Nambour, nestled in the hinterland of Queensland's Sunshine Coast, is a well-established suburb that blends suburban convenience with a relaxed regional lifestyle. For owners of a free standing home here, understanding what you're paying for home insurance — and whether it represents good value — is an important part of protecting one of your biggest assets. This article breaks down a recent home and contents insurance quote for a four-bedroom, two-bathroom property in Nambour (postcode 4560), and puts the numbers in context using real suburb, state, and national data.

---

Is This Quote Fair?

The quote in question comes in at $2,545 per year (or $249/month) for combined home and contents cover, with a building sum insured of $758,000 and contents valued at $50,000. Both the building and contents excess are set at $500.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. At $2,545/yr, this premium sits comfortably below the Nambour suburb average of $2,806/yr and also under the suburb median of $2,731/yr. That means this homeowner is paying less than what most comparable properties in the area are quoted — a solid outcome.

It's worth noting that the suburb's pricing spreads quite widely. The 25th percentile sits at $1,839/yr, meaning a quarter of quotes in the area come in below that mark, while the 75th percentile reaches $3,284/yr. This quote lands between the median and the 75th percentile, which is a reasonable position — not the cheapest available, but well within a normal range for the area.

---

How Nambour Compares

To truly appreciate this quote, it helps to zoom out and look at the broader picture. You can explore the full breakdown on the Nambour suburb stats page.

| Benchmark | Premium |

|---|---|

| This Quote | $2,545/yr |

| Nambour Suburb Average | $2,806/yr |

| Nambour Suburb Median | $2,731/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| Sunshine Coast LGA Average | $7,249/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The contrast with Queensland's state average of $9,129/yr is striking — but that figure is heavily skewed by high-risk coastal and cyclone-prone areas in Far North Queensland, where premiums can be eye-watering. The QLD state stats page gives a fuller picture of how premiums vary across the state.

Even against the more grounded state median of $3,903/yr, this Nambour quote looks competitive. And when compared to the national average of $5,347/yr, it's well below the mark — reflecting that Nambour, while in Queensland, doesn't carry the extreme risk loading that affects many parts of the state.

The Sunshine Coast LGA average of $7,249/yr is notably high, likely driven by beachside and flood-prone pockets within the region. Nambour's hinterland location helps insulate it from some of the coastal risk factors that push premiums up elsewhere on the Coast.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers price the risk.

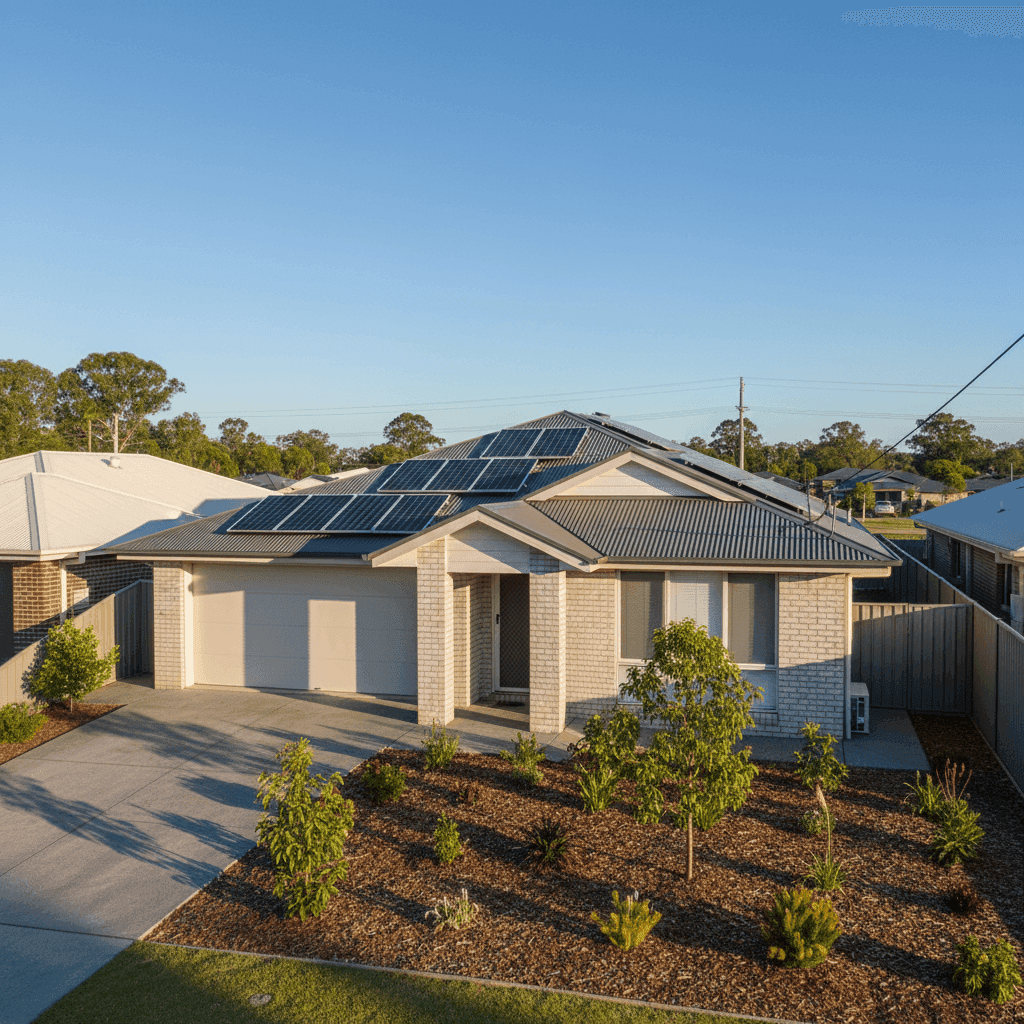

Brick Veneer Walls & Colorbond Roof Brick veneer construction is viewed favourably by insurers — it's durable, fire-resistant, and holds up well in storms. Paired with a steel Colorbond roof, this home has a combination that typically attracts lower premiums than, say, weatherboard cladding or older tile roofs. Colorbond is lightweight, resistant to corrosion, and performs well in high-wind events.

Slab Foundation & Tiled Flooring A concrete slab foundation is a standard and reliable base for homes built in Queensland's climate. It reduces the risk of subfloor moisture damage and pest intrusion. Tiled flooring throughout is also a practical choice that's easy to maintain and resistant to water damage — both factors that can reduce the likelihood of contents claims.

Built in 2015 At roughly a decade old, this home sits in a sweet spot for insurers. It's modern enough to comply with contemporary building codes (including post-2011 cyclone and flood-aware standards), yet established enough to have a known track record. Newer builds generally attract more competitive premiums than older homes that may have ageing electrical systems or outdated plumbing.

Solar Panels The presence of solar panels adds a small layer of complexity to a home insurance policy. Panels are typically covered under the building sum insured, so it's important to ensure the $758,000 building value adequately accounts for their replacement cost. Solar systems can also be a target for hail damage, so checking your policy's specific inclusions for panels is worthwhile.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and is generally covered under building insurance. Again, this reinforces the importance of ensuring your building sum insured is sufficient — ducted systems can cost $10,000–$20,000 or more to replace.

No Pool, No Cyclone Risk Zone The absence of a swimming pool removes a common liability risk factor. And while Nambour sits in Queensland, it falls outside the designated cyclone risk zone — a significant premium advantage compared to properties in North Queensland.

---

Tips for Homeowners in Nambour

1. Review Your Building Sum Insured Annually Construction costs have risen sharply in recent years. With solar panels and ducted climate control factored in, a $758,000 sum insured needs to reflect genuine rebuild costs — not just the market value of the home. Use a building calculator or ask your insurer to confirm the figure is adequate.

2. Don't Overlook Flood Cover Parts of the Sunshine Coast hinterland, including areas around Nambour, have experienced flooding historically. Check whether your policy explicitly includes flood cover (not just storm damage), as some policies treat these as separate events. If flood cover isn't included, it may be worth adding.

3. Bundle Home and Contents Strategically This quote covers both home and contents under a single policy. While bundling is often convenient and can attract discounts, it's worth comparing standalone policies too — sometimes splitting cover across providers can result in better overall value.

4. Increase Your Excess to Lower Your Premium With both excesses currently set at $500, there's room to consider raising them if you're comfortable self-funding smaller claims. Moving to a $1,000 excess can meaningfully reduce your annual premium, particularly on the building component.

---

Compare Your Options at CoverClub

Whether you're renewing your policy or shopping around for the first time, it pays to see how your current quote stacks up. CoverClub makes it easy to compare home and contents insurance quotes for properties across Australia, with real pricing data from your suburb and beyond. Get a quote today and find out if you're getting the best deal for your Nambour home.