If you own a free standing home in Nichols Point, VIC 3501, you've probably wondered whether you're paying too much — or too little — for home insurance. This article breaks down a real home and contents insurance quote for a three-bedroom brick veneer property in the suburb, comparing it against local, state, and national benchmarks to help you understand what's driving the price.

---

Is This Quote Fair?

The annual premium for this property came in at $2,122 per year (or roughly $203 per month), covering both building (insured at $694,000) and contents ($50,000), each with a $1,000 excess.

Our price rating for this quote is CHEAP — below average for the area. That's a meaningful finding. Based on suburb-level data for Nichols Point, the average premium across 18 quotes is $3,288 per year, and the median sits at $3,201. This quote lands well below the 25th percentile of $2,531 — meaning it's cheaper than at least three-quarters of comparable quotes in the suburb.

For homeowners, this is genuinely good news. A premium this far below the local average suggests the insurer has assessed this particular property's risk profile favourably. That said, "cheap" doesn't automatically mean "best" — it's worth confirming the policy provides adequate cover for your needs, especially given the building sum insured of $694,000 for a 214 sqm home.

---

How Nichols Point Compares

To put this quote in proper context, here's how Nichols Point stacks up against broader benchmarks:

| Benchmark | Average Premium | Median Premium |

|---|---|---|

| Nichols Point (suburb) | $3,288/yr | $3,201/yr |

| Swan Hill LGA | $2,484/yr | — |

| Victoria (state) | $3,000/yr | $2,718/yr |

| Australia (national) | $5,347/yr | $2,764/yr |

A few things stand out here. First, the Swan Hill LGA average of $2,484 is notably lower than the Nichols Point suburb average of $3,288 — suggesting that premiums within the 3501 postcode may be influenced by localised risk factors such as flood proximity to the Murray River or specific property characteristics in the area.

Second, while Victoria's average of $3,000 per year is broadly in line with the suburb median, the national average of $5,347 is dramatically higher — largely driven by elevated premiums in cyclone-prone regions of Queensland and Western Australia, as well as high-value coastal properties. Nichols Point homeowners are, by comparison, operating in a relatively affordable insurance environment.

This quote at $2,122 sits 35% below the suburb average and 29% below the Victorian average — a strong result by any measure.

---

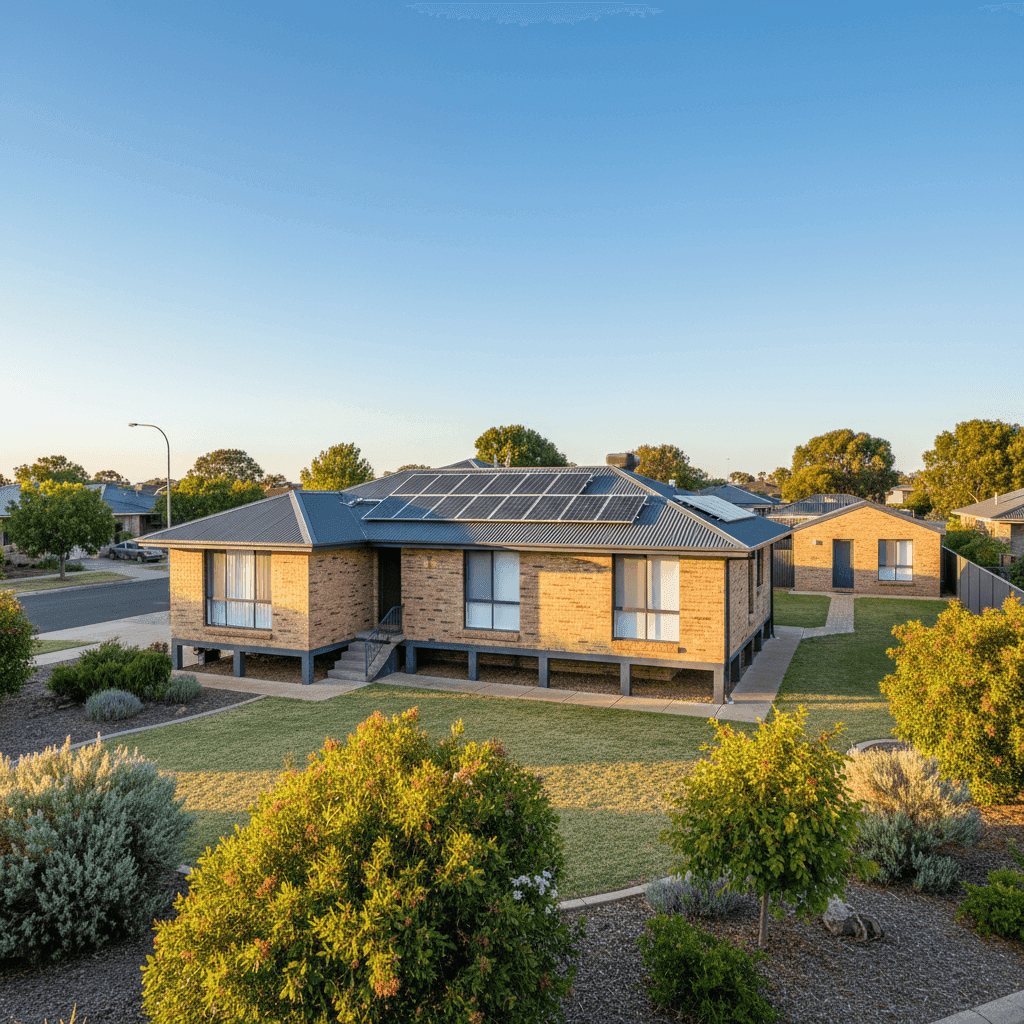

Property Features That Affect Your Premium

Several characteristics of this property are likely contributing to its competitive premium:

Brick Veneer Walls & Colorbond Roof Brick veneer construction is widely regarded by insurers as a resilient and fire-resistant building material. Combined with a steel Colorbond roof — which is durable, low-maintenance, and resistant to ember attack — this combination typically attracts more favourable underwriting terms than, say, weatherboard or fibrous cement cladding.

Slab Foundation A concrete slab foundation is generally considered a stable and lower-risk base compared to raised stumped or pier foundations, which can be more susceptible to movement, moisture ingress, and pest damage over time.

1990 Construction At around 35 years old, this home sits in a sweet spot for insurers. It's old enough that any construction defects would have long since surfaced, but modern enough to have been built under reasonably contemporary building codes. Homes from this era tend to attract standard (rather than loaded) premiums.

Solar Panels The presence of solar panels adds some replacement value to the building sum insured, but it's a relatively common feature now and doesn't typically inflate premiums significantly. It's worth confirming with your insurer that panels are explicitly covered under the building policy.

Granny Flat A granny flat on the property is an important factor to flag with your insurer. Depending on the policy, a secondary dwelling may or may not be automatically included in the building sum insured. Homeowners should verify whether the granny flat's rebuild cost is captured within the $694,000 building cover — if not, you may be underinsured.

Ducted Climate Control Ducted air conditioning systems are a fixed building fixture and should be included in the building sum insured. Given the hot summers typical of the Sunraysia region, this is a meaningful asset worth confirming is covered.

No Cyclone Risk Nichols Point is not in a designated cyclone risk zone, which removes one of the most significant premium loading factors seen in northern Australia. This contributes to the comparatively affordable pricing in the region.

---

Tips for Homeowners in Nichols Point

1. Double-check your granny flat is covered Secondary dwellings are a common source of underinsurance. Contact your insurer to confirm whether the granny flat is included in your building sum insured or whether it requires a separate policy or endorsement.

2. Review your building sum insured annually Construction costs have risen sharply in recent years across regional Victoria. A $694,000 sum insured for a 214 sqm home is approximately $3,243 per square metre — reasonable, but worth validating against current local rebuild cost estimates, particularly given the ducted systems, solar panels, and granny flat on the property.

3. Protect against flood risk near the Murray Nichols Point sits close to the Murray River, and flood cover is not always included by default in standard home insurance policies. Check your Product Disclosure Statement carefully and, if flood cover is excluded or optional, consider whether it's appropriate given your property's location.

4. Compare at renewal, not just at purchase Even with a competitive premium today, insurers regularly adjust pricing at renewal. Set a reminder to compare quotes at CoverClub before your renewal date each year — loyalty doesn't always pay in the insurance market.

---

Get Your Own Quote

Whether you're a first-time buyer or a long-time Nichols Point homeowner, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes tailored to your property. Start your free comparison today and find out if you're getting a fair deal — or if there's a better option waiting for you.