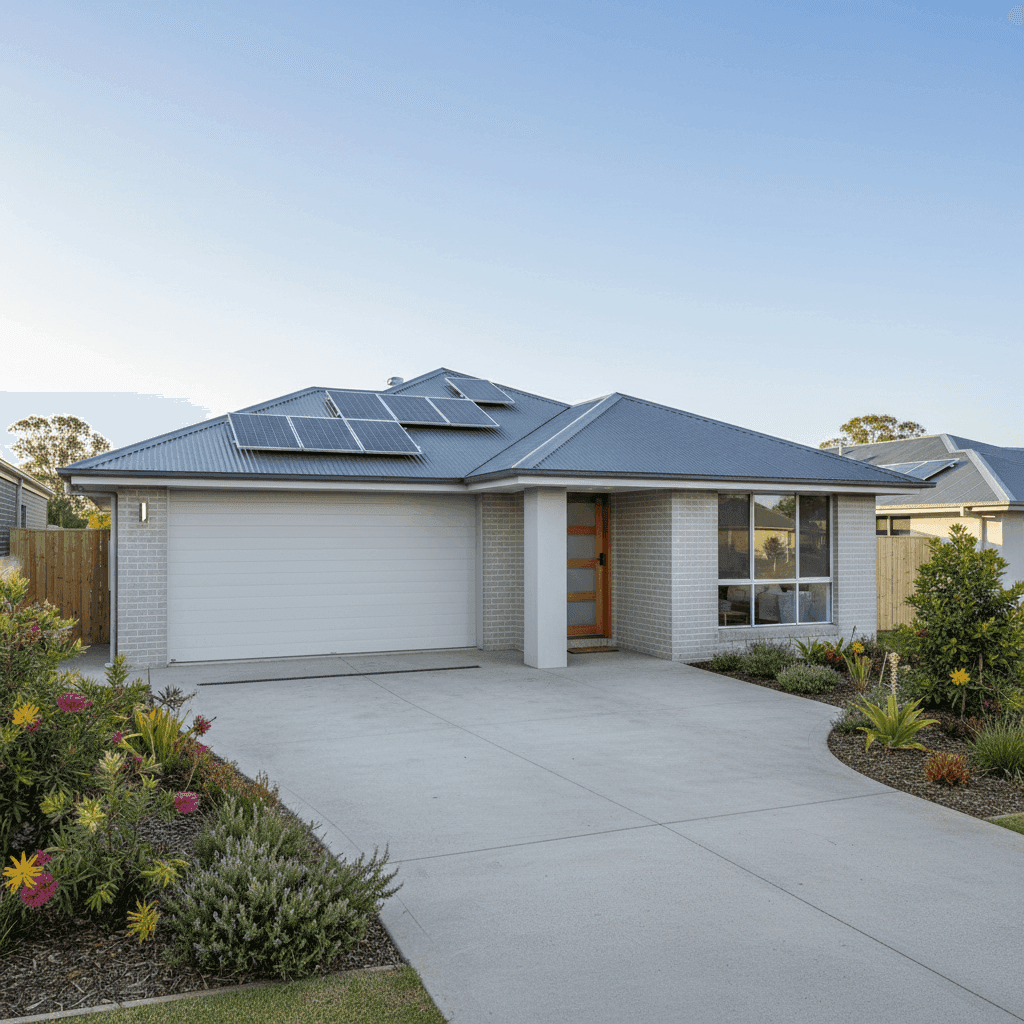

Nirimba is a modern residential suburb on Queensland's Sunshine Coast, and like much of the region, it attracts homeowners looking for a relaxed lifestyle within reach of coastal amenities. If you own a free standing home here — particularly a newer build — understanding what you should be paying for home and contents insurance is an important part of protecting your investment. This article breaks down a real quote for a four-bedroom, two-bathroom home in Nirimba (postcode 4551) and puts it in context against local, state, and national benchmarks.

---

Is This Quote Fair?

The quote in question comes in at $5,054 per year (or roughly $496 per month) for combined home and contents cover, with a building sum insured of $700,000 and contents valued at $50,000. The building excess sits at $3,000 and the contents excess at $1,000.

Our pricing engine rates this quote as FAIR — around average. That's a meaningful finding. It doesn't mean this is the cheapest available option, but it does suggest the premium isn't wildly out of step with what insurers are typically charging for similar properties in this area. Given the relatively high building sum insured ($700,000 for a 214 sqm home built in 2021), a premium in this range is broadly defensible.

That said, "fair" shouldn't be mistaken for "the best you can do." There's often meaningful variation between insurers for the same property, and shopping around remains one of the most effective ways to reduce your annual outgoings.

---

How Nirimba Compares

To put this quote in proper perspective, it helps to look at the local suburb data for Nirimba (QLD 4551) alongside broader benchmarks.

| Benchmark | Premium |

|---|---|

| This quote | $5,054/yr |

| Nirimba suburb average | $3,752/yr |

| Nirimba suburb median | $2,094/yr |

| Nirimba 25th percentile | $1,802/yr |

| Nirimba 75th percentile | $6,683/yr |

| QLD state average | $4,547/yr |

| QLD state median | $3,931/yr |

| National average | $2,965/yr |

| National median | $2,716/yr |

| Sunshine Coast LGA average | $4,608/yr |

A few things stand out here. First, the suburb median of $2,094 is considerably lower than this quote — but medians can be skewed by a large proportion of lower-value properties or contents-only policies in the sample. With 80 quotes in the Nirimba dataset, there's reasonable data to work with, but individual property characteristics (especially a $700,000 building sum insured) will push a premium well above the median.

Compared to the Queensland state average of $4,547 and the Sunshine Coast LGA average of $4,608, this quote of $5,054 sits modestly above both — which is consistent with the "around average" rating. Against the national average of $2,965, it looks more expensive, but Queensland as a whole carries higher insurance costs due to its elevated exposure to severe weather events, including storms, flooding, and hail.

The 75th percentile for the suburb is $6,683, which means roughly a quarter of quotes in Nirimba are even higher than this one. That context matters — it suggests this premium, while above the midpoint, is far from the top of the range.

---

Property Features That Affect Your Premium

Several characteristics of this property will be influencing the premium, both positively and negatively.

Newer construction (2021): Homes built within the last five years typically benefit from lower premiums. Modern building codes require improved structural integrity, better fire resistance, and more resilient materials — all of which reduce the likelihood and severity of claims. This is a meaningful advantage for this property.

Brick veneer external walls: Brick veneer is a well-regarded construction type in Australia. It offers solid fire resistance and durability, which insurers generally view favourably compared to timber or lightweight cladding alternatives.

Steel/Colorbond roof: Colorbond roofing is popular in Queensland for good reason — it handles heat, UV exposure, and moderate storm conditions well. Insurers typically rate it positively, particularly compared to older tile roofs that may be more susceptible to impact damage.

Slab foundation: A concrete slab is the standard foundation type for modern Queensland homes and doesn't carry the elevated risk associated with older stumped or suspended foundations, which can be more vulnerable to movement and moisture.

Solar panels: While solar panels are an asset, they can slightly increase the replacement cost of a building — particularly if they need to be removed and reinstalled during roof repairs. It's worth confirming your policy explicitly covers solar panels as part of the building sum insured.

Ducted climate control: Ducted air conditioning systems are a significant fixed asset and add to the overall replacement value of the home. This is another factor that supports a higher building sum insured and, consequently, a higher premium.

No pool, tiles throughout: The absence of a pool removes a common liability and maintenance risk. Tiled flooring is durable and straightforward for insurers to value, with no particular risk implications.

---

Tips for Homeowners in Nirimba

1. Review your building sum insured carefully A sum insured of $700,000 for a 214 sqm home built in 2021 with standard fittings is on the higher end. It's worth using a building cost calculator (many insurers provide these) to verify the replacement cost estimate is accurate. Over-insuring inflates your premium unnecessarily, while under-insuring can leave you exposed at claim time.

2. Compare quotes before renewal The "fair" rating on this quote means there may be better value available. Insurers price risk differently, and a quote that's average with one provider could be well below average with another. Use CoverClub's comparison tool to see multiple quotes side by side before your renewal date.

3. Confirm solar panel coverage As noted above, solar panels aren't always automatically included in building cover. Check your Product Disclosure Statement (PDS) to confirm they're listed and that the coverage extends to inverters and associated wiring, not just the panels themselves.

4. Consider your excess settings This quote carries a $3,000 building excess. Opting for a higher excess is one of the most direct ways to reduce your annual premium — but it's only a smart trade-off if you could comfortably cover that amount out of pocket in the event of a claim. Review whether the current excess level reflects your financial position and risk appetite.

---

Compare Your Options with CoverClub

Whether you're assessing a new quote or approaching your annual renewal, it pays to know where your premium sits relative to the market. CoverClub makes it easy to compare home and contents insurance quotes for properties across Nirimba and the broader Sunshine Coast region. Enter your address and get started today — it takes just a few minutes and could save you hundreds of dollars a year.