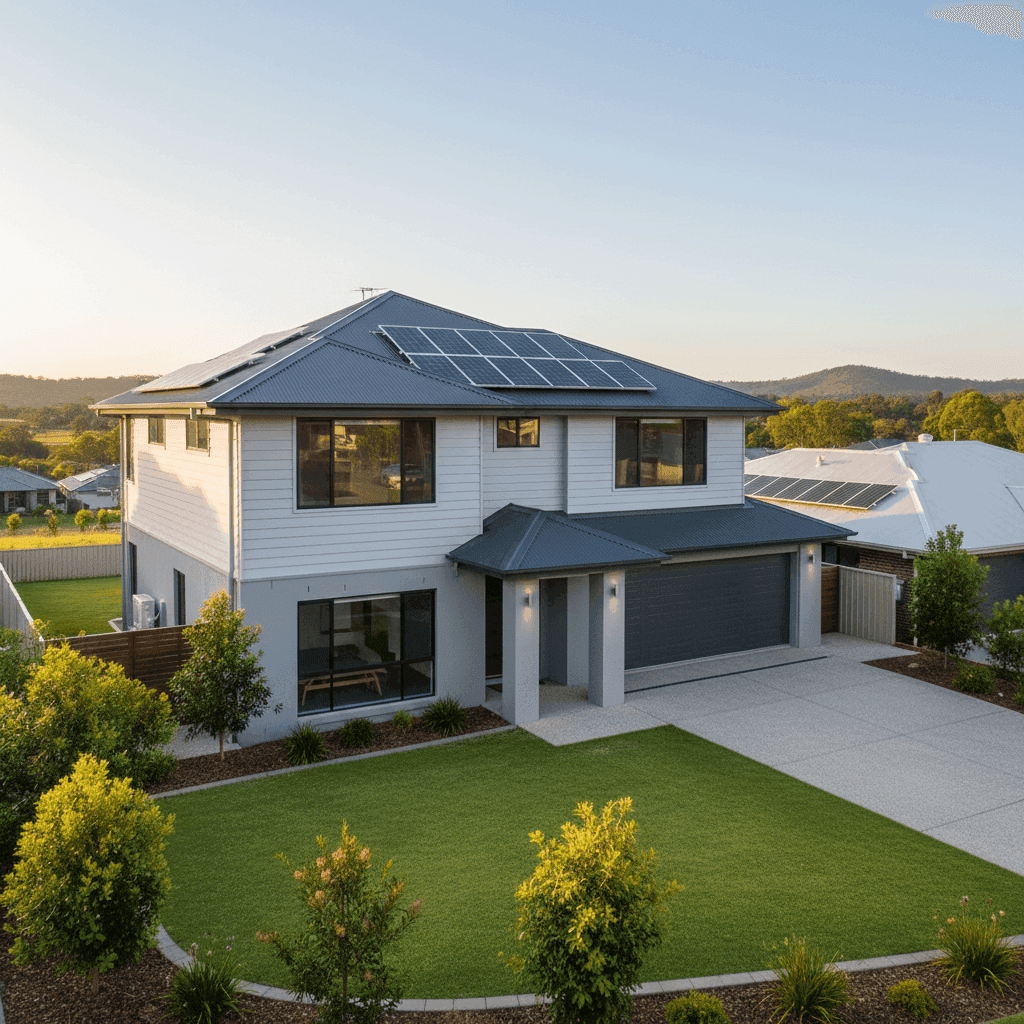

New Beith is a leafy, semi-rural suburb in the City of Ipswich, sitting about 40 kilometres south-west of Brisbane's CBD. It's a popular choice for families seeking larger blocks, newer builds, and a quieter lifestyle without straying too far from urban conveniences. For a five-bedroom, three-bathroom free-standing home built in 2021, we've analysed a recent home and contents insurance quote to help you understand whether the price stacks up — and what's driving it.

---

Is This Quote Fair?

The annual premium for this property came in at $2,838 per year (or roughly $283 per month), covering both building (sum insured: $1,000,000) and contents ($50,000). Our pricing model rates this as CHEAP — below average for the area.

To put that in perspective:

- The suburb average for New Beith (QLD 4124) sits at $4,451/yr, based on 47 quotes in our dataset.

- The suburb median is $4,024/yr, meaning this quote comes in nearly $1,200 below the midpoint.

- Even at the 25th percentile — the cheapest quarter of quotes in the suburb — the benchmark is $3,055/yr. This quote beats that comfortably.

In short, this is a genuinely competitive result. Homeowners paying close to the suburb average could potentially save over $1,600 per year by shopping around for a similar level of cover.

---

How New Beith Compares

Zooming out beyond the suburb paints an interesting picture. You can explore full pricing data on the New Beith suburb stats page, the Queensland state overview, or the national home insurance stats.

| Benchmark | Annual Premium |

|---|---|

| This quote | $2,838 |

| New Beith suburb average | $4,451 |

| New Beith suburb median | $4,024 |

| Ipswich LGA average | $8,901 |

| QLD state average | $9,129 |

| QLD state median | $3,903 |

| National average | $5,347 |

| National median | $2,764 |

A few things stand out here. Queensland's state average of $9,129/yr is dramatically higher than the national average — a reflection of the state's significant exposure to extreme weather events, including flooding, cyclones, and severe storms. However, the QLD median of $3,903/yr tells a more nuanced story: a relatively small number of very high-risk properties (particularly in flood-prone or cyclone-affected areas) are pulling that average upward.

New Beith's suburb average of $4,451/yr sits above both the state and national medians, which suggests the area carries a moderate-to-elevated risk profile compared to many parts of Australia. The Ipswich LGA average of $8,901/yr is particularly striking — likely influenced by flood-prone suburbs closer to the Bremer River and Brisbane River catchments. New Beith itself sits at higher elevation than many parts of Ipswich, which may partly explain why this particular quote came in well below the LGA average.

Compared to the national median of $2,764/yr, this quote is only marginally higher — a strong outcome for a property of this size and value in Queensland.

---

Property Features That Affect Your Premium

Several characteristics of this property work in its favour from an insurance pricing perspective.

Modern construction (2021): Newer homes typically attract lower premiums. A 2021 build means the property was constructed to current Australian building codes, which incorporate improved structural standards, fire resistance, and weather resilience. Insurers generally view newer homes as lower risk than older stock.

Hardiplank/Hardiflex cladding: This fibre cement cladding is widely regarded as a durable, low-maintenance external wall material. It offers solid resistance to fire, moisture, and impact — all factors that insurers assess when calculating risk. Compared to weatherboard or older brick veneer, Hardiflex is generally well regarded.

Steel/Colorbond roof: Colorbond roofing is a staple of modern Australian construction for good reason. It's lightweight, corrosion-resistant, and performs well in high-wind events. From an insurance standpoint, it's considered a favourable roofing material compared to terracotta tiles, which can dislodge more easily in storms.

Concrete slab foundation: Slab foundations are structurally sound and less susceptible to subsidence or pest-related damage than raised timber stumps. This is a positive risk factor.

Solar panels: The presence of rooftop solar panels adds some complexity to insurance. Solar systems have value and can be damaged in hail or storm events, so it's worth confirming with your insurer whether the panels are covered under the building policy or require a separate endorsement.

Ducted climate control: Ducted HVAC systems are a higher-cost fixture that contributes to the overall replacement value of the home. Ensuring your sum insured accurately reflects the cost to replace these systems is important.

No pool, no cyclone risk zone: The absence of a pool removes a common liability and maintenance risk factor. Being outside a designated cyclone risk area also keeps premiums lower than properties in North Queensland or coastal Far North QLD.

Standard fittings: The standard (rather than premium) fittings quality means the internal fit-out doesn't dramatically inflate the rebuild cost, which helps keep the sum insured — and therefore the premium — reasonable.

---

Tips for Homeowners in New Beith

1. Review your sum insured regularly A $1,000,000 building sum insured is substantial, but construction costs have risen sharply in recent years. It's worth using a building cost calculator or consulting a quantity surveyor periodically to ensure your cover keeps pace with actual rebuild costs. Being underinsured at claim time can be a costly mistake.

2. Confirm solar panel coverage Solar panels are a significant asset and can be expensive to repair or replace after a hail event or storm. Check your policy's product disclosure statement (PDS) to confirm whether they're automatically included under the building cover or need to be specifically listed.

3. Consider your excess carefully This quote carries a $4,000 building excess and a $2,000 contents excess. Higher excesses are one of the key levers insurers use to reduce premiums. Before accepting a high excess, make sure you're comfortable covering that amount out of pocket in the event of a claim — particularly for contents, where individual item values may not always justify the cost.

4. Shop around at renewal time Insurance premiums can shift significantly year to year, and loyalty doesn't always pay. Using a comparison platform like CoverClub at renewal time takes only a few minutes and can surface meaningfully cheaper options — as this quote demonstrates, there's often a wide spread between the cheapest and most expensive quotes for the same property.

---

Ready to Compare Your Own Quote?

Whether you're buying, renewing, or just curious about whether you're paying too much, CoverClub makes it easy to compare home and contents insurance quotes across Australia's leading insurers. Get a personalised quote today and see how your premium stacks up against your neighbours.