Ningi is a quiet residential suburb on Queensland's Sunshine Coast hinterland fringe, sitting within the Moreton Bay Region. It's a popular choice for families seeking larger blocks and spacious homes — and this six-bedroom, four-bathroom free-standing property is a prime example of what the area offers. But when it comes to insuring a home like this, the numbers can be surprising. This article breaks down a recent building insurance quote of $5,102 per year for this property and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The short answer: this quote is rated Expensive — sitting above average for the Ningi suburb.

At $5,102 per year (or $489 per month), this premium is notably higher than what most comparable properties in the area are paying. The suburb average sits at $2,770/yr, and the median is $2,826/yr, meaning this quote is roughly 84% above the local average. Even at the 75th percentile — meaning 75% of Ningi quotes are cheaper — premiums reach only $3,410/yr, still well below this figure.

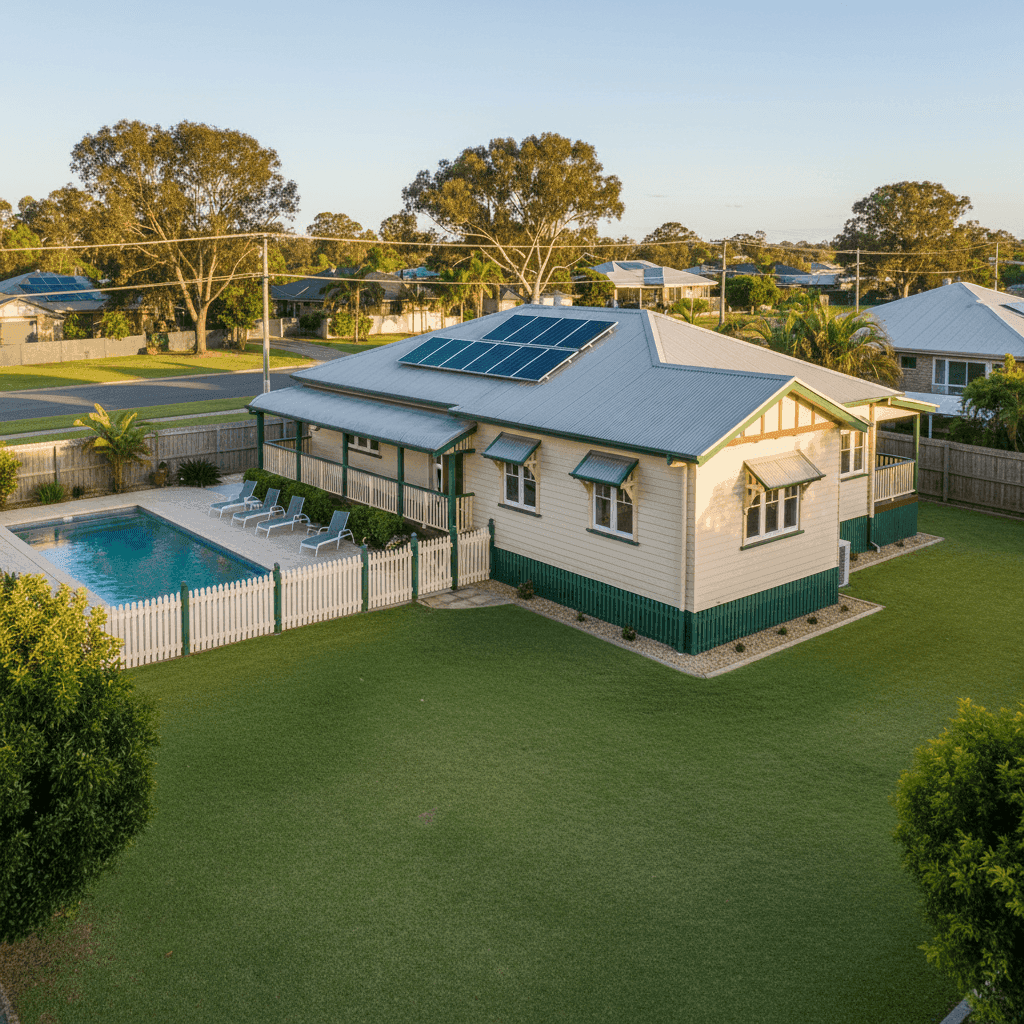

That said, context matters. This isn't a standard three-bedroom brick veneer. The property is a large, six-bedroom weatherboard home built in 1970, with a sum insured of $1,033,000 — a figure that reflects both the size and the cost to rebuild. The building excess is set at $2,000, which is on the higher end and would typically help bring premiums down, making the overall cost even more noteworthy.

When zooming out to the Queensland state level, the picture shifts. The QLD average premium is a striking $9,129/yr, heavily skewed by high-risk coastal and cyclone-prone areas in Far North Queensland. Against that backdrop, $5,102 looks far more reasonable. Similarly, the national average sits at $5,347/yr, putting this quote just slightly below the Australian average — a meaningful reframe.

So while this quote is expensive for Ningi, it's broadly in line with what Australians are paying nationally, and well below the Queensland average.

---

How Ningi Compares

Here's a snapshot of how this quote stacks up across different benchmarks:

| Benchmark | Premium |

|---|---|

| This Quote | $5,102/yr |

| Ningi Suburb Average | $2,770/yr |

| Ningi Suburb Median | $2,826/yr |

| Ningi 25th Percentile | $2,084/yr |

| Ningi 75th Percentile | $3,410/yr |

| Moreton Bay LGA Average | $3,435/yr |

| QLD State Average | $9,129/yr |

| QLD State Median | $3,903/yr |

| National Average | $5,347/yr |

| National Median | $2,764/yr |

The Ningi suburb stats are based on a sample of 48 quotes, which provides a reasonable local comparison pool. It's worth noting that the suburb median ($2,826) and average ($2,770) are very close together, suggesting a fairly consistent pricing band locally — without the extreme outliers that can skew averages in other postcodes.

The Moreton Bay LGA average of $3,435/yr also sits well below this quote, reinforcing that the property's specific characteristics — rather than location risk alone — are the primary cost drivers here.

---

Property Features That Affect Your Premium

Several characteristics of this home directly influence the premium, and understanding them can help you make more informed decisions.

Weatherboard timber walls are one of the most significant factors. Older timber-framed homes are considered higher risk by insurers due to their susceptibility to fire, rot, and pest damage compared to brick or rendered masonry. For a home built in 1970, this risk is amplified — the older the construction, the more likely an insurer is to price in potential structural vulnerabilities and higher rebuild complexity.

The sum insured of $1,033,000 reflects the true cost to rebuild a 214 sqm home with quality fittings, a pool, solar panels, and ducted climate control. A higher sum insured directly translates to a higher premium, and this figure is substantially above what many smaller Ningi properties would carry.

The swimming pool adds liability and structural risk to the policy. Pools require additional cover considerations, and their presence typically nudges premiums upward.

Solar panels on the roof are another modern addition that increases the replacement value of the home. Insurers factor in the cost of replacing panels in the event of storm, hail, or fire damage — all realistic risks in South East Queensland.

Ducted climate control is a high-value fixed asset within the building. As a built-in system, it's covered under building insurance and adds to the overall sum insured justification.

On the positive side, the steel/Colorbond roof is viewed favourably by insurers — it's durable, fire-resistant, and performs well in storm conditions. The concrete slab foundation also provides structural stability. These features may be helping to moderate what could otherwise be an even higher premium.

---

Tips for Homeowners in Ningi

1. Review your sum insured regularly At $1,033,000, this is a substantial sum insured. It's worth getting a professional building replacement cost estimate every few years — particularly as construction costs have risen sharply in recent years. Over-insuring drives up premiums unnecessarily, while under-insuring leaves you exposed.

2. Consider your excess strategically This policy carries a $2,000 building excess. Opting for a higher voluntary excess is one of the most effective ways to reduce your annual premium. If you have sufficient savings to cover a larger out-of-pocket cost in the event of a claim, increasing your excess could meaningfully lower what you pay each year.

3. Explore discounts for safety and security upgrades Many insurers offer premium discounts for homes with monitored alarm systems, deadbolts, and smoke detectors. Given the age of this home (1970), it may also be worth confirming that electrical wiring and plumbing have been updated — some insurers apply loadings for older homes that haven't been modernised.

4. Compare quotes across multiple insurers The single most impactful thing any homeowner can do is shop around. Premium variation for the same property across different insurers can be significant — sometimes thousands of dollars. Use a comparison platform like CoverClub to see multiple quotes side by side without the legwork.

---

Ready to Find a Better Rate?

Whether you're renewing your policy or insuring for the first time, comparing quotes is the fastest way to ensure you're not overpaying. At CoverClub, we make it easy to see how your premium stacks up and find competitive alternatives — all in one place. Get a quote today and see what Ningi homeowners are actually paying for cover like yours.