Nirimba is a modern residential suburb on Queensland's Sunshine Coast, and it's attracting plenty of new homeowners drawn to its contemporary housing stock and coastal lifestyle. If you've recently built or purchased a free standing home in the area, understanding what you should be paying for home and contents insurance is an important step in protecting one of your biggest assets. This article breaks down a real insurance quote for a four-bedroom, two-bathroom home in Nirimba (postcode 4551) and puts the numbers in context so you can make a more informed decision.

---

Is This Quote Fair?

The quote in question comes in at $4,436 per year (or around $427 per month) for combined home and contents cover, with a building sum insured of $800,000 and contents valued at $70,000. The building excess is $3,000 and the contents excess is $2,000.

Our price rating for this quote is FAIR — Around Average, which means it sits in a reasonable range relative to comparable properties in the area. It's not the cheapest cover available, but it's also well within the bounds of what other Nirimba homeowners are paying, particularly given the property's features and the level of cover provided.

It's worth noting that a "fair" rating doesn't mean you shouldn't shop around — even a modest saving of a few hundred dollars per year adds up significantly over the life of a mortgage.

---

How Nirimba Compares

To understand whether this premium makes sense, it helps to look at the broader market data. Based on quotes collected for Nirimba (QLD 4551), here's how this quote stacks up:

| Benchmark | Premium |

|---|---|

| This Quote | $4,436/yr |

| Nirimba Suburb Average | $3,752/yr |

| Nirimba Suburb Median | $2,094/yr |

| Nirimba 25th Percentile | $1,802/yr |

| Nirimba 75th Percentile | $6,683/yr |

| Sunshine Coast LGA Average | $4,608/yr |

| QLD State Average | $4,547/yr |

| QLD State Median | $3,931/yr |

| National Average | $2,965/yr |

| National Median | $2,716/yr |

A few things stand out here. First, the suburb's median premium of $2,094 is considerably lower than this quote — but medians can be misleading when there's a wide spread of property values and cover levels in the data set. The gap between the 25th percentile ($1,802) and 75th percentile ($6,683) is enormous, reflecting just how much premiums can vary based on the sum insured, property features, and individual insurer pricing models.

This quote is slightly above the suburb average of $3,752 but sits comfortably below the Sunshine Coast LGA average of $4,608 and the Queensland state average of $4,547. It's also notably higher than the national average of $2,965, though that's largely expected — Queensland premiums tend to run higher than the rest of the country due to elevated weather-related risk across much of the state.

In short, this quote is broadly in line with what you'd expect to pay for a well-appointed property on the Sunshine Coast with a high building sum insured.

---

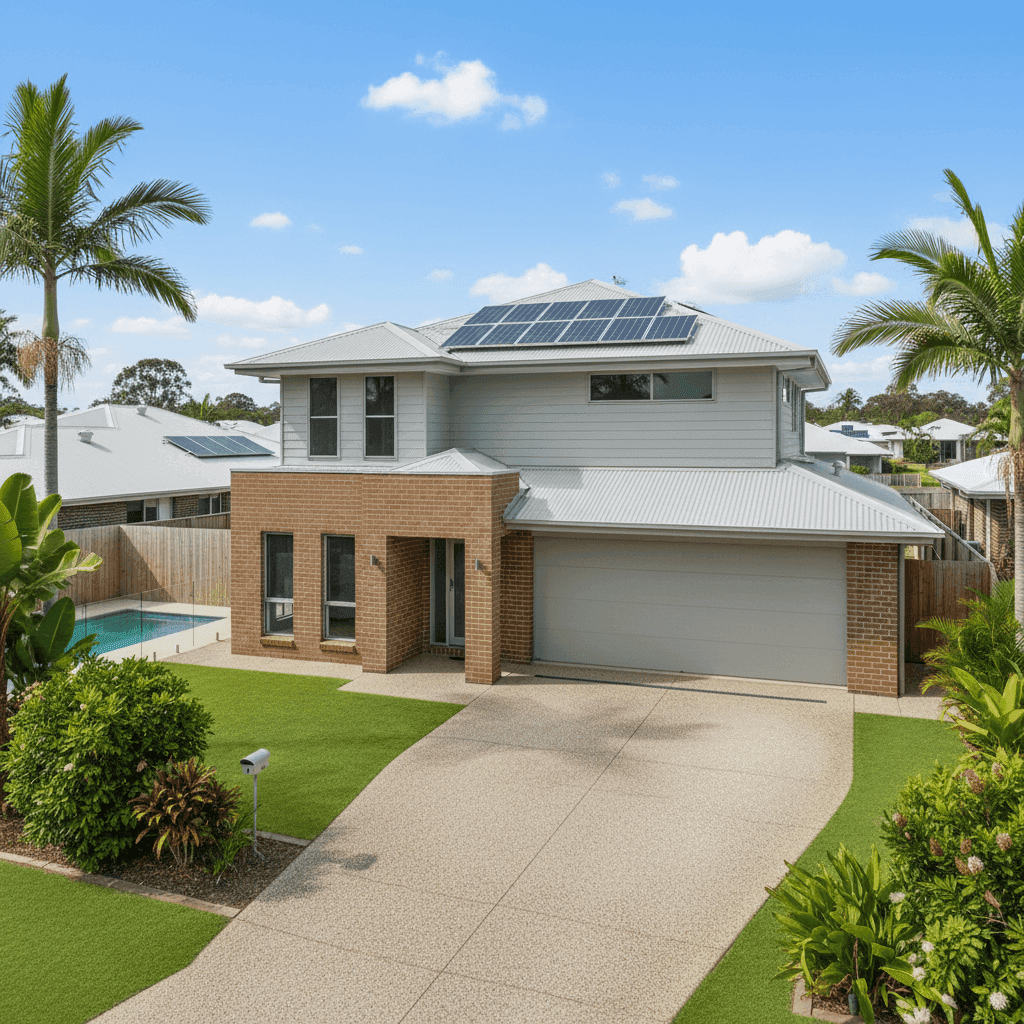

Property Features That Affect Your Premium

Several characteristics of this particular property have a meaningful influence on the premium.

New construction (2025): Newly built homes typically attract more competitive premiums because modern building standards reduce the risk of structural failure, electrical faults, and water damage. Insurers generally view a 2025 build favourably.

Brick veneer walls and Colorbond roof: Brick veneer is a widely accepted and well-regarded wall construction type in Australia. Combined with a steel/Colorbond roof — which is durable, lightweight, and resistant to corrosion — this property presents a solid risk profile from a structural standpoint.

Slab foundation and tile flooring: Concrete slab foundations are standard in Queensland and are generally considered low-risk by insurers. Tiled flooring is similarly straightforward and doesn't add significant premium loading compared to, say, polished timber or carpet.

Above-average fittings: The property's above-average fittings quality means the cost to repair or rebuild will be higher than a standard home, which justifies a higher sum insured and contributes to a larger premium. This is an appropriate reflection of the property's value rather than a red flag.

Swimming pool: Pools add both value and liability to a property. Insurers factor in the cost of pool-related damage (such as cracking or pump failure under certain policies) as well as public liability considerations, which can nudge premiums upward.

Solar panels: Solar systems are now a standard feature on many Queensland homes, but they do add to the replacement cost of the property. Ensuring your building sum insured accounts for the full cost of reinstalling solar panels is important — underinsurance here is a common oversight.

Ducted climate control: Ducted air conditioning is another high-value fixed asset that should be captured in your building sum insured. It's a feature that increases rebuild cost and is reflected in the premium.

No cyclone risk: Despite being on the Sunshine Coast, this property falls outside a designated cyclone risk zone, which is a meaningful factor in keeping the premium lower than it might otherwise be for a coastal Queensland property.

---

Tips for Homeowners in Nirimba

1. Review your sum insured regularly A $800,000 building sum insured is substantial, but construction costs in South East Queensland have risen sharply in recent years. Make sure your sum insured reflects the true cost to rebuild your home from scratch — including the pool, solar system, and ducted air conditioning — not just the market value of the property.

2. Consider your excess carefully This policy carries a $3,000 building excess and a $2,000 contents excess. Opting for a higher excess is a common way to reduce your annual premium, but make sure you'd genuinely be able to cover that amount out of pocket in the event of a claim. Conversely, if cash flow isn't a concern, a higher excess can be a smart way to lower ongoing costs.

3. Don't overlook contents cover At $70,000, the contents value here is relatively modest for a four-bedroom home with above-average fittings. It's worth doing a proper stocktake of your furniture, appliances, electronics, clothing, and valuables to ensure you're not underinsured. A common rule of thumb is to imagine replacing everything in your home from scratch.

4. Shop around at renewal time Insurance loyalty rarely pays off in Australia. Insurers frequently offer their best rates to new customers, meaning long-term policyholders can end up paying significantly more than necessary. Use a comparison tool like CoverClub to benchmark your renewal quote each year.

---

Compare Your Own Quote

Whether you're a new homeowner in Nirimba or reviewing your existing policy, it pays to see what the broader market looks like before you commit. CoverClub makes it easy to compare home and contents insurance quotes side by side, so you can be confident you're getting the right cover at a fair price. Get a quote today and see how your premium stacks up.