repair or replace than concrete slab alternatives. This may have a modest upward effect on the premium.

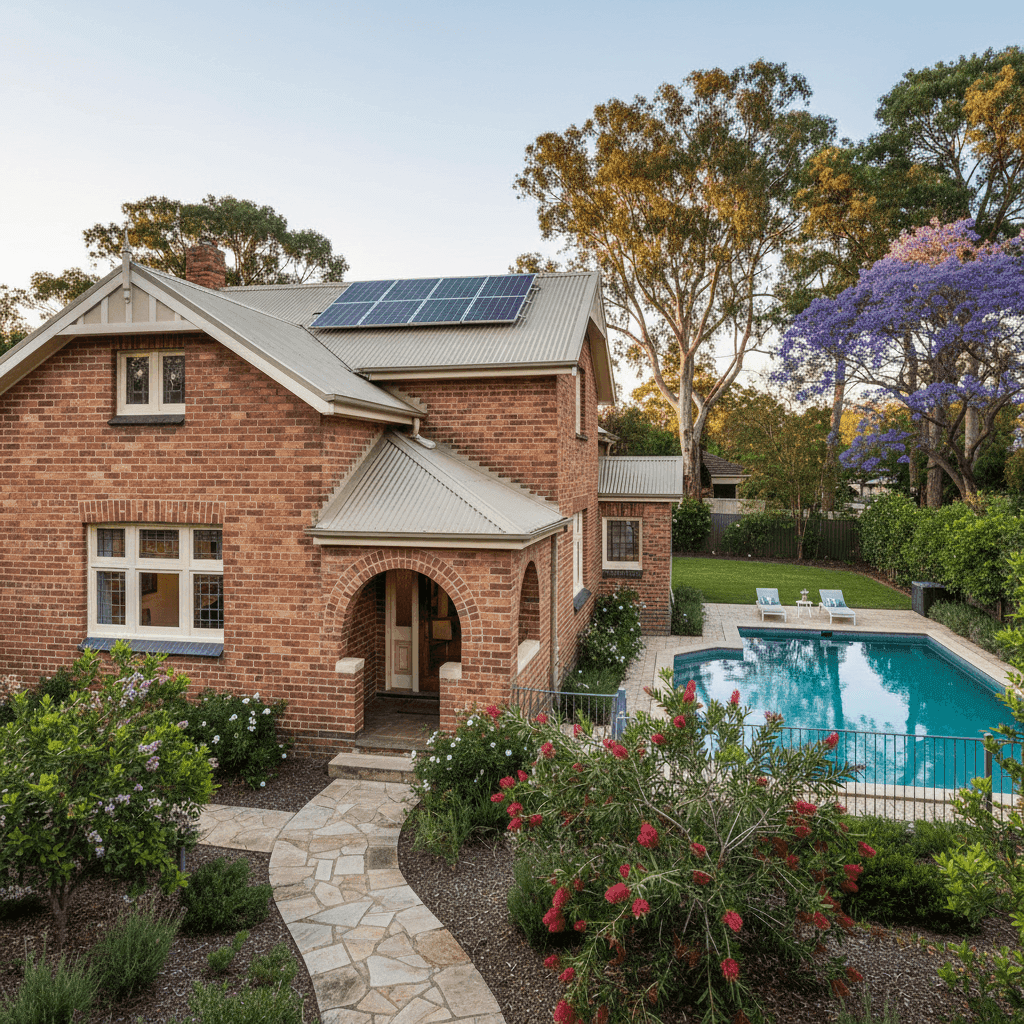

Pool, Solar Panels & Ducted Climate Control

The presence of a swimming pool adds liability exposure (though this is typically covered under home insurance rather than a separate policy). Solar panels increase the replacement cost of the building and may require specific coverage confirmation with your insurer. Ducted climate control is a significant fixed asset that should be captured in your building sum insured — and at $1,088,000, this quote appears to account for the property's full replacement value appropriately.

1930s Heritage Era

Older homes often cost more to rebuild due to the use of period materials, craftsmanship, and compliance with modern building codes during reinstatement. A sum insured of $1,088,000 for a 277 sqm home built in 1930 reflects this reality — and getting the sum insured right is critical to avoiding underinsurance.

---

Tips for Homeowners in Myrtle Bank

1. Review your sum insured regularly Construction costs have risen sharply in recent years. A building sum insured that was accurate two years ago may no longer reflect the true cost of rebuilding your home today. Use a building cost calculator annually and adjust your cover accordingly — underinsurance can leave you significantly out of pocket after a major claim.

2. Confirm solar panel coverage with your insurer Not all standard home insurance policies automatically cover solar panel systems to their full value. Check whether your panels are included in your building sum insured and whether the policy covers both physical damage and any associated electrical components.

3. Maintain your stumps Subsidence and foundation movement are among the more common — and expensive — issues in older Adelaide homes. Regular inspection of your subfloor and stumps by a qualified builder can help catch problems early and may also support your insurance position if you ever need to make a claim related to structural movement.

4. Compare quotes before renewal Loyalty doesn't always pay in insurance. Premiums can vary significantly between providers for the same property and level of cover. Given this quote is already rated as below average in price, it's a good benchmark — but it's still worth comparing at renewal to ensure you're getting the best combination of price and coverage.

---

Ready to Compare?

Whether you're a Myrtle Bank local or simply curious about what your home might cost to insure, CoverClub makes it easy to get a real quote in minutes. Enter your address at CoverClub and see how your premium stacks up against SA and national benchmarks — no obligation, no jargon.