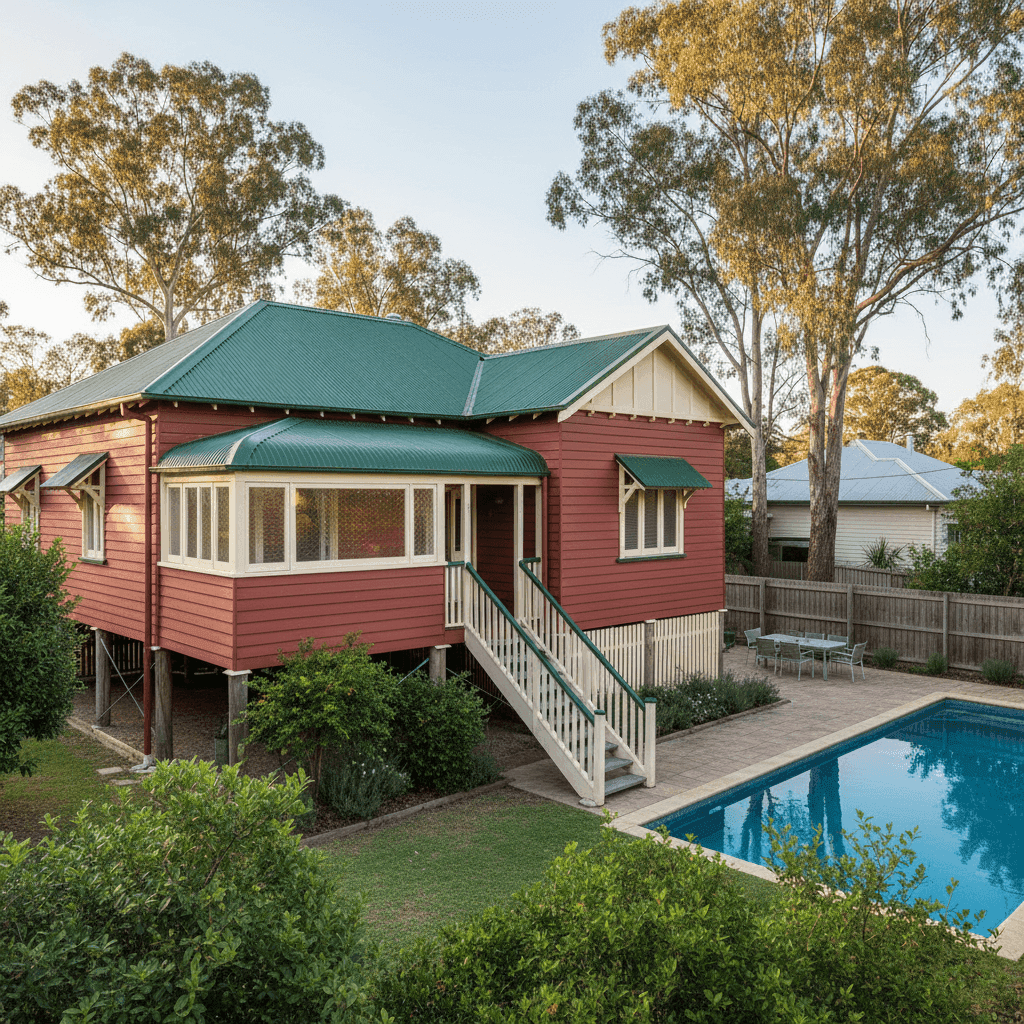

Nestled in the inner suburbs of Newcastle, New Lambton (NSW 2305) is a sought-after neighbourhood known for its leafy streets, federation-era homes, and strong community feel. This analysis looks at a home and contents insurance quote for a 3-bedroom, 3-bathroom free-standing home in the area — a character-filled weatherboard property built in 1910, sitting on stumps with a Colorbond roof, timber flooring, and a backyard pool. The annual premium came in at $5,681, or roughly $544 per month. So, is that a fair price? Let's dig in.

---

Is This Quote Fair?

Based on our pricing data, this quote has been rated Expensive (Above Average) for the New Lambton area.

At $5,681 per year, this premium sits above the suburb average of $4,639 and well above the suburb median of $3,764. It also exceeds the 75th percentile for the suburb ($5,583), meaning it's pricier than roughly three-quarters of comparable quotes we've seen in postcode 2305.

That said, context matters. The national average home and contents premium sits at $5,347/yr, so this quote is only modestly above what Australians are paying on average across the country. And when you consider the NSW state average of $9,528/yr — heavily skewed by high-risk and high-value properties — this quote is actually quite reasonable in a broader sense.

The $925,000 building sum insured is a significant factor here. This is a substantial rebuild value, particularly for a 235 sqm home with period features, and insurers price accordingly. Add in a $50,000 contents value, a swimming pool, and the age and construction style of the property, and the premium starts to make more sense — even if it's on the higher end locally.

The $2,000 excess on both building and contents is on the higher side, which would normally push premiums down. The fact the premium is still above average despite this suggests the property's risk profile is carrying real weight in the insurer's calculations.

---

How New Lambton Compares

Here's a snapshot of how this quote stacks up across different benchmarks:

| Benchmark | Annual Premium |

|---|---|

| This Quote | $5,681 |

| New Lambton Suburb Average | $4,639 |

| New Lambton Suburb Median | $3,764 |

| New Lambton 25th Percentile | $3,113 |

| New Lambton 75th Percentile | $5,583 |

| NSW State Average | $9,528 |

| NSW State Median | $3,770 |

| National Average | $5,347 |

| National Median | $2,764 |

| Lake Macquarie LGA Average | $11,064 |

It's worth noting that the Lake Macquarie LGA average of $11,064 is remarkably high — likely driven by properties in flood-prone or coastal pockets of the LGA where risk profiles are significantly elevated. New Lambton, sitting further inland and on higher ground, generally fares better than many parts of the LGA.

You can explore more localised pricing data on the New Lambton suburb stats page, compare it against NSW state-wide insurance trends, or take a look at national home insurance benchmarks for a broader picture.

---

Property Features That Affect Your Premium

Several characteristics of this property have a meaningful influence on what insurers charge:

🏚️ Age & Construction (Built 1910, Weatherboard Walls)

A home built in 1910 is well over a century old. While these federation-era homes are charming and often structurally sound, insurers view older properties as higher risk — plumbing, wiring, and structural elements may not meet modern standards. Weatherboard timber cladding is also considered more susceptible to fire, rot, and pest damage compared to brick veneer or full brick construction, which typically attracts a loading on premiums.

🏗️ Stump Foundation & Elevated Position

This home sits on stumps and is elevated by less than 1 metre. Stump foundations are common in older NSW and Queensland-style homes and can be a double-edged sword for insurance: they allow for good subfloor ventilation and can reduce flood impact, but they also introduce risks around subfloor access, pest intrusion, and structural movement over time.

🏊 Swimming Pool

Having a pool on the property adds to the insurer's liability exposure. Pool-related incidents — from structural damage to third-party injuries — are factored into the premium calculation.

❄️ Ducted Climate Control

The presence of ducted climate control is a sign of higher-value fittings and systems within the home. This contributes to a higher rebuild cost estimate, which in turn supports the $925,000 sum insured.

🌀 No Cyclone Risk

New Lambton is not in a designated cyclone risk zone, which is a positive for premiums. Properties in northern Queensland or parts of WA can face significant cyclone loadings — this property avoids that entirely.

🌊 Not in a High-Flood Zone

While parts of the Lake Macquarie LGA are flood-affected, New Lambton's elevation and geography generally place it at lower flood risk than many nearby suburbs — another factor that keeps this premium from being even higher.

---

Tips for Homeowners in New Lambton

If you're a homeowner in New Lambton looking to get better value from your home insurance, here are some practical steps worth taking:

1. Review Your Sum Insured Regularly

Building costs have risen sharply in recent years. Make sure your $925,000 sum insured genuinely reflects what it would cost to rebuild your home today — not just its market value. Underinsurance is a serious risk, but over-insuring can also mean you're paying more than necessary. Use a building cost calculator or speak to a local builder to get a realistic estimate.

2. Consider a Higher Excess — Carefully

This policy already carries a $2,000 excess, which is relatively high. Going higher could reduce your premium further, but only makes sense if you're confident you could cover that cost out of pocket in an emergency. Weigh the annual savings against the financial exposure.

3. Maintain Your Weatherboard Home Proactively

Insurers love well-maintained properties. Keeping your weatherboard cladding painted, sealed, and free from rot or pest damage can reduce the likelihood of a claim — and may support a better premium at renewal. Document your maintenance with photos and receipts.

4. Shop Around at Renewal Time

Loyalty doesn't always pay in insurance. The fact that this quote sits above the suburb median suggests there may be better-priced options available for the same level of cover. Use a comparison tool like CoverClub to benchmark your renewal quote against the market before you sign on for another year.

---

Compare Your Quote with CoverClub

Whether you're reviewing an existing policy or shopping for the first time, CoverClub makes it easy to see how your premium stacks up. Our data covers thousands of quotes across Australia, giving you real, localised context — not just generic averages.

Ready to see what you could be paying? Get a home insurance quote comparison at CoverClub and find out if your premium is working as hard as it should be.