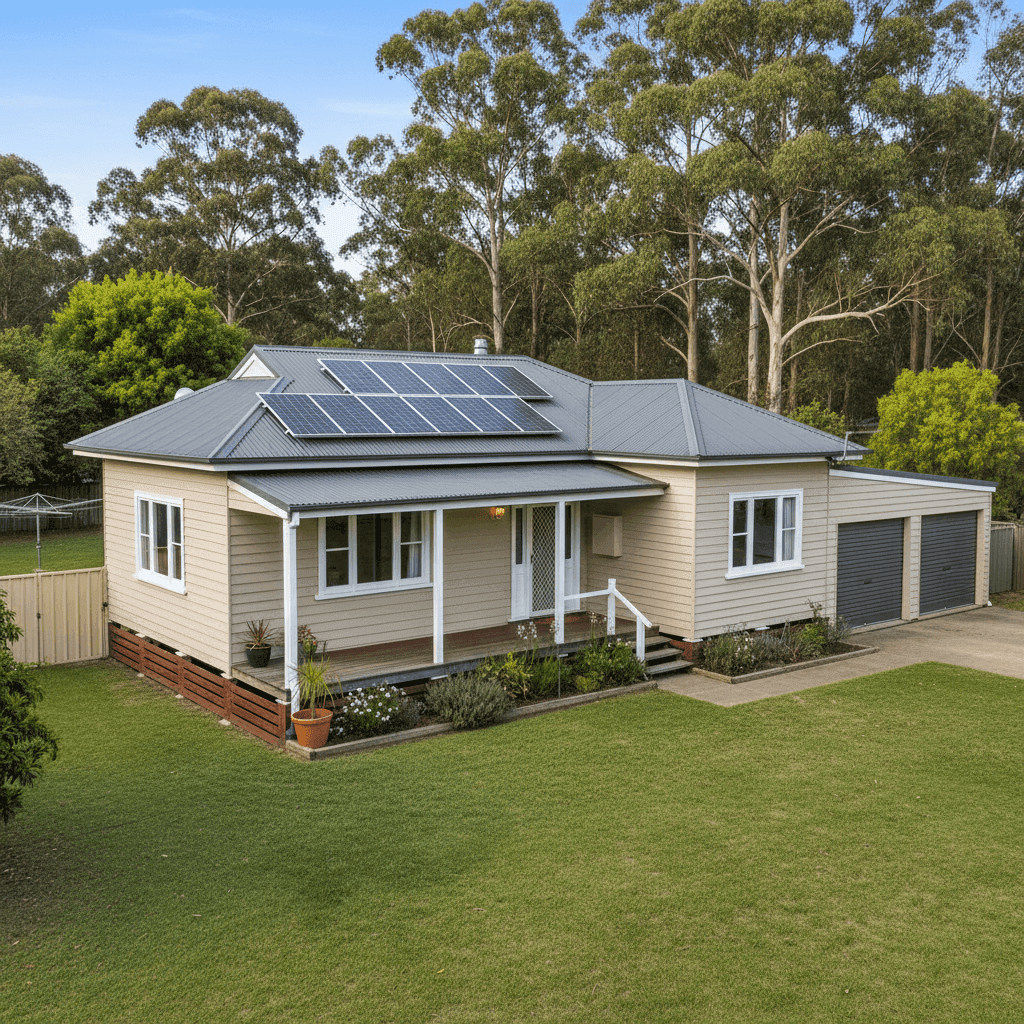

If you own a free standing home in Nemingha, NSW 2340, you're likely no stranger to the challenge of finding home insurance that offers genuine value. Nestled on the outskirts of Tamworth in the Liverpool Plains local government area, Nemingha is a semi-rural suburb where property characteristics — from older construction styles to the surrounding landscape — can play a significant role in shaping your insurance premium. This article breaks down a recent home and contents insurance quote for a 4-bedroom, 2-bathroom weatherboard home in the area, and puts it into context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: yes, and then some. The annual premium for this quote comes in at $3,481 per year (or $334 per month), covering a building sum insured of $600,000 and $100,000 worth of contents — with a $1,000 excess on each. Our pricing analysis rates this quote as CHEAP, meaning it sits comfortably below the average for comparable policies.

To put that in perspective, the NSW state average premium sits at a hefty $9,528 per year, with a state median of $3,770. Nationally, the average premium across Australia is $5,347, with a median of $2,764. At $3,481, this quote lands well below the NSW average and very close to the state median — a strong result for a property of this size and age.

For a 214 sqm home built in 1960, this pricing is particularly encouraging. Older homes often attract higher premiums due to the increased cost of sourcing period-appropriate materials and the greater likelihood of wear-related claims. The fact that this quote undercuts the state average by more than $6,000 per year is a meaningful outcome for the homeowner.

---

How Nemingha Compares

Suburb-level data for Nemingha isn't yet available in our database, but we can draw useful comparisons from the broader regional picture. Here's how the numbers stack up:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $3,481 |

| LGA (Liverpool Plains) Average | $2,851 |

| NSW State Median | $3,770 |

| NSW State Average | $9,528 |

| National Median | $2,764 |

| National Average | $5,347 |

The Liverpool Plains LGA average of $2,851 is the most locally relevant comparison point. This quote sits about $630 above that LGA average, which is understandable given the larger-than-typical building size (214 sqm) and the higher sum insured of $600,000. When you account for the level of cover on offer, the pricing remains competitive.

You can explore more data for this postcode at our Nemingha suburb stats page, and compare it against the national picture as more local data becomes available.

---

Property Features That Affect Your Premium

Every home is different, and insurers weigh up a range of property characteristics when calculating your premium. Here's how the specific features of this Nemingha home are likely influencing the cost:

Weatherboard Timber Walls

Weatherboard construction is common in older Australian homes and carries a higher fire risk than brick or rendered masonry. Timber walls are also more susceptible to moisture damage and pest ingress over time. Insurers typically factor this in, which can push premiums upward — making the below-average quote here even more impressive.

Steel / Colorbond Roof

On the positive side, a Colorbond steel roof is viewed favourably by insurers. It's durable, low-maintenance, and performs well in hail and wind events — all relevant considerations in regional NSW. This likely helps offset some of the risk associated with the timber wall construction.

Stump Foundation

Homes built on stumps (common in older Australian builds) can be more vulnerable to subsidence, flooding beneath the floor, and pest damage. This foundation type may contribute a modest loading to the premium, though it also allows for better airflow and easier access for inspections and repairs.

Timber and Laminate Flooring

Timber flooring adds replacement value to a contents and building claim but is generally not a major premium driver on its own. It does, however, contribute to the overall rebuild cost estimate, which is reflected in the $600,000 sum insured.

Solar Panels

This property includes solar panels, which are increasingly common across regional NSW. Solar systems add to the insured value of the home and can complicate roof-related claims. Most modern policies cover solar panels as part of the building, but it's worth confirming this with your insurer.

Ducted Climate Control

Ducted air conditioning systems represent a significant asset — both in terms of replacement cost and the potential for water or electrical damage claims. Including this in your building sum insured is important and is likely already factored into the $600,000 cover level here.

Construction Era (1960)

A home built in 1960 is over 60 years old. While well-maintained period homes can be structurally sound, older properties often require specialist trades and materials to restore them to their original condition following a claim. This can make rebuilds more expensive, which is why an accurate sum insured is especially critical for homes of this vintage.

---

Tips for Homeowners in Nemingha

Whether you're reviewing an existing policy or shopping around for the first time, here are four practical steps to make sure you're getting the best deal on your home insurance.

- Check your sum insured annually. Building costs have risen significantly across regional NSW in recent years. A sum insured set a few years ago may no longer be sufficient to cover a full rebuild. Use a building cost calculator or speak with a local builder to get an updated estimate.

- Maintain your weatherboard exterior. Regular painting and sealing of timber cladding not only preserves the home's value but can also demonstrate to insurers that the property is well-maintained — potentially supporting a more competitive premium at renewal.

- Confirm solar panel coverage. Ask your insurer explicitly whether your solar system is covered under the building policy, and whether that includes inverters and mounting hardware. Some policies treat solar panels as a separate item requiring additional cover.

- Compare quotes before renewing. Loyalty doesn't always pay in the insurance world. Premiums can vary dramatically between providers for the same level of cover. Running a comparison before your renewal date takes only a few minutes and could save you hundreds — or even thousands — of dollars each year.

---

Ready to Compare?

Whether this quote is your current policy or one you're considering, it's always worth seeing what else is on the market. At CoverClub, we make it easy to compare home and contents insurance quotes from a range of Australian insurers — so you can be confident you're not paying more than you need to. Get a quote today and see how your premium stacks up.