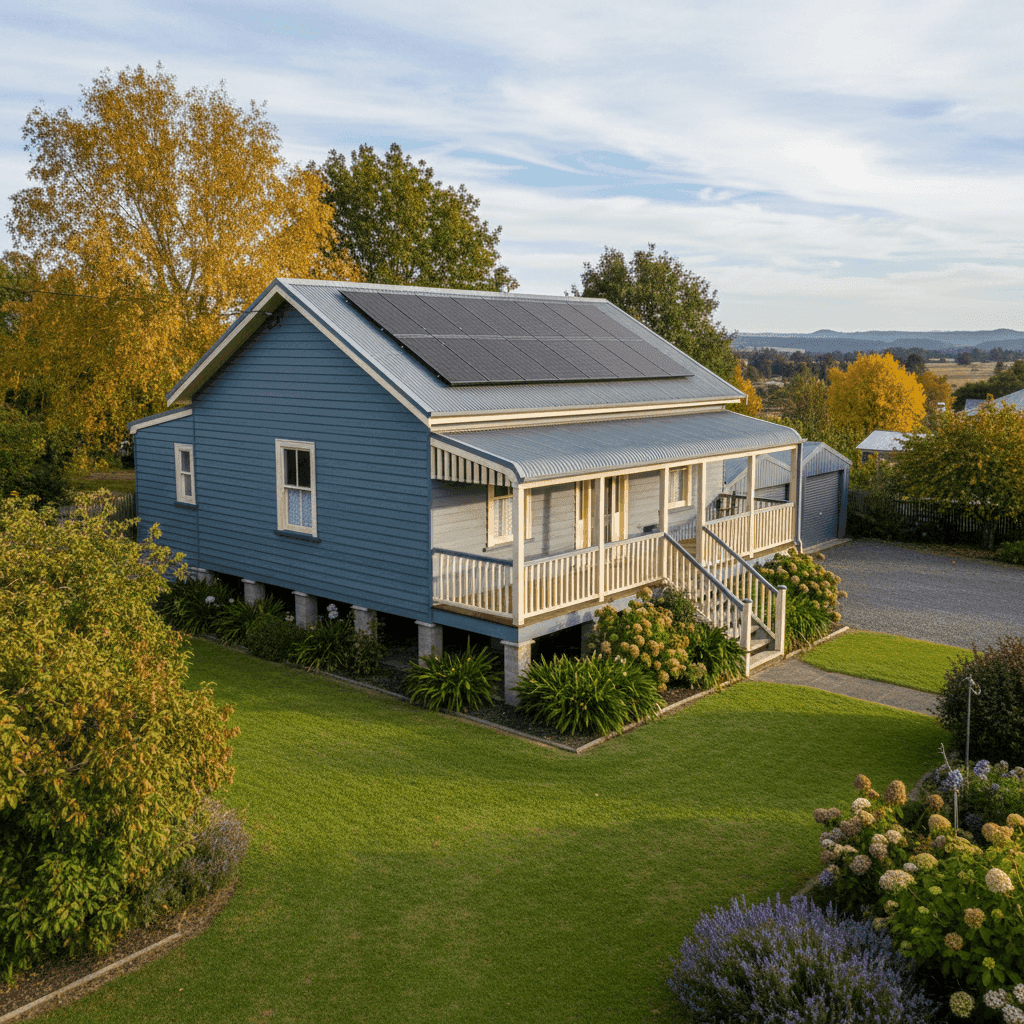

New Norfolk, nestled in the Derwent Valley about 38 kilometres north-west of Hobart, is one of Tasmania's oldest towns — and its housing stock reflects that rich history. This analysis looks at a home and contents insurance quote for a four-bedroom, free-standing weatherboard home in New Norfolk (postcode 7140), built in 1925, with a building sum insured of $837,000 and contents cover of $128,000. The annual premium came in at $2,893 (or $283/month). So how does that stack up?

---

Is This Quote Fair?

The short answer: yes, broadly fair — though there's room to shop around.

This quote has been rated Fair (Around Average), which means it sits in a reasonable band relative to what other homeowners in the area are paying — but it's not the keenest price on the market. At $2,893 per year, it lands above Tasmania's state median of $2,272 and above the suburb median of $1,868, but comfortably below the national average of $2,965 and well below the New Norfolk suburb average of $4,654.

The wide spread of premiums in this suburb — from $1,274 at the 25th percentile all the way to $5,890 at the 75th percentile — tells you something important: insurers price New Norfolk properties very differently. That kind of variability is a strong signal that comparing multiple quotes could meaningfully reduce what you pay.

For a property of this age, size, and construction type, a premium in the $2,893 range isn't surprising. But it's also not a done deal. Depending on your insurer and the specifics of your policy, you may be able to do better.

---

How New Norfolk Compares

Here's a snapshot of where this quote sits across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $2,893/yr |

| New Norfolk Suburb Average | $4,654/yr |

| New Norfolk Suburb Median | $1,868/yr |

| New Norfolk 25th Percentile | $1,274/yr |

| New Norfolk 75th Percentile | $5,890/yr |

| TAS State Average | $2,458/yr |

| TAS State Median | $2,272/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

| West Coast LGA Average | $3,729/yr |

(Based on a sample of 45 quotes in the New Norfolk area. View full [New Norfolk suburb insurance stats](https://coverclub.com.au/stats/TAS/7140/new-norfolk), [TAS state stats](https://coverclub.com.au/stats/TAS), and [national stats](https://coverclub.com.au/stats/national).)

A few things stand out. The suburb average ($4,654) is dramatically higher than the median ($1,868) — a classic sign that a handful of very expensive quotes are skewing the average upward. This quote at $2,893 sits between those two figures, which is a reasonable outcome.

Compared to the broader Tasmanian state average of $2,458, this quote is about $435 higher per year. Against the national average of $2,965, it's actually slightly cheaper — a modest win for a property that carries several risk factors worth noting.

---

Property Features That Affect Your Premium

Several characteristics of this property have a direct bearing on what insurers charge:

Age of construction (1925). At over 100 years old, this home is considered heritage-era stock. Older homes can be more expensive to repair or rebuild due to non-standard materials, craftsmanship requirements, and the likelihood of hidden issues within walls and subfloors. Insurers factor this in when calculating risk.

Weatherboard timber walls. Weatherboard is a classic Australian external cladding — but from an insurance perspective, timber is more susceptible to fire, rot, and pest damage than brick or rendered masonry. This typically pushes premiums higher compared to brick-veneer equivalents.

Stump foundation. The home sits on stumps, which is common in older Tasmanian properties. While stumps allow for good underfloor ventilation, they can be vulnerable to movement, rot, and pest activity over time. Insurers may view this as a moderate structural risk factor.

Timber and laminate flooring. Like the walls, timber flooring adds to the overall combustibility profile of the home and can be costly to replace or match in the event of damage.

Steel/Colorbond roof. This is actually a positive from an insurance standpoint. Colorbond roofs are durable, fire-resistant, and low-maintenance — a factor that can help moderate premiums relative to older tile or iron roofing.

Solar panels. The presence of solar panels adds value to the property and increases the cost of reinstatement if the roof is damaged. Some insurers automatically include panels under building cover; others require them to be specifically noted. It's worth confirming your policy covers them.

Building size (226 sqm). At 226 square metres, this is a generously sized home. A higher floor area generally means a higher rebuild cost, which is reflected in the $837,000 sum insured and, in turn, the premium.

No pool, no ducted climate control, not in a cyclone zone. Each of these absences works in the homeowner's favour — pools and ducted systems add complexity and cost to claims, while cyclone-zone properties attract significant loading in northern Australia. New Norfolk has none of these concerns.

---

Tips for Homeowners in New Norfolk

1. Get multiple quotes — the spread is wide. With a 25th-to-75th percentile range of $1,274 to $5,890 in this suburb, the difference between a cheap and expensive policy can be enormous. Don't settle for the first quote you receive. Use a comparison tool like CoverClub to see what multiple insurers would charge for the same property.

2. Review your sum insured carefully. At $837,000, the building sum insured needs to reflect the full cost of rebuilding — not the market value of the home. For a heritage-era weatherboard property of this size, rebuild costs can be significant. Underinsurance is a common and costly mistake; consider using a professional building calculator or speaking to a quantity surveyor if you're unsure.

3. Confirm solar panels are explicitly covered. Solar panel systems can represent a substantial investment. Check your policy wording to ensure panels are included under building cover and that the sum insured accounts for their replacement value. Some policies cover them as standard; others treat them as an optional extra.

4. Ask about discounts for security and maintenance. Some insurers offer premium reductions for homes with monitored alarms, deadbolts, or smoke detectors. Keeping up with maintenance on stumps, weatherboards, and gutters can also reduce the likelihood of a claim — and in some cases, demonstrating good upkeep can support negotiations with your insurer at renewal.

---

Compare Your Options with CoverClub

Whether you're buying a new policy or reviewing your current one at renewal, it pays to compare. CoverClub makes it easy to see how your home insurance quote stacks up against real data from your suburb, state, and across Australia. Get a quote today and find out if you're getting a fair deal — or if there's a better one waiting.