If you own a free standing home in Noranda, WA 6062, you're likely paying close attention to the cost of home insurance — especially as premiums across Australia have been climbing in recent years. This article breaks down a real home and contents insurance quote for a four-bedroom property in Noranda, compares it against local, state, and national benchmarks, and offers practical tips to help you get the most out of your cover.

---

Is This Quote Fair?

The quote in question comes in at $1,707 per year (or roughly $164 per month) for combined home and contents insurance, covering a building sum insured of $570,000 and contents valued at $70,000. Both the building and contents excess are set at $500.

Our price rating for this quote is FAIR — Around Average, and the data backs that up. The suburb median premium for Noranda sits at $1,728 per year, meaning this quote lands just below the midpoint — a solid result. The suburb average is slightly higher at $1,847/yr, suggesting a handful of higher-priced quotes are pulling the mean upward.

In practical terms, this homeowner is paying less than what most of their neighbours are quoted, without having skimped on coverage. A $570,000 building sum insured for a 214 sqm double brick home is reasonable, and $70,000 in contents cover is a sensible baseline for a four-bedroom household. There's no cause for alarm here, but as we'll explore below, there's always room to shop around.

---

How Noranda Compares

To put this quote in perspective, here's how Noranda stacks up against broader benchmarks:

| Benchmark | Premium |

|---|---|

| This quote | $1,707/yr |

| Noranda suburb median | $1,728/yr |

| Noranda suburb average | $1,847/yr |

| Noranda 25th percentile | $1,474/yr |

| Noranda 75th percentile | $2,113/yr |

| LGA (Bayswater) average | $1,514/yr |

| WA state median | $2,127/yr |

| WA state average | $2,811/yr |

| National median | $2,764/yr |

| National average | $5,347/yr |

(Based on a sample of 19 quotes in the Noranda suburb. See full [Noranda suburb insurance stats](https://coverclub.com.au/stats/WA/6062/noranda), [WA state stats](https://coverclub.com.au/stats/WA), and [national stats](https://coverclub.com.au/stats/national).)

A few things stand out here. First, Noranda is genuinely affordable compared to the rest of Western Australia — the WA state average of $2,811/yr is nearly 65% higher than what this homeowner is paying. Second, the gap between Noranda and the national average is even more striking; at $5,347/yr nationally, this quote is less than a third of what some Australians are paying elsewhere.

It's worth noting that the LGA average for Bayswater (which encompasses Noranda) is $1,514/yr — slightly below this quote. That difference may reflect variations in property size, age, construction type, or the level of cover selected across different homes in the area. This quote's higher sum insured and contents value likely account for some of that gap.

For anyone in the suburb curious about where they stand, the Noranda insurance stats page provides an up-to-date picture of what locals are paying.

---

Property Features That Affect Your Premium

Several characteristics of this property play a meaningful role in how insurers price the risk — for better and for worse.

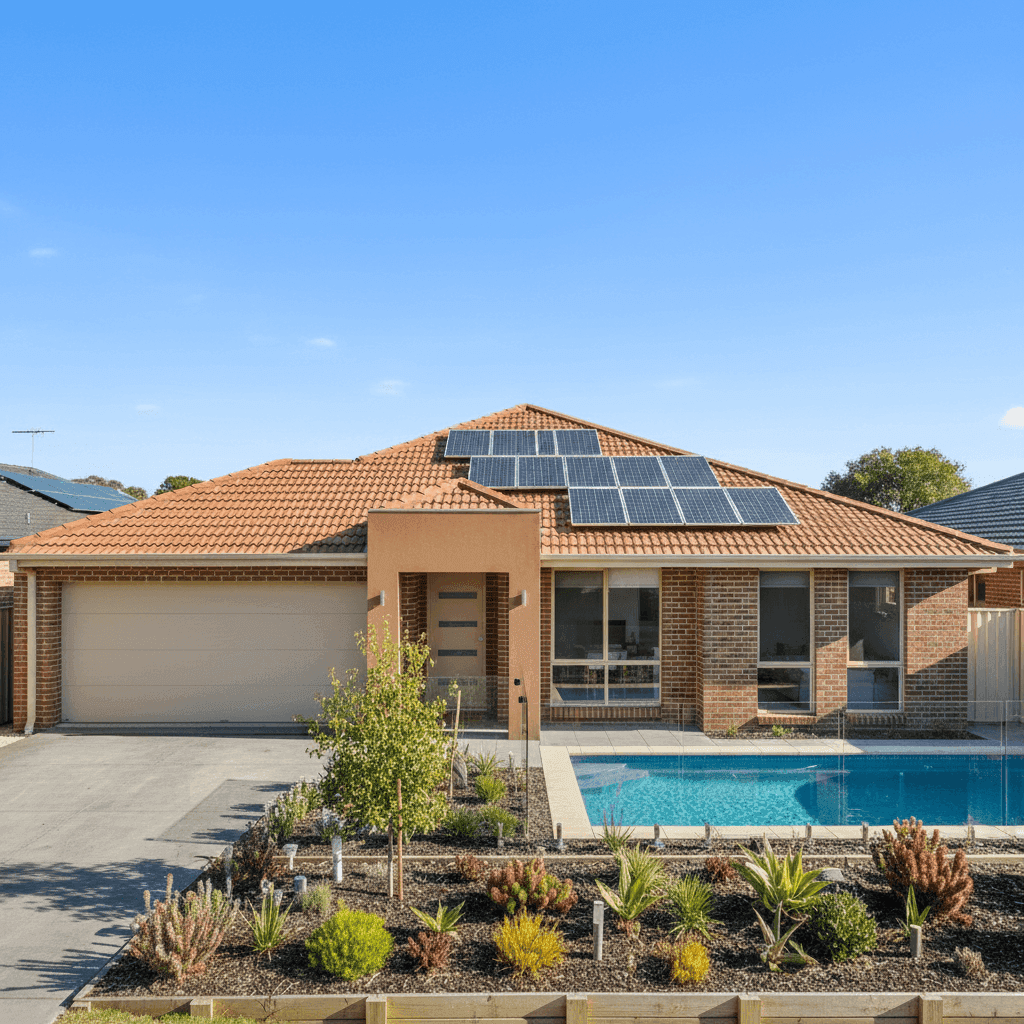

Double Brick Construction Double brick is widely regarded as one of the most durable and fire-resistant wall types in Australian residential construction. Insurers generally view it favourably, as it's less susceptible to storm damage and structural failure than lighter-weight alternatives like weatherboard or cladding. For a home built in 1985, double brick also signals solid, enduring construction that has stood the test of time.

Tiled Roof Terracotta or concrete tiles are a common and well-regarded roofing choice in Perth's climate. They offer good durability and are considered lower risk than materials like Zincalume or older corrugated iron. That said, tiles can crack under impact (such as hail), so it's worth confirming your policy covers roof tile replacement.

Slab Foundation A concrete slab is a stable and widely used foundation type in Western Australia. It tends to be associated with lower subsidence risk compared to strip or pier footings in certain soil types, which can be a positive factor in premium calculations.

Swimming Pool Having a pool on the property introduces some additional liability considerations. Most home insurance policies include public liability cover, which would apply if a guest were injured in or around the pool. Ensure your policy's liability limit is adequate — $20 million is a common benchmark.

Solar Panels Solar panels are increasingly common on Perth rooftops, and most insurers now include them under building cover as a fixed fixture. It's worth double-checking that your policy explicitly covers the panels for storm damage, fire, and accidental breakage, as some older policies may not.

Ducted Climate Control Ducted air conditioning is a significant fixed asset and typically covered under building insurance. Given the cost of replacing a full ducted system, confirming it's included in your sum insured is a sensible step.

Flooring: Timber and Laminate Timber and laminate floors can be costly to replace following water damage or fire. Contents policies don't always cover fixed flooring, so check whether your building policy includes floor coverings — particularly for timber boards, which can be expensive to match and reinstate.

---

Tips for Homeowners in Noranda

1. Review your building sum insured annually Construction costs in Perth have risen considerably over the past few years. A sum insured that was accurate two years ago may no longer be sufficient to fully rebuild your home today. Use a building cost calculator or speak with a quantity surveyor to ensure your $570,000 figure still reflects current rebuild costs for a 214 sqm double brick home.

2. Don't overlook your pool and solar panel cover Both features add value — and risk — to your property. Review your policy documents to confirm that your pool structure, equipment (pump, filter, heating), and solar panels are explicitly covered, and for what events. Accidental damage and storm cover for these items can vary significantly between insurers.

3. Compare quotes before renewal With 19 quotes sampled in Noranda, there's a meaningful spread between the 25th percentile ($1,474/yr) and the 75th percentile ($2,113/yr). That's a difference of over $600 per year for what may be similar cover. Shopping around at renewal time — rather than auto-renewing — is one of the simplest ways to avoid overpaying.

4. Consider your contents figure carefully $70,000 in contents cover is a reasonable starting point for a four-bedroom home, but it can be easy to underestimate the true replacement value of everything inside. Walk through each room and account for furniture, appliances, clothing, jewellery, electronics, and tools. Many households find their actual contents value is higher than they initially assumed.

---

Ready to Compare Home Insurance in Noranda?

Whether you're reviewing an existing policy or shopping for the first time, comparing multiple quotes is the most effective way to ensure you're getting fair value. CoverClub makes it easy to see what insurers are offering for your specific property. Get a home insurance quote today and see how your premium stacks up against what others in Noranda are paying.