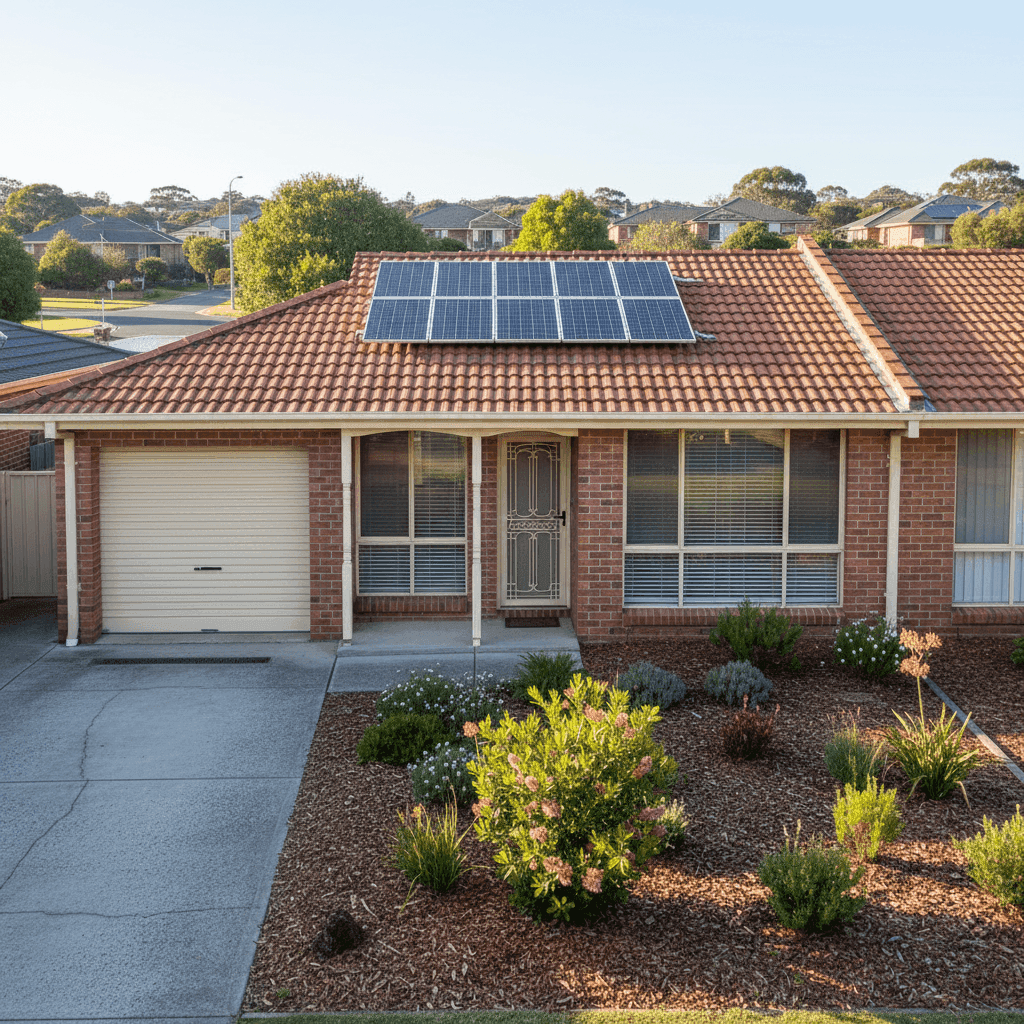

Nelson Bay is one of the jewels of the Port Stephens region — a coastal town known for its dolphin-watching cruises, pristine beaches, and relaxed lifestyle. It's also a suburb where property owners need to think carefully about home insurance, given the mix of coastal exposure, an ageing housing stock, and a property market that has grown considerably in value over recent years. This article breaks down a real home and contents insurance quote for a four-bedroom, brick veneer semi detached home in Nelson Bay (postcode 2315), built in 1991, and helps you understand whether the premium stacks up.

---

Is This Quote Fair?

The quote in question comes to $2,401 per year (or $246/month) for combined home and contents cover, with a building sum insured of $662,000 and contents valued at $96,000. The building excess is $3,000 and the contents excess is $1,000.

Our pricing engine rates this quote as Fair — Around Average, and the data backs that up. The suburb average premium for Nelson Bay sits at $2,314/year, meaning this quote is only about $87 above the local average — a difference of less than 4%. That's well within the normal range of variation you'd expect based on individual property characteristics, chosen insurer, and specific cover inclusions.

It's worth noting that the suburb median is slightly lower at $2,173/year, which suggests a modest skew from a handful of higher-priced quotes pulling the average up. At $2,401, this quote sits comfortably between the suburb median and the 75th percentile ($2,778/year), placing it in the middle-to-upper portion of the local market — not a bargain, but certainly not overpriced either.

For homeowners comparing options, this rating is a reasonable starting point. A "Fair" rating doesn't mean you can't do better — it means the quote is competitive enough that you're not being significantly overcharged, but shopping around could still yield meaningful savings.

---

How Nelson Bay Compares

Understanding where Nelson Bay sits in the broader insurance landscape is essential context for any homeowner. Here's how the numbers line up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $2,401 |

| Nelson Bay Suburb Average | $2,314 |

| Nelson Bay Suburb Median | $2,173 |

| Port Stephens LGA Average | $3,116 |

| NSW State Average | $9,528 |

| NSW State Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

A few things stand out here. First, Nelson Bay's premiums are notably lower than both the NSW state average and the national average — the NSW average of $9,528/year is dramatically higher, largely driven by high-value properties in Sydney and flood-affected regional areas. Even the NSW median of $3,770/year is well above what Nelson Bay homeowners are typically paying.

Second, this quote also comes in under the Port Stephens LGA average of $3,116/year, which is a meaningful comparison given that the LGA includes a range of property types and risk profiles across the broader region.

For a deeper look at how Nelson Bay's insurance costs break down across different property types and cover levels, visit the Nelson Bay suburb stats page.

---

Property Features That Affect Your Premium

Every home insurance quote is shaped by the specific characteristics of the property. Here's how the features of this particular home are likely influencing the premium:

Brick Veneer Walls & Tiled Roof Brick veneer construction with a tiled roof is one of the more insurer-friendly combinations in Australia. Brick veneer offers solid fire resistance and structural durability, while tiles are considered a lower-risk roofing material compared to metal or, particularly, older materials like fibro or asbestos sheeting. This combination generally attracts more competitive premiums.

Slab Foundation A concrete slab foundation is standard for homes of this era and is generally viewed favourably by insurers. It reduces the risk of subsidence-related claims and is less susceptible to termite damage than older timber-framed sub-floor systems.

Construction Year: 1991 At around 34 years old, this home is in a middle-ground age bracket. It's old enough that some components — roofing, plumbing, electrical — may be approaching the end of their serviceable life, but it was built under reasonably modern building codes. Insurers may factor in the age of the property when assessing risk.

Solar Panels The presence of solar panels is worth flagging. Most standard home insurance policies cover rooftop solar panels as part of the building, but it's important to confirm this with your insurer. Panels add replacement value to the building sum insured and can occasionally be a source of claims if damaged by storms or hail.

Ducted Climate Control Ducted air conditioning systems are a fixed building improvement and should be included in the building sum insured. At 235 sqm, this is a reasonably sized home, and the ducted system would contribute meaningfully to the overall rebuild cost.

Timber/Laminate Flooring & Standard Fittings Standard-quality fittings and timber or laminate flooring are reflected in the $662,000 building sum insured. This figure needs to accurately represent the full cost of rebuilding the home from scratch — not its market value — so it's worth reviewing periodically as construction costs rise.

No Pool, No Cyclone Risk The absence of a pool removes a common liability concern, and Nelson Bay falls outside designated cyclone risk zones, which keeps premiums lower than comparable coastal properties in Queensland or northern NSW.

---

Tips for Homeowners in Nelson Bay

1. Review Your Building Sum Insured Annually Construction costs have risen sharply across Australia in recent years. A sum insured of $662,000 may have been appropriate when the policy was first taken out, but it's worth checking against a current building cost calculator to ensure you're not underinsured. Underinsurance is one of the most common — and costly — mistakes homeowners make.

2. Check Your Solar Panel Cover With solar panels on the roof, confirm with your insurer exactly how they're covered. Are they included under the building policy? What events are they protected against? Some policies have specific exclusions or sub-limits for solar systems, so it pays to read the Product Disclosure Statement carefully.

3. Consider Your Excess Strategy This quote carries a $3,000 building excess and a $1,000 contents excess. A higher excess typically reduces your premium, but make sure the excess is an amount you could comfortably pay in the event of a claim. If $3,000 would be a financial stretch, it may be worth comparing quotes with a lower excess — even if the annual premium is slightly higher.

4. Shop Around at Renewal Insurance loyalty rarely pays. Insurers often reserve their best rates for new customers, meaning long-term policyholders can end up paying more than necessary. Set a reminder to compare quotes before each annual renewal — even if your current insurer offers a competitive rate, you won't know unless you check.

---

Compare Home Insurance Quotes in Nelson Bay

Whether this quote is the right fit depends on your individual circumstances, risk tolerance, and what's included in the policy. The premium looks reasonable based on the available data, but the best way to know for certain is to compare multiple quotes side by side. Head to CoverClub to get a home insurance comparison tailored to your Nelson Bay property — it takes just a few minutes and could save you hundreds of dollars a year.