Nimbin is one of New South Wales' most distinctive communities — a laid-back village nestled in the lush hinterland of the Northern Rivers region, roughly 30 kilometres north-west of Lismore. If you own a free standing home here, understanding how your building insurance premium stacks up against local and national benchmarks is an important step toward making sure you're getting genuine value. This article breaks down a recent quote of $2,133 per year for a 2-bedroom, 1-bathroom free standing home in Nimbin (postcode 2480), and puts it in context with suburb, state, and national data.

---

Is This Quote Fair?

The short answer: yes, broadly speaking. This quote has been rated Fair (Around Average) — meaning it sits in the middle of the road relative to what other homeowners in the area are paying, without being a standout bargain or an obvious overprice.

At $2,133 per year (or roughly $204 per month), this premium lands just above the suburb's 25th percentile of $2,093, which means it's only marginally more expensive than the cheapest quarter of quotes seen in the area. It sits comfortably below both the suburb average ($2,966) and the suburb median ($2,605), which is a reasonably encouraging sign.

That said, "fair" doesn't mean "the best available." There may still be room to sharpen the price by comparing across insurers — more on that below.

The building excess on this policy is $2,000, which is on the higher end of what's typical for Australian home insurance. A higher excess generally brings the premium down, so it's worth weighing whether you'd be comfortable covering that amount out of pocket in the event of a claim. The contents excess listed is $1,000, though this is a building-only policy, so contents cover would need to be arranged separately if required.

---

How Nimbin Compares

To truly appreciate what $2,133 per year means, it helps to zoom out and look at the broader pricing landscape.

| Benchmark | Premium |

|---|---|

| This quote | $2,133/yr |

| Nimbin suburb average | $2,966/yr |

| Nimbin suburb median | $2,605/yr |

| NSW average | $9,528/yr |

| NSW median | $3,770/yr |

| National average | $5,347/yr |

| National median | $2,764/yr |

| Ballina LGA average | $23,241/yr |

A few things stand out here. First, the NSW state average of $9,528 is extraordinarily high — driven in large part by coastal and flood-prone areas, as well as the catastrophic insurance losses recorded across the Northern Rivers in recent years. The national average of $5,347 tells a similar story of elevated premiums across the country.

What's particularly striking is the Ballina LGA average of $23,241 per year — one of the highest in the country, reflecting the severe flood risk that devastated much of the Northern Rivers in 2022. Nimbin, while technically within the broader Northern Rivers region, sits at higher elevation and has a different risk profile to the lowland areas around Ballina and Lismore. This likely explains why Nimbin suburb premiums are considerably lower than the LGA average.

At $2,133, this quote is well below the NSW median, the national average, and the national median — a meaningful result for a region that has experienced significant insurance pressure in recent years.

---

Property Features That Affect Your Premium

Several characteristics of this property play a role in shaping the premium, for better or worse.

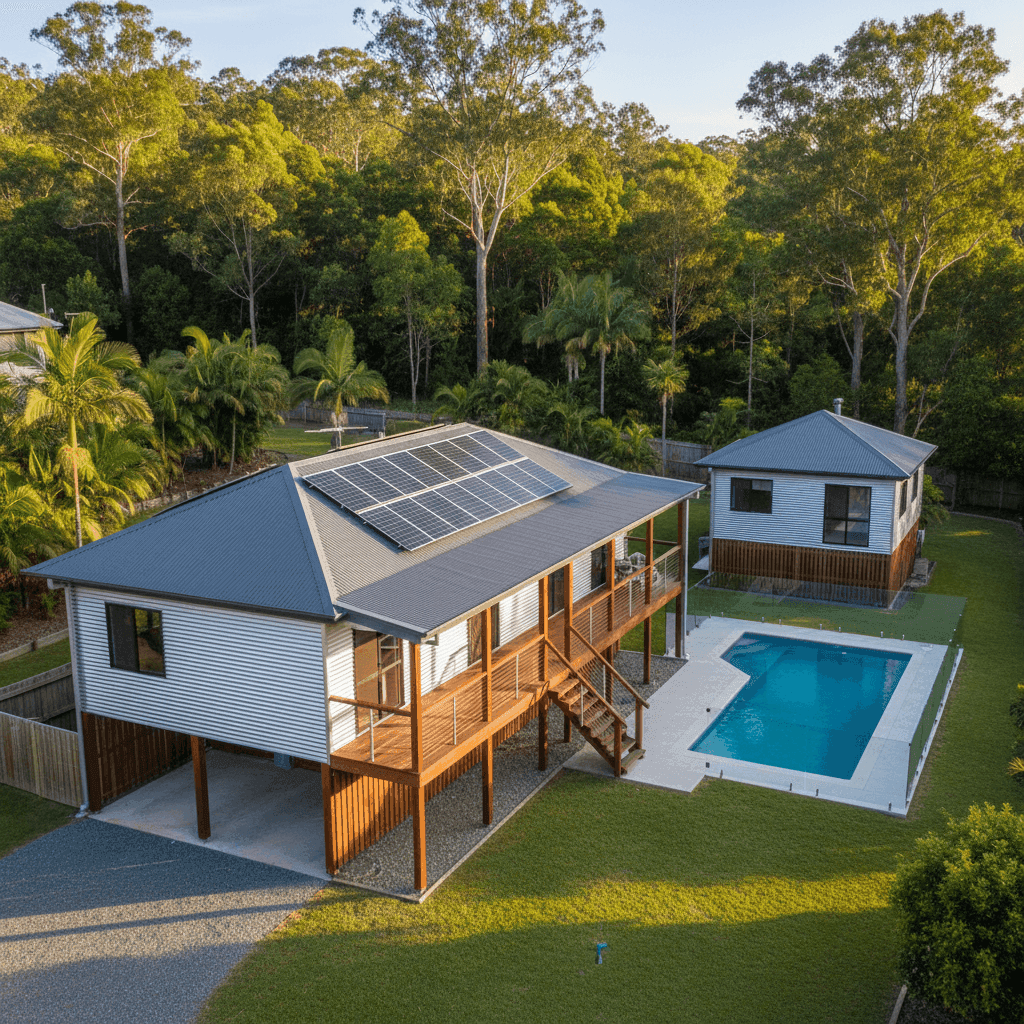

Elevated foundation on stumps — The home is raised by at least one metre on stumps, which is a classic construction style in the Northern Rivers hinterland. Elevation can be a double-edged sword: it offers meaningful protection against surface flooding and moisture ingress, which insurers generally view favourably. However, elevated homes can also be more exposed to wind and storm damage, which may offset some of the benefit.

Aluminium cladding and Colorbond roof — These are both durable, low-maintenance materials. Colorbond steel roofing in particular is well-regarded by insurers for its resistance to fire, wind, and corrosion. Aluminium cladding is similarly resilient and non-combustible, which is a positive factor in a region where bushfire risk (while not extreme for Nimbin) is still a consideration.

Timber and laminate flooring — Timber floors add to the rebuild cost and can be more susceptible to water damage than tiles. This is worth keeping in mind when reviewing your sum insured.

Swimming pool — A pool increases the overall replacement value of the property and adds liability considerations. It's important to ensure your sum insured of $500,000 adequately accounts for the pool structure and surrounds.

Solar panels — Solar systems are increasingly common in Nimbin, and most standard building policies will cover roof-mounted panels as part of the building structure. It's worth confirming this is explicitly included in your policy wording.

Granny flat — The presence of a secondary dwelling on the property adds complexity. Some policies automatically cover a granny flat under the main building sum insured, while others treat it as a separate structure. Confirm with your insurer exactly how this is handled.

Ducted climate control — Ducted systems are considered a fixed building feature and should be included in your building sum insured. Given the cost of replacing these systems, it's worth ensuring the $500,000 sum insured reflects this.

---

Tips for Homeowners in Nimbin

1. Review your sum insured carefully A $500,000 building sum insured for a 105 sqm home with a pool, solar panels, granny flat, and ducted climate control needs to be scrutinised. Construction costs in regional NSW have risen sharply since 2022. Use a building cost calculator or speak to a quantity surveyor to confirm your sum insured is adequate — being underinsured at claim time can be a costly mistake.

2. Clarify granny flat and secondary structure cover Not all policies treat secondary dwellings the same way. Before renewing or switching, ask your insurer specifically whether the granny flat is covered under your building policy and whether the sum insured is sufficient to cover both structures.

3. Compare quotes annually The insurance market in NSW has been volatile, particularly in the Northern Rivers. Premiums that were competitive last year may not be this year — and vice versa. Using a comparison platform like CoverClub at renewal time takes only a few minutes and can surface meaningfully cheaper options.

4. Consider your excess strategically The $2,000 building excess on this policy is relatively high. If you have the financial buffer to absorb a larger out-of-pocket cost in a claim, maintaining a high excess to keep premiums down can make sense. If not, it may be worth requesting quotes with a lower excess to understand the premium trade-off.

---

Find a Better Deal on CoverClub

Whether you're renewing your current policy or shopping for the first time, comparing quotes is the single most effective way to ensure you're not overpaying. CoverClub aggregates real insurance data from across Australia so you can see exactly how your premium measures up — and find better options when they exist.

Get a home insurance quote for your Nimbin property today and see how much you could save.