Nestled on the Central Coast of New South Wales, Narara is a well-established suburb offering a blend of quiet residential living and convenient access to Gosford's amenities. For owners of a free standing home in this area, understanding what you should be paying for home and contents insurance — and why — can make a real difference to your household budget. This article breaks down a recent quote for a 3-bedroom, 2-bathroom brick veneer home in Narara (postcode 2250) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $3,294 per year (or roughly $316 per month), covering both building (insured at $697,000) and contents (valued at $117,000), each with a $1,000 excess.

Our price rating for this quote is CHEAP — below average for the area. That's genuinely good news for the homeowner. To put it plainly: this quote sits comfortably below the suburb median of $4,186 per year and well below the 25th percentile threshold of $3,748 per year. In other words, this premium is more affordable than at least three-quarters of comparable quotes we've seen for Narara properties.

It's worth noting that the suburb average of $95,903 per year is a statistical outlier — almost certainly skewed upward by a small number of high-risk or high-value properties in the dataset (the suburb sample size is just 11 quotes). The median figure of $4,186 is a far more reliable benchmark for typical Narara homeowners, and this quote beats it by nearly $900 annually.

At the state level, the NSW average premium sits at $9,528 per year, though the NSW median is a more grounded $3,770. This quote comes in just below that state median too — a solid result. Compared to the national average of $5,347 and a national median of $2,764, this premium is right in the competitive zone for a comprehensive home and contents policy.

---

How Narara Compares

Here's a snapshot of how this quote sits relative to broader benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $3,294/yr |

| Narara Suburb Median | $4,186/yr |

| Narara 25th Percentile | $3,748/yr |

| NSW State Median | $3,770/yr |

| National Median | $2,764/yr |

| National Average | $5,347/yr |

| NSW State Average | $9,528/yr |

This quote undercuts both the suburb and state medians, which is a strong outcome. The nearby Hawkesbury LGA average of $10,350 per year — significantly higher — is a reminder of how dramatically flood and bushfire risk can inflate premiums in parts of regional NSW. Narara, by contrast, carries a more moderate risk profile, which is reflected in this competitive pricing.

You can explore more data for this postcode on the Narara suburb stats page.

---

Property Features That Affect Your Premium

Several characteristics of this particular property influence where its premium lands — for better or worse.

Brick Veneer Walls & Tiled Roof

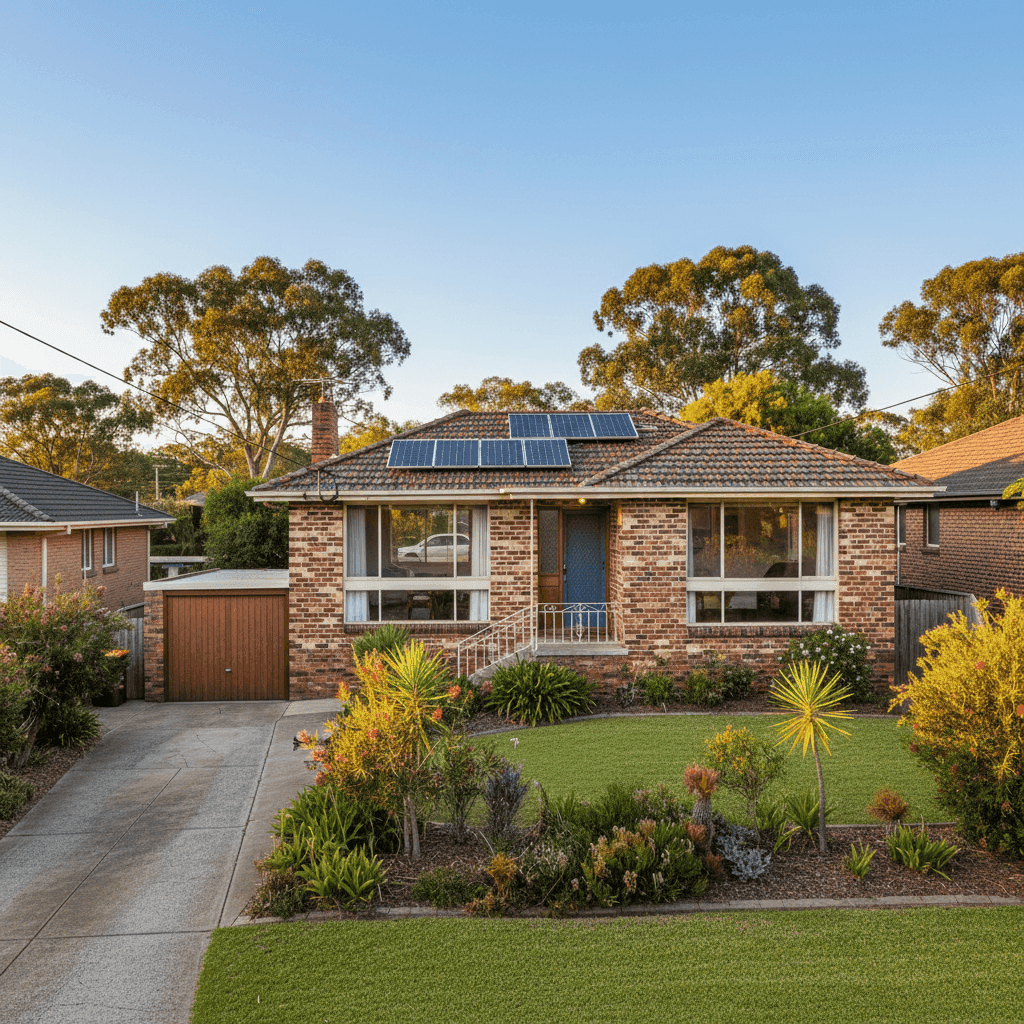

Brick veneer construction is generally viewed favourably by insurers. It offers good fire resistance and structural durability compared to weatherboard or fibre cement alternatives. Combined with a tiled roof — another robust and low-maintenance material — this home presents a relatively low-risk profile from a building construction standpoint.

Built in 1975

Homes from the mid-1970s are common across the Central Coast and are well understood by insurers. That said, a property of this age may have older plumbing, wiring, or roofing materials that could attract a slight loading. It's worth ensuring your sum insured of $697,000 accurately reflects current rebuild costs, including demolition and professional fees, which have risen sharply in recent years due to construction inflation.

Stump Foundation & Timber/Laminate Flooring

A stump (or pier) foundation is common in older NSW homes and can be both a blessing and a consideration. On the upside, it allows for airflow beneath the home, reducing moisture-related issues. However, stumps can deteriorate over time, and some insurers factor this into their risk assessment. The timber and laminate flooring is consistent with this foundation type and is standard for the era.

Solar Panels

This property includes solar panels, which are increasingly common across Australian homes. Insurers treat solar panels differently — some include them under building cover automatically, while others require them to be specifically listed. It's essential to confirm with your insurer that your solar system is covered under your building sum insured, particularly given the replacement cost of modern solar arrays.

Ducted Climate Control

Ducted air conditioning adds value to the property and is typically covered under building insurance as a fixed installation. However, it also adds to the overall rebuild cost, so homeowners should ensure their building sum insured accounts for this system.

No Pool, No Cyclone Risk

The absence of a swimming pool removes a common source of liability and maintenance claims. And being outside a designated cyclone risk zone (unlike parts of Queensland or northern WA) means this home avoids the significant premium loadings that apply in those regions.

---

Tips for Homeowners in Narara

1. Review your sum insured regularly With construction costs rising across NSW, the $697,000 building sum insured should be reviewed at each renewal. Use a building cost calculator or consult a quantity surveyor to confirm your coverage keeps pace with actual rebuild costs — underinsurance is one of the most common and costly mistakes homeowners make.

2. Confirm solar panel coverage explicitly Don't assume your solar panels are automatically covered. Ask your insurer directly whether the panels, inverter, and associated wiring are included in your building sum insured, and whether accidental damage or storm damage is covered.

3. Shop around at renewal time Even with a below-average premium, the insurance market changes every year. Insurers reprice based on claims data, reinsurance costs, and local risk assessments. Comparing quotes annually — rather than auto-renewing — can help you maintain competitive pricing.

4. Consider your excess carefully Both the building and contents excess on this policy sit at $1,000. Opting for a higher excess (say, $2,000) can reduce your annual premium, but only makes sense if you're financially comfortable covering that amount out of pocket in the event of a claim. Conversely, a lower excess may be worth the slightly higher premium for peace of mind.

---

Compare Your Own Quote

Whether you're a Narara local or looking at properties across the Central Coast, it pays to see what the market can offer. CoverClub aggregates real insurance data so you can make informed decisions — not just accept the first renewal notice that arrives in the mail. Get a home insurance quote today and see how your premium stacks up.