Narellan Vale is a well-established residential suburb in the Macarthur region of south-west Sydney, sitting within the Campbelltown local government area. It's a popular choice for families, thanks to its quiet streets, proximity to Camden and good access to the M5 and M7 motorways. For homeowners here, understanding what drives the cost of home insurance — and whether a quote stacks up — can mean the difference between overpaying and getting genuinely good value.

This article breaks down a recent home and contents insurance quote for a four-bedroom, free-standing brick veneer home in Narellan Vale, comparing it against local, state and national benchmarks.

---

Is This Quote Fair?

The annual premium for this property came in at $1,732 per year (or about $166 per month), covering both building ($600,000 sum insured) and contents ($100,000), each with a $1,000 excess. Our pricing engine rates this quote as FAIR — Around Average.

That assessment holds up when you look at the numbers. The suburb average for comparable properties in Narellan Vale sits at $1,718 per year, meaning this quote is only $14 above the local average — a negligible difference. The suburb median is slightly lower at $1,653 per year, which suggests a modest cluster of cheaper quotes pulling the midpoint down, but this premium is well within normal range.

The middle 50% of quotes in the suburb fall between $1,248 and $2,252 per year (the 25th and 75th percentiles), so at $1,732, this property sits comfortably in the middle of that band — closer to the upper half, but far from the most expensive policies being written in the area.

In short: you're not getting a bargain, but you're not being stung either. There's room to improve, but this quote is broadly in line with what Narellan Vale homeowners are paying.

---

How Narellan Vale Compares

One of the more striking takeaways from this data is just how affordable Narellan Vale is relative to broader benchmarks. Check out the full suburb stats for Narellan Vale (NSW 2567) to explore the complete picture.

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Narellan Vale (2567) | $1,718/yr | $1,653/yr |

| Campbelltown LGA | $1,893/yr | — |

| NSW State | $9,528/yr | $3,770/yr |

| National | $5,347/yr | $2,764/yr |

The NSW state average of $9,528 per year looks alarming at first glance, but it's heavily skewed by high-risk and high-value properties across the state — coastal flood zones, bushfire-prone regions and prestige properties in Sydney's eastern suburbs all drag that figure upward. The NSW state insurance stats give useful context here. The median of $3,770 is a more grounded comparison point, and even against that figure, Narellan Vale homeowners are paying less than half.

Against national benchmarks, the story is similar. The national average of $5,347 and median of $2,764 both sit well above what's being quoted in this suburb. That reflects Narellan Vale's relatively low-risk profile — it's not in a cyclone zone, it's not coastal, and while parts of south-west Sydney can experience storm activity, the area doesn't carry the same elevated risk loading as many other parts of the country.

Even within the Campbelltown LGA, Narellan Vale performs well, with the LGA average at $1,893 compared to the suburb average of $1,718 — suggesting this particular pocket of the LGA attracts more competitive pricing.

---

Property Features That Affect Your Premium

Several characteristics of this property influence the premium calculation, both positively and negatively.

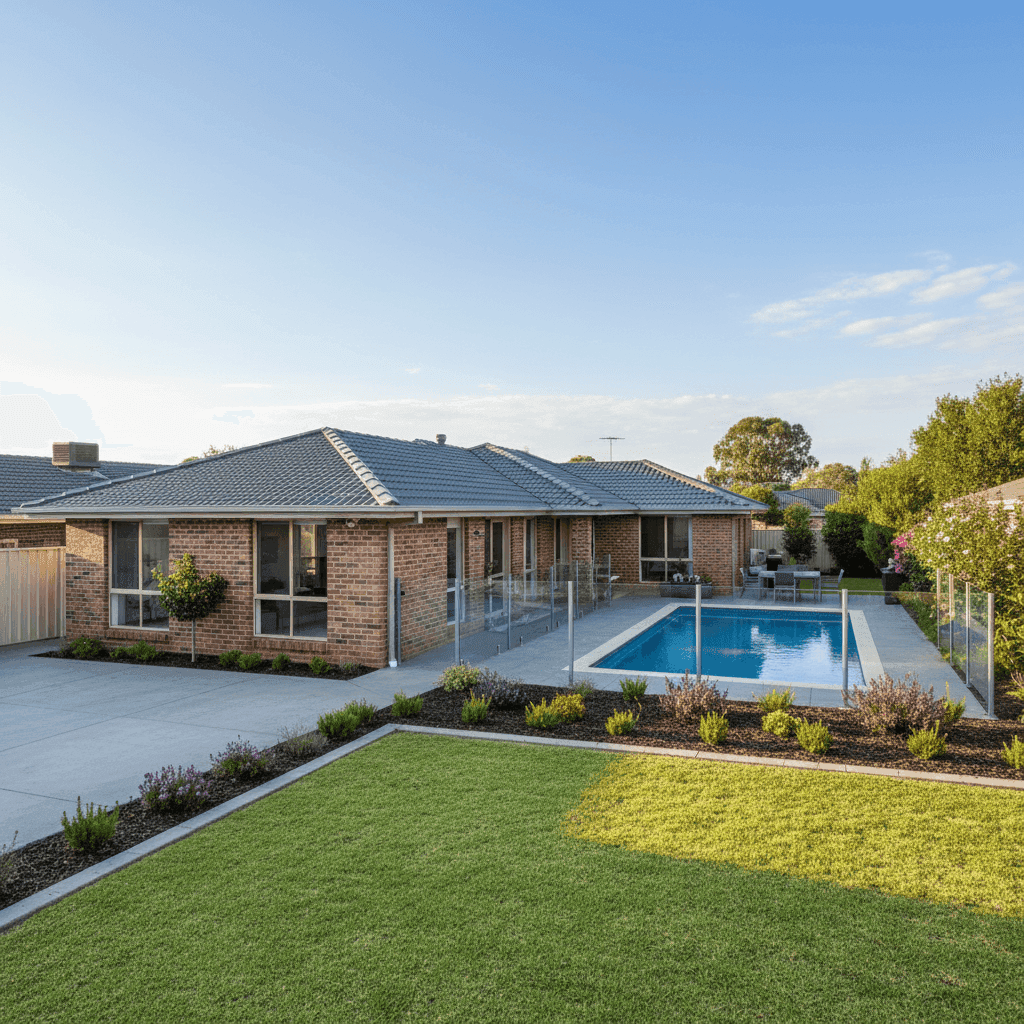

Brick veneer construction is generally viewed favourably by insurers. It offers solid fire resistance and durability compared to timber-framed or clad exteriors, which can translate to lower risk loading on the building component of a policy.

Tiled roofing is another positive signal. Terracotta or concrete tiles are considered more resilient than Colorbond or corrugated iron in certain weather conditions, and they carry a lower fire risk than some older roofing materials.

Slab foundation is standard for homes of this era in south-west Sydney and doesn't introduce any unusual risk factors. Similarly, tiled flooring throughout is a practical, low-maintenance choice that insurers tend to view neutrally.

The swimming pool is worth noting. Pools add a layer of liability risk to a property — accidental injury is a genuine exposure — and they can also increase the replacement cost of the property. Insurers factor this in, and it's one reason why some quotes for pool-equipped homes sit slightly above the suburb median.

Ducted climate control adds to the insured value of the home's fixtures and fittings. Ducted systems are expensive to replace, and their presence is reflected in the building sum insured. Ensuring your sum insured accurately accounts for this system is important — underinsurance is a real risk if you've upgraded or installed ducted air conditioning since your policy was first written.

The property was built in 1990, which puts it in a middle ground — not old enough to raise significant concerns about outdated wiring or plumbing, but not new enough to benefit from the most modern building standards. At 130 sqm, it's a modest footprint for a four-bedroom home, which helps keep the building replacement cost — and therefore the premium — manageable.

---

Tips for Homeowners in Narellan Vale

1. Review your building sum insured regularly Construction costs have risen sharply in recent years. A sum insured of $600,000 for a 130 sqm brick veneer home is substantial, but it's worth stress-testing that figure against current builder rates in south-west Sydney. Use a building cost calculator or ask your insurer how they've arrived at the figure — underinsurance can leave you significantly out of pocket after a major claim.

2. Consider raising your excess to reduce your premium Both the building and contents excess on this policy sit at $1,000. Many insurers will offer a meaningful premium discount if you opt for a higher voluntary excess — say $2,500 or $5,000. If you have an emergency fund and are unlikely to make small claims, this can be an effective way to lower your annual cost.

3. Shop around at renewal time The 48-quote sample for Narellan Vale shows a wide spread — from $1,248 at the 25th percentile to $2,252 at the 75th. That's a $1,000 gap between the cheapest and more expensive policies for broadly similar properties. Loyalty doesn't always pay in insurance; comparing quotes annually is one of the simplest ways to avoid drifting into the upper end of that range.

4. Check your pool and outbuilding coverage If your policy includes a swimming pool, confirm exactly what's covered — pool equipment, fencing, and surrounding structures like pump sheds or decking can sometimes fall into grey areas depending on the policy wording. Make sure your contents sum insured also reflects any outdoor furniture, BBQ equipment or garden tools you'd want replaced.

---

Compare Home Insurance Quotes in Narellan Vale

Whether you're renewing an existing policy or shopping for the first time, it pays to see what the market is offering. CoverClub makes it easy to compare home and contents insurance quotes for properties across Narellan Vale and the wider Macarthur region. Get a quote today and find out where your premium sits relative to your neighbours.